Jul-2026

Sales

Trend

6-Month

Product Count

SKUs

Avg Price

YoY Sales Change

YoY Price Change

Market Insights Snapshot

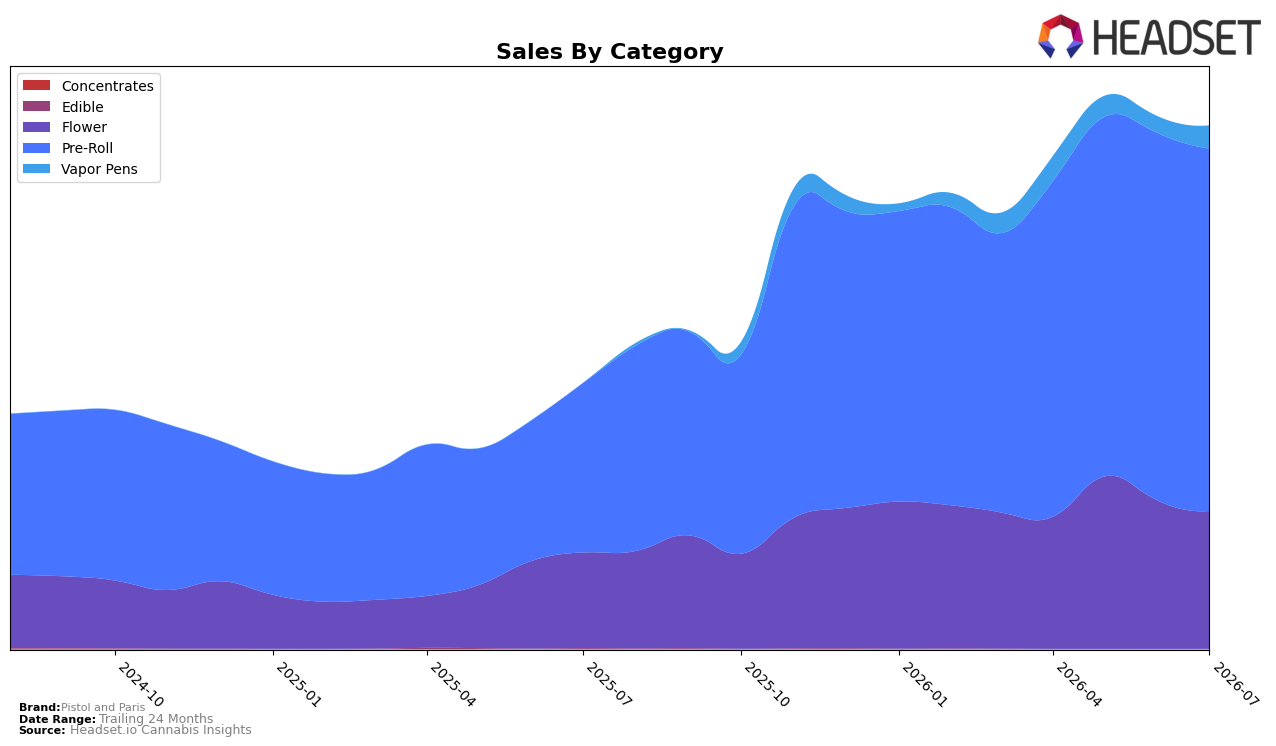

In July 2026, Pistol and Paris leaned heavily into Pre-Roll, which captured 69.29% share with 114.02% year-over-year growth while slipping 1.37% month over month, versus Flower at 26.32% share growing 44.23% YoY but falling 6.97% MoM, and Vapor Pens at 4.38% share with a 38.04% MoM surge and no reported YoY baseline. The brand’s average price rose 4.43% YoY to $23.65 even as Pre-Roll’s average price sat lower at 19.98, and the brand ranked 7 in Pre-Roll in British Columbia; taken together, the mix shows a Pre-Roll-led engine that is expanding YoY but softening sequentially, with Vapor Pens emerging as the only MoM gainer, implying a gradual diversification pressure point.

The split between a 114.02% YoY gain in Pre-Roll and a 6.97% MoM decline in Flower suggests the brand’s short-term momentum depends on stabilizing repeat Pre-Roll turns while seeding Vapor Pens, where a 38.04% MoM rise can offset Pre-Roll’s 1.37% MoM dip if scaled. With a 7 rank in British Columbia Pre-Roll and average price up 4.43% YoY against a core category price point of 19.98, the positioning implies room to trade up in Flower (40.07 average price) without losing the Pre-Roll volume base, meaning near-term share defense rests on price-pack architecture while medium-term growth hinges on extending the Vapor Pens foothold from 4.38% mix.

Competitive Landscape

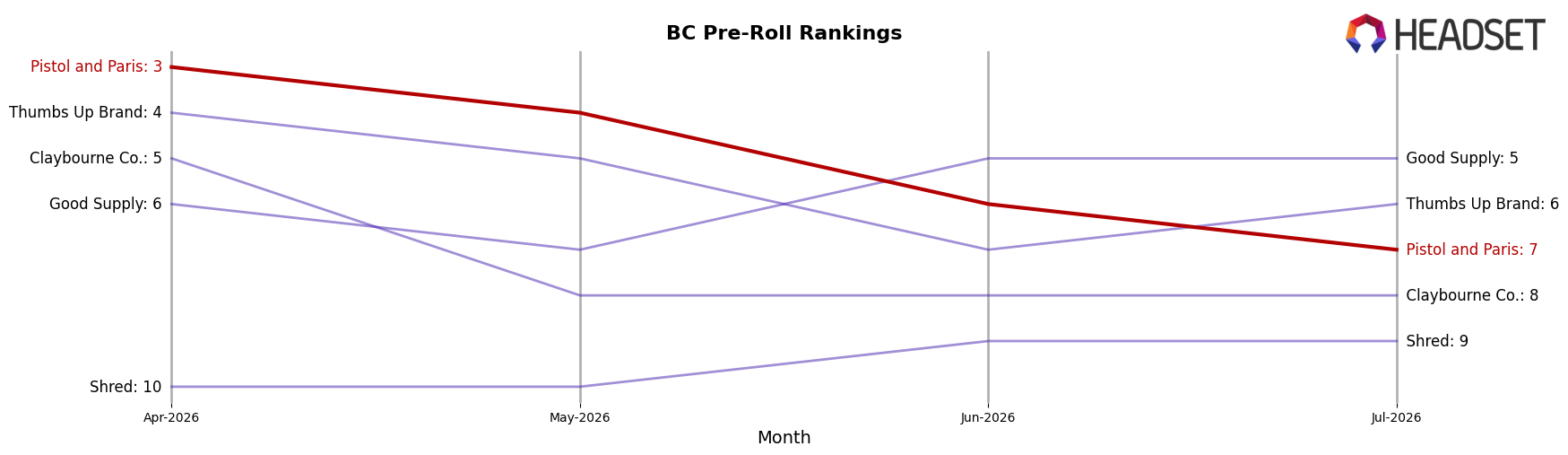

Pistol and Paris sits at rank #7 in BC Pre-Roll in July 2026, improving 4 positions year over year from #11 while sliding 4 spots since April 2026 when it was #3; the brand’s peak was #2 in November 2025, indicating a 5-position drop from that high to today. In contrast, Back Forty / Back 40 Cannabis climbed from #17 to #2 with a 215.2% YoY sales increase, while General Admission held #1 year over year despite a 22.3% YoY sales decline, signaling that Pistol and Paris’s recent pullback from #3 to #7 is less about category-wide momentum shifts and more about ceding share to faster risers; this trajectory implies mid-pack stability year over year but a need to arrest short-term rank erosion to reengage its late-2025 ceiling.

Notable Products

Blackberry Breath Pre-Roll 3-Pack (1.5g) posted the steepest decline in July 2026 at -26.46% while slipping within the top 10 at rank 8, whereas Pink Goo Pre-Roll (1g) fell -18.90% and held rank 4. In contrast, Blue Zushi Pre-Roll 3-Pack (1.5g) climbed +34.47% to rank 5 as Hawaiian Fanta Pre-Roll 10-Pack (5g) advanced +18.78% at rank 9. The concentration remains anchored in Pre-Rolls, with eight of the top ten SKUs from this format, implying reliance on multi-pack convenience even as single-gram offerings soften. This pattern suggests Pistol and Paris is migrating demand toward larger pack sizes and select flavor lines, reallocating momentum away from underperforming single units.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.