Where to Buy

Snoozy is stocked at 104 licensed dispensaries across New York, with the deepest coverage in New York, Rochester, Buffalo, Depew, and Farmingdale. Search by ZIP code or city below to find the closest one.

Market Insights Snapshot

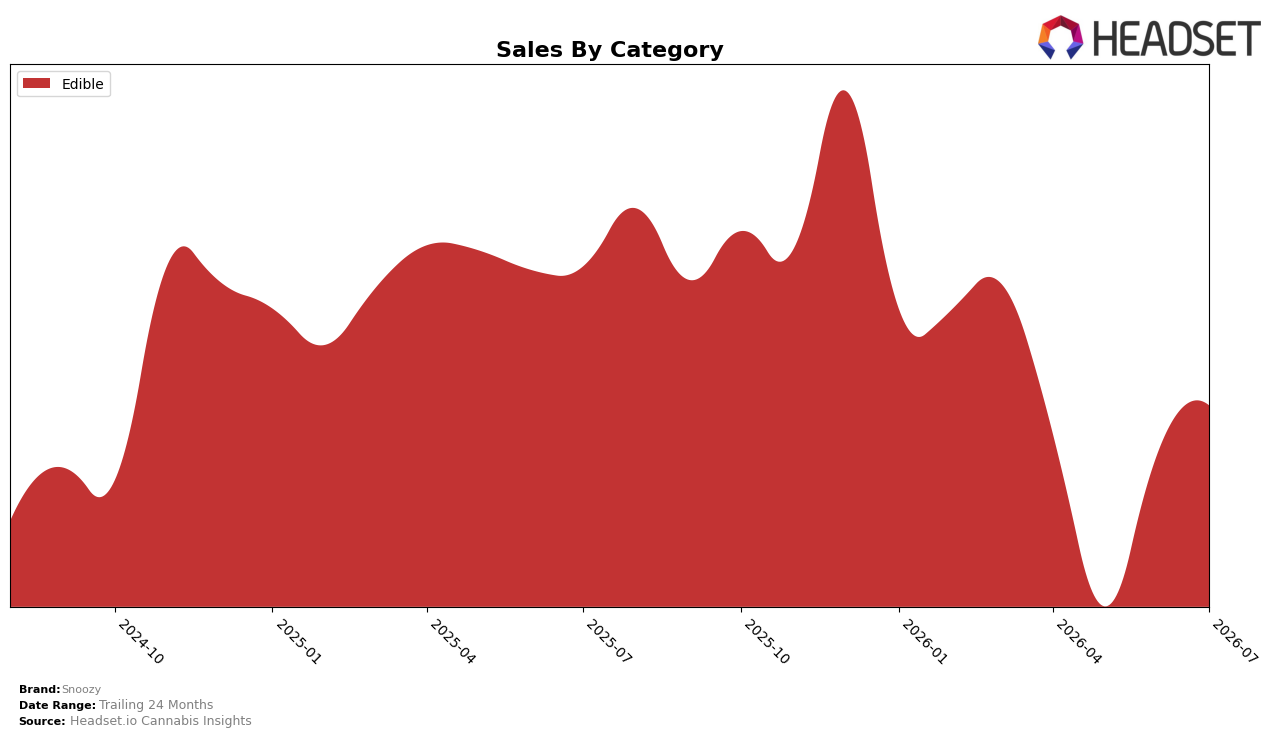

Snoozy operated as a single-category brand in July 2026, with Edible accounting for 100.0% of sales and an average price of $27.29. Within Edible, sales fell 20.21% year over year while rising 9.56% month over month, and average price declined 3.36% year over year, signaling a volume-led mix within a narrower portfolio. In New York Edible, Snoozy held rank 23 in July 2026, positioning the brand in the lower-mid tier even as month-over-month momentum improved. The pattern implies Snoozy is increasingly reliant on a single Edible line to offset a deeper year-over-year contraction, meaning short-term gains are coming from execution within Edible rather than diversification across categories.

The combination of a 9.56% month-over-month lift alongside a 20.21% year-over-year decline and a 3.36% price decrease indicates Snoozy’s positioning is shifting toward value-accessible Edibles to drive unit throughput, not premium-priced differentiation. Holding the 23 rank in New York Edible while Edible is 100.0% of the mix suggests competitive exposure is concentrated at a single shelf, so incremental share gains will hinge more on flavor/format depth and promotional cadence than channel expansion. The pattern implies that sustained recovery will require either price discipline that preserves the 9.56% month-over-month unit momentum or selective category re-entry to reduce reliance on a single Edible ranking corridor.

Competitive Landscape

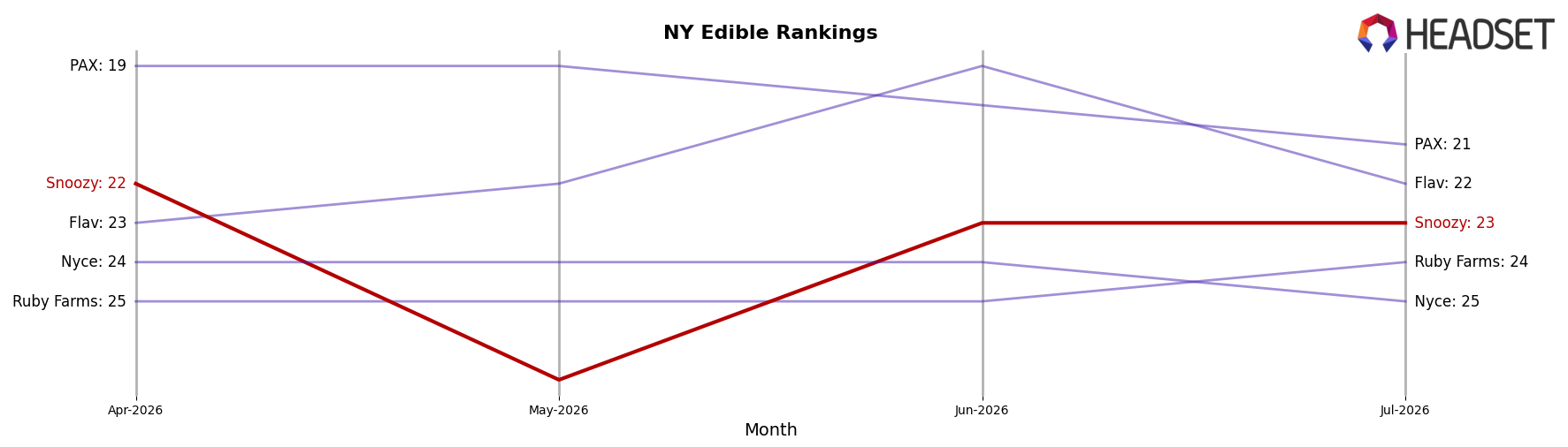

Snoozy sits at rank #23 in NY Edible for July 2026, down 5 positions year over year from #18, and off 1 spot from April 2026 when it was #22; the slide from a peak of #15 in February 2025 to #23 now indicates erosion in competitive standing. In the same July 2026 period, Off Hours moved down from #1 to #2 while posting a -10.4% year-over-year sales change, and Wyld held steady at #3 with a 7.4% sales increase; this divergence—Snoozy losing 5 ranks while a stable #3 competitor grows—implies a share shift away from mid-pack brands toward leaders. The pattern of a 1-rank quarter-over-quarter dip alongside a 5-rank year-over-year decline suggests that without a reversal, Snoozy’s trajectory points to continued mid-20s placement rather than a return toward its #15 peak.

Notable Products

CBD/CBG/CBC/THC 1:1:1 Sigh of Relief Blueberry Gummies 20-Pack (100mg CBD, 100mg CBG, 100mg CBC, 100mg THC) delivered the largest month-over-month gain at 86.1% while sitting at rank 6, contrasting with Sleep with Benefits - CBD/THC/CBN 1:1:1 Raspberry Flavored Bedtime Gummies 20-Pack (100mg CBD, 100mg THC, 100mg CBN) which fell 20.3% to rank 3. The top two positions tightened around bedtime and balance formulations, with CBD/THC/CBN 10:10:5 Raspberry Flavored Bedtime Chews 20-Pack (200mg CBD, 200mg THC, 100mg CBN) up 25.3% at rank 1 and CBD/THC 4:1 Free Mind Strawberry Gummies 20-Pack (400mg CBD, 100mg THC) up 19.3% at rank 2. Four of the top six are multi-cannabinoid edible SKUs, and CBD/CBG/THC 1:1:1 New Morning Highs Orange Flavored Daytime Gummies 20-Pack rose 29.0% at rank 4 while CBD/THC 2:1 Stress Free Mind Gummies 20-Pack climbed 37.4% at rank 7, implying Snoozy’s mix is tilting toward diversified, ratio-based gummies that balance bedtime and daytime need-states rather than a single hero line.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.