Jul-2026

Sales

Trend

6-Month

Product Count

SKUs

Avg Price

YoY Sales Change

YoY Price Change

Where to Buy

&Shine is stocked at 812 licensed dispensaries across Illinois, New Jersey, and 10 other states, 183 of them in Illinois, with the deepest coverage in Chicago, Springfield, East Peoria, Naperville, and Normal. Search by ZIP code or city below to find the closest one, or filter by product type if you are after a specific format.

Market Insights Snapshot

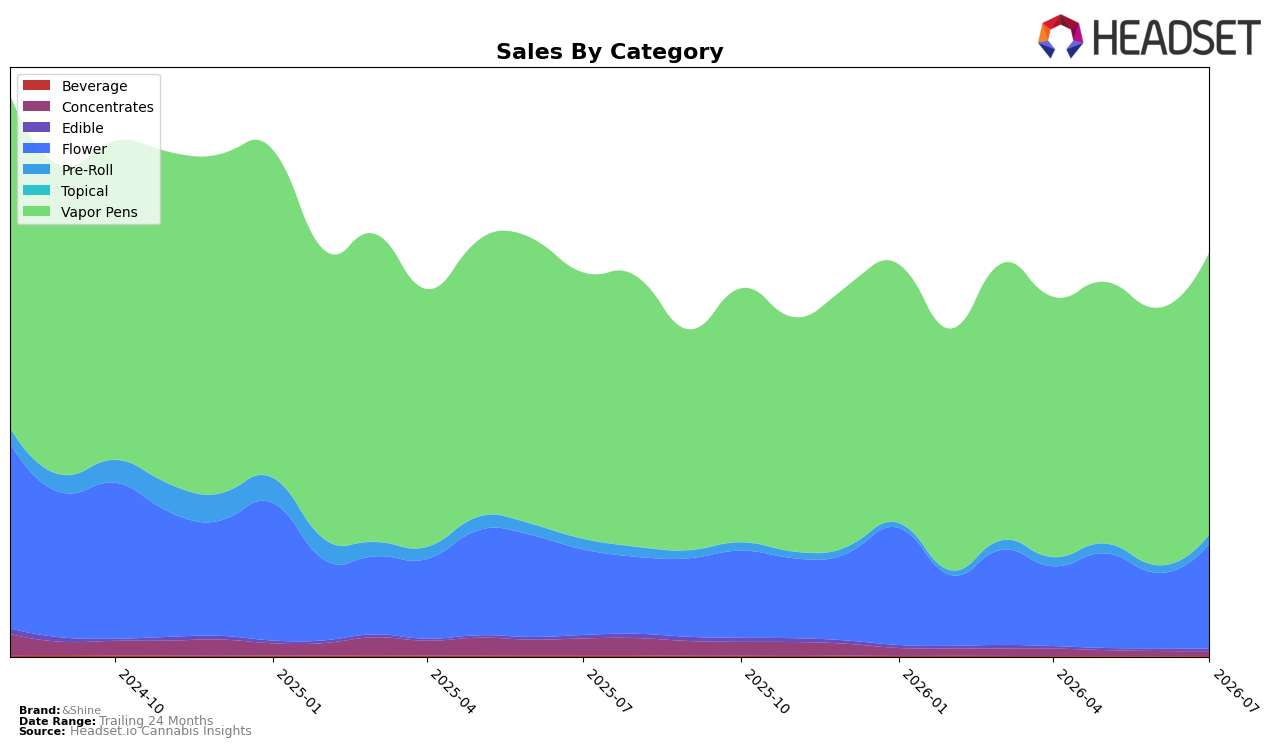

In July 2026, &Shine’s mix skews heavily to Vapor Pens at 69.96% share with 5.99% YoY growth and 9.70% MoM, while Flower expanded to 25.98% share with 22.79% YoY and 39.17% MoM gains; together, these two categories now account for 95.94% of sales, up sharply as Pre-Roll contracted to 2.20% share on a -12.59% YoY but rebounded 23.07% MoM. Peripheral formats are retreating: Concentrates fell -72.44% YoY and -6.67% MoM to 1.12% share, and Edible declined -27.43% YoY and -1.75% MoM to 0.57% share, even as Beverage lifted 30.43% MoM despite a -57.00% YoY drop to 0.16% share; the pattern implies deliberate concentration in inhalables, with July 2026 momentum consolidating around Vapor Pens and Flower rather than diversifying into smaller formats.

The tilt toward Vapor Pens (ranked 1 in Vapor Pens in Illinois) alongside outsized MoM acceleration in Flower (39.17%) and a 10.52% YoY increase in average price signals pricing power anchored in two lead formats, while negative YoY in Concentrates (-72.44%) and Edible (-27.43%) reduces cross-format hedge. With brand sales up 5.35% YoY but down -17.21% over 24 months, the July 2026 configuration concentrates risk and opportunity in two categories whose combined MoM growth of 9.70% and 39.17% outpaces the rest, implying &Shine’s near-term positioning is to win depth in inhalables and accept lower breadth in ancillary formats to sustain rank and margin in its core market.

Competitive Landscape

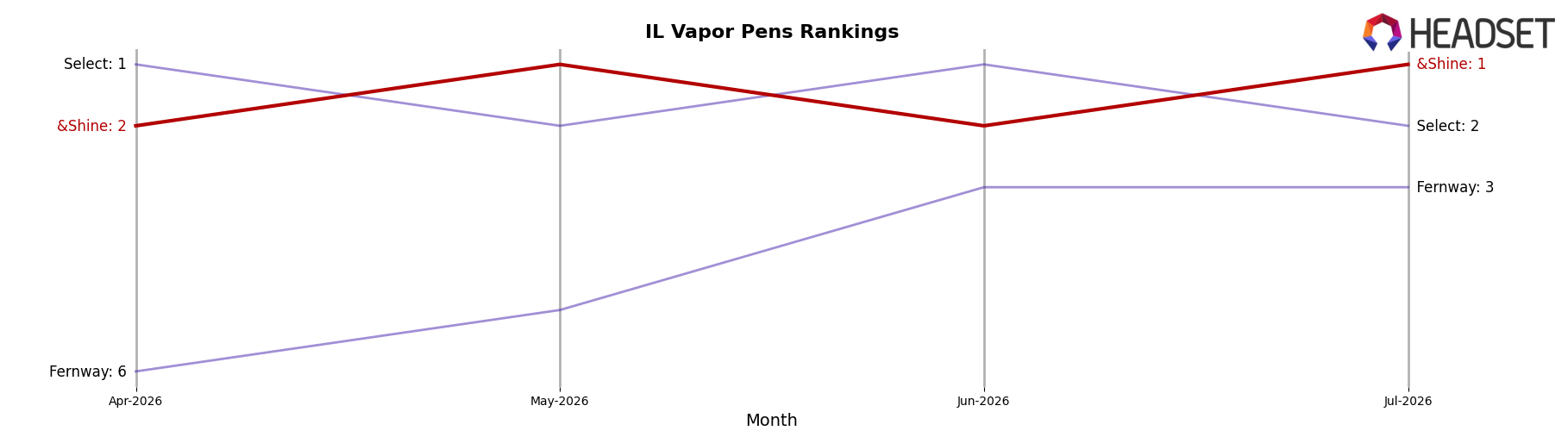

&Shine holds rank #1 in IL Vapor Pens in July 2026, unchanged from #1 a year earlier, after moving up from #2 three months ago to reach a peak at #1 in July 2026; meanwhile, Select sits at #2 now versus #2 a year ago with sales up 15.3% YoY, and Joos climbed from #6 to #4 on 31.9% YoY sales growth, indicating faster chasers are tightening the gap even as &Shine’s top rank remains steady. The combination of a flat YoY rank at #1 and a quarter-over-quarter rise from #2 to #1, alongside RYTHM slipping from #4 to #5 despite 23.0% YoY sales growth, implies &Shine’s leadership depends more on relative momentum than absolute expansion, signaling that maintaining #1 will require defending against competitors gaining share at lower ranks.

Notable Products

Blue Dream Distillate Disposable (2g) led July 2026 with a 71.5% month-over-month surge to $421,289 and held rank 1, while Pineapple Express Distillate CDT Cartridge (1g) fell 31.1% and sat at rank 3; that spread between +71.5% and -31.1% within the top three signals a rotation toward high-capacity disposables over legacy 1g cartridges. With Vapor Pens occupying nine of the top ten ranks and Remix - Blue Dream Infused Pre-Roll (1g) the lone outlier at rank 10, the assortment is concentrated in a single category, implying pricing, merchandising, and R&D are coalescing around disposable pen formats where velocity is accelerating fastest. The minor uplift for Durban Poison Distillate Cartridge (1g) at +10.4% in rank 4 against a steep decline for Pineapple Express Distillate CDT Cartridge (1g) at -31.1% indicates flavor-specific elasticity, suggesting SKU pruning on underperforming 1g cartridges could fund further expansion of successful 2g disposables.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.