Jul-2026

Sales

Trend

6-Month

Product Count

SKUs

Avg Price

YoY Sales Change

YoY Price Change

Market Insights Snapshot

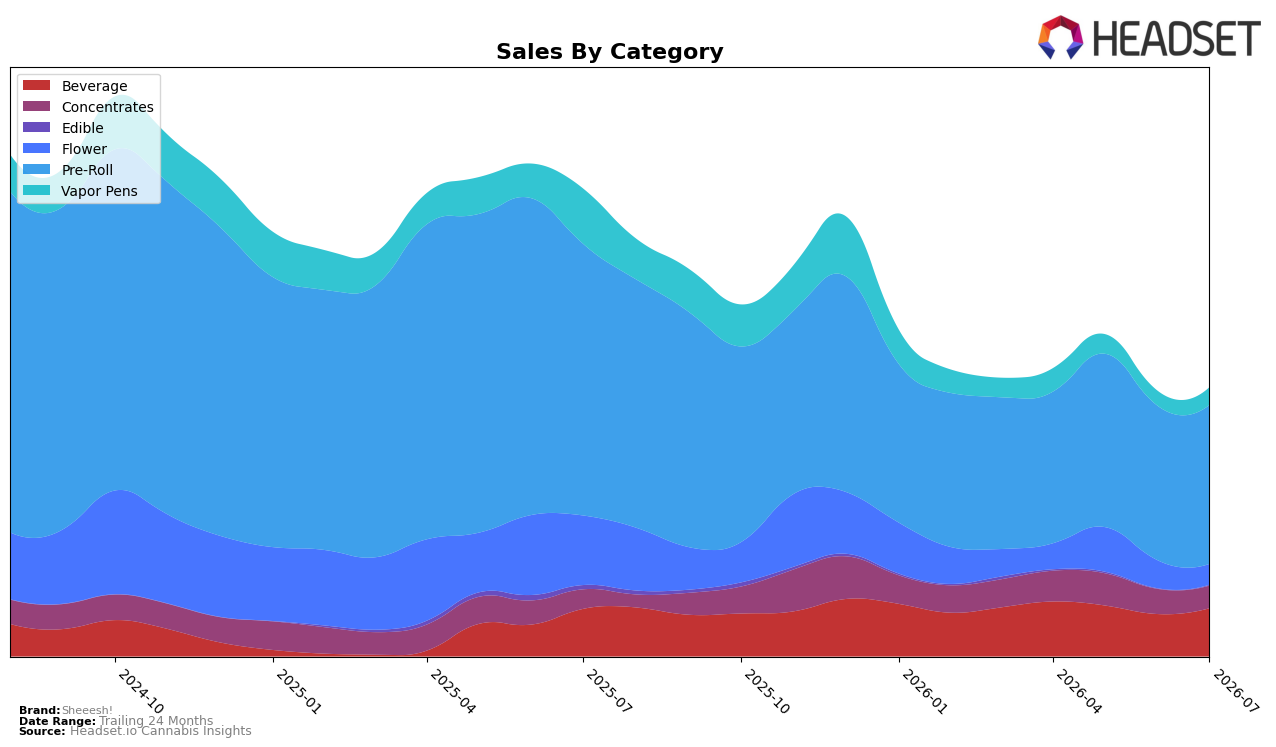

In July 2026, Sheeesh! concentrated 59.32% of sales in Pre-Roll with year-over-year decline of 41.55% and month-over-month growth of 2.96%, while Beverage expanded to 17.94% share with 1.32% YoY and 13.75% MoM gains; meanwhile, Concentrates held 8.35% share with 16.08% YoY growth but a 9.92% MoM drop. Flower contracted to 7.66% share with a 70.40% YoY and 25.71% MoM decline, and Vapor Pens at 6.52% share fell 68.28% YoY despite an 18.50% MoM lift; Edible remained negligible at 0.20% share with an 86.64% YoY decline despite 112.17% MoM volatility. With brand-level sales down 42.64% YoY and average price down 19.74%, the pattern implies a pivot toward lower-ticket formats (notably Beverage and Pre-Roll) to stabilize volume while de-emphasizing premium-priced Flower and Vapor Pens.

These shifts position Sheeesh! as a Pre-Roll–led player using Beverage and short-cycle Vapor Pens momentum to buffer demand, but the 59 rank in Ontario Pre-Roll and a 41.39% 24‑month sales contraction imply share is vulnerable if Pre-Roll softness persists. The combination of 13.75% MoM growth in Beverage alongside a 25.71% MoM decline in Flower suggests reallocation toward value-leaning categories, and the 9.92% MoM dip in Concentrates against 16.08% YoY growth indicates inconsistent replenishment that could impede rank recovery; net effect, Sheeesh! must lean into price-pack architecture where average tickets of $8.03–$16.28 dominate and treat premium tiers as selective rather than scale drivers.

Competitive Landscape

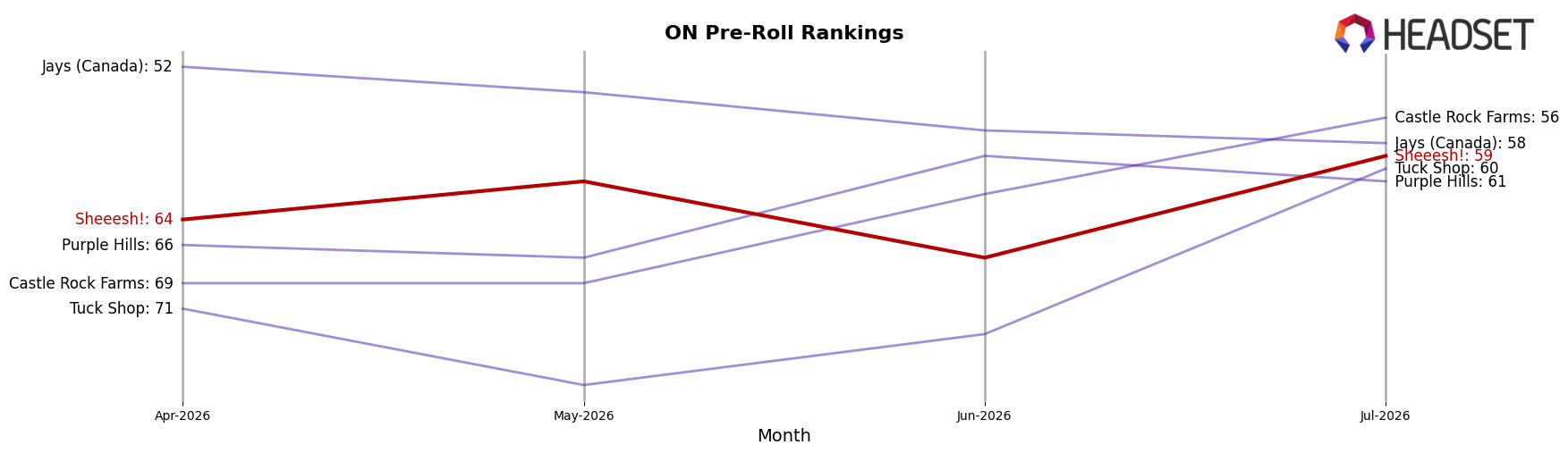

Sheeesh! sits at rank #59 in ON Pre-Roll for July 2026, down 19 positions year over year from #40, yet up 5 positions from April 2026 when it was #64; against this mixed trajectory, Back Forty / Back 40 Cannabis advanced to #1 from #2 while growing sales 67.4% YoY, and General Admission slipped to #2 from #1 with a 23.2% YoY sales decline. The gap between Sheeesh!’s current #59 and its peak of #24 in September 2024 underscores lost share of voice in a tier that is consolidating at the top, as rising competitors like Spinach pushed up from #14 to #5 on 65.3% YoY growth while Sheeesh! moved only 5 ranks in the last three months; the pattern implies Sheeesh!’s rank is drifting toward the long tail unless near-term execution reverses multi-quarter slippage.

Notable Products

SMURF Infused Pre-Roll (1g) plunged 83.8% month over month while holding rank 1, and O.G. Hash (2g) slipped 9.9% at rank 7, signaling a sharp pivot away from the prior flagship’s volume even as it technically remains top-ranked. In contrast, SMRF Liquid Diamond Cartridge (1g) climbed 40.5% to rank 9 and Minionz Infused Pre-Roll (1g) rose 41.5% at rank 3, while three Beverage SKUs sit at ranks 2, 4, and 5 with gains of 16.2%, 16.0%, and 23.8%, respectively; this mix suggests demand is shifting from a single pre-roll hero toward a broader basket across beverages and vapor. With four of the top ten as Pre-Roll SKUs and three as Beverage SKUs, the concentration across two categories points to a portfolio hedging strategy that reduces reliance on any one format and reallocates attention to growing, flavor-led occasions.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.