Jul-2026

Sales

Trend

6-Month

Product Count

SKUs

Avg Price

YoY Sales Change

YoY Price Change

Market Insights Snapshot

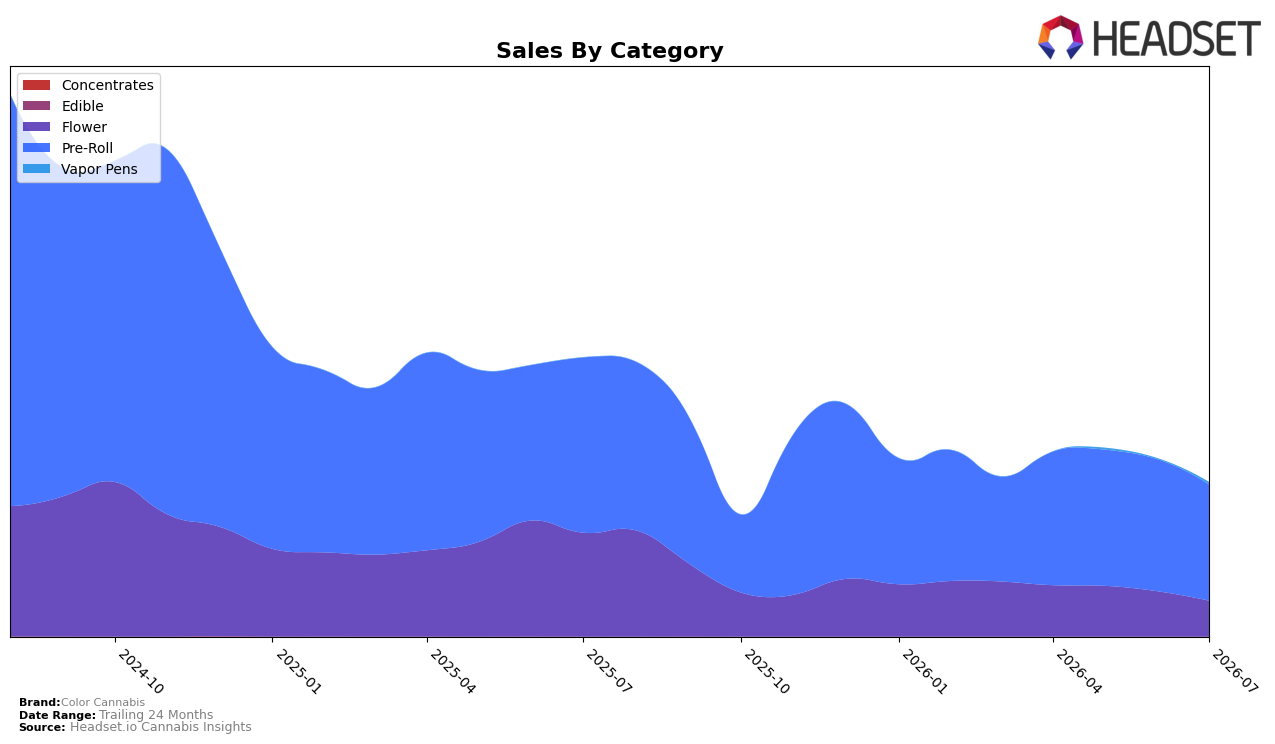

In July 2026, Color Cannabis concentrated 75.35% of sales in Pre-Roll, with Flower at 23.18% and Vapor Pens at 1.47%, while overall brand sales fell 44.84% year over year and average price declined 11.86%. Within the mix, Pre-Roll contracted 33.81% YoY and 12.09% MoM, Flower declined 65.64% YoY and 20.86% MoM, and Vapor Pens expanded 208.79% MoM from a very small base, indicating a tactical tilt toward value-priced formats as Pre-Roll average price sat at 17.72 versus Flower at 28.55. Taken together, the heavier reliance on Pre-Roll and sharper Flower attrition imply Color Cannabis is consolidating around its largest, lower-priced format to stabilize share despite broad sales contraction.

Positionally, a 32 rank in British Columbia Pre-Roll, combined with a 12.09% MoM decline in that category and a 20.86% MoM drop in Flower, suggests competitive pressure is eroding shelf velocity faster in higher-priced segments. The 208.79% MoM lift in Vapor Pens, alongside an 11.86% brand-wide price decrease and a 33.81% YoY drop in Pre-Roll, indicates a pivot toward trial in adjacent inhalables while defending the core Pre-Roll base. This pattern implies Color Cannabis is trading down on price to protect Pre-Roll share while testing a small foothold in Vapor Pens to offset severe Flower losses.

Competitive Landscape

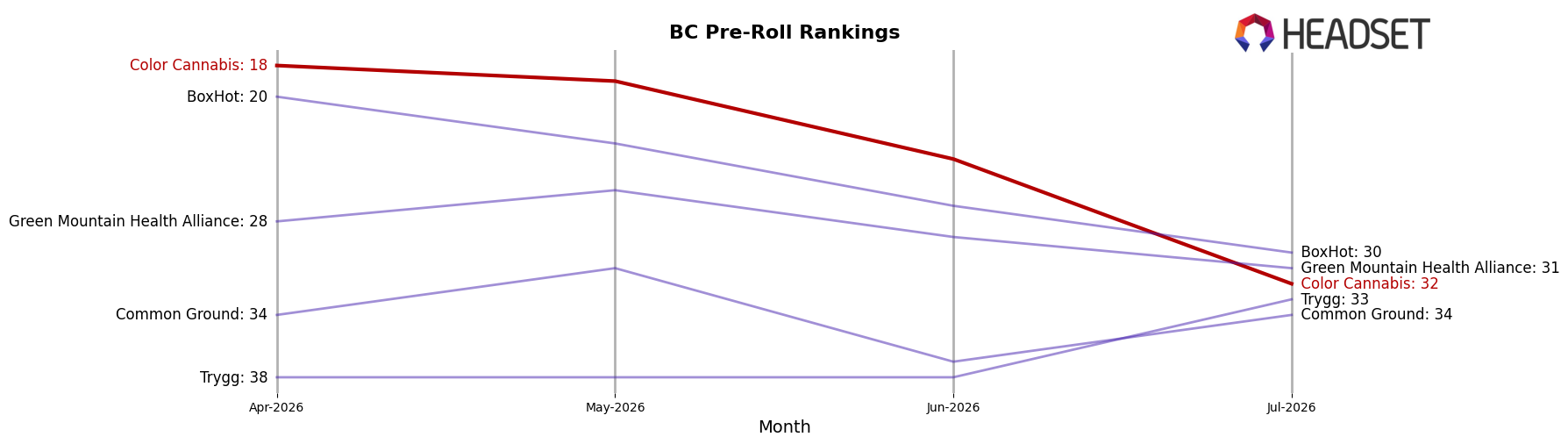

Color Cannabis sits at rank #32 in BC Pre-Roll for July 2026, down 19 positions year over year from #13 and sliding 14 spots from #18 in April 2026, despite a historical peak of #4 in September 2024; meanwhile, General Admission holds #1 with a -22.3% YoY sales change, and Back Forty / Back 40 Cannabis advanced to #2 with a +215.2% YoY sales lift from a #17 rank a year ago, indicating that Color Cannabis’s mid-pack drop is driven more by rivals’ faster gains than by absolute category contraction, and the trajectory implies continued share erosion unless rank momentum stabilizes.

Notable Products

Space Cake Pre-Roll 10-Pack (3.5g) posted a -15.3% month-over-month decline and slid to rank 5, while Mango Haze Pre-Roll 10-Pack (3.5g) fell -32.7% yet still held rank 1, indicating volume concentration atop the lineup even as velocity cooled. Blueberry Seagal Pre-Roll 10-Pack (3.5g) countered the trend with a +23.6% lift at rank 6, and Pedro's Sweet Sativa Pre Roll 2-Pack (0.7g) dropped -20.5% at rank 8, with eight of the top ten SKUs concentrated in Pre-Rolls that are diverging between value 10-packs and smaller 2-packs. Mango Haze (3.5g) in Flower inched up +6.7% at rank 7 while Blueberry Seagal (7g) contracted -34.5% at rank 9, and total monthly revenue was $619,036, signaling the portfolio is leaning on large-pack Pre-Rolls for share while mid-size Flower and 2-packs shed momentum.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.