Jun-2026

Sales

Trend

6-Month

Product Count

SKUs

Avg Price

YoY Sales Change

YoY Price Change

Market Insights Snapshot

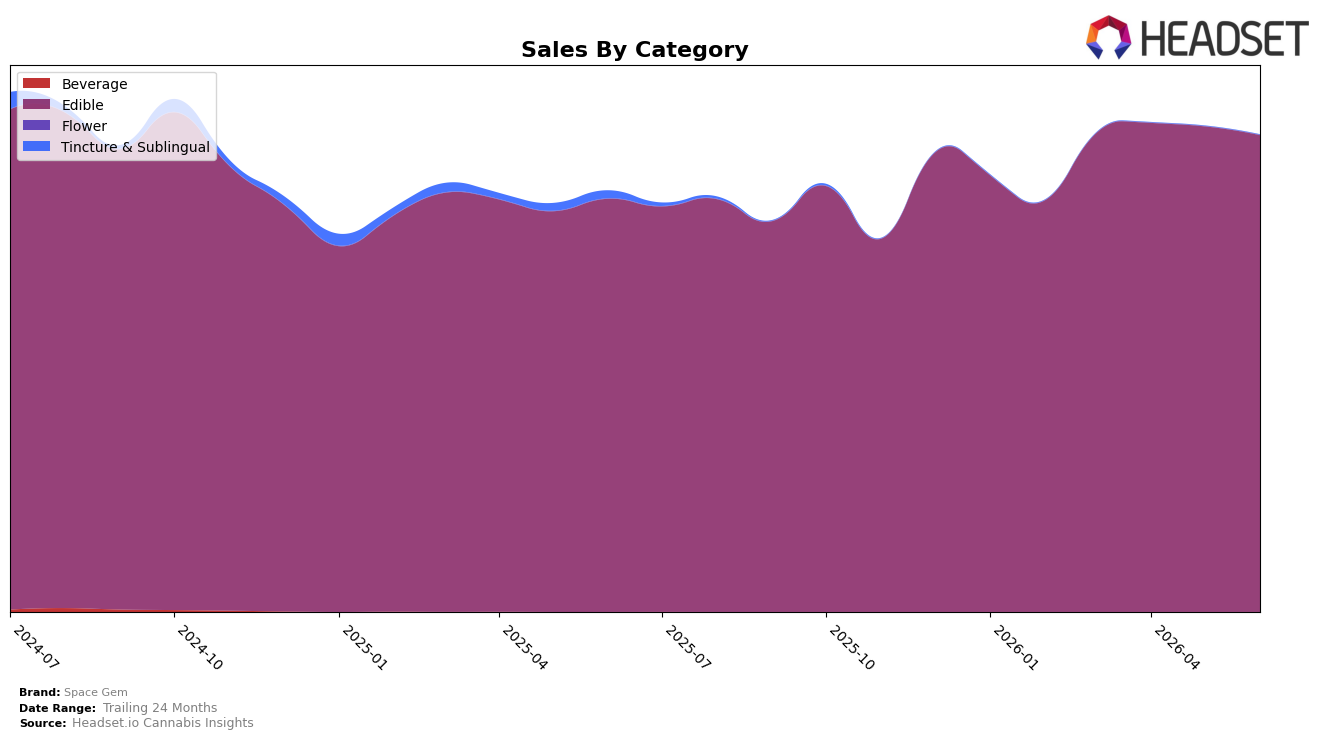

In June 2026, Space Gem operated as a single-category brand with Edible accounting for 100.0% of sales, which concentrates exposure entirely in one segment while overall brand sales rose 13.3% year over year and declined 1.8% month over month within Edible. The brand’s average price fell 15.0% YoY alongside a 15.4% YoY sales increase in Edible, indicating unit expansion offsetting price compression; the month-over-month sales dip of 1.8% against an unchanged category mix of 100.0% suggests short-term softness confined to volume rather than portfolio shifts. The thesis is that a pure-play Edible posture amplified price-to-volume trade-offs, implying resilience to mix drag but vulnerability to intra-category seasonality and pricing pressure.

Positioning-wise, Space Gem’s 21 rank in California Edibles, paired with a 15.4% YoY category sales lift and a 15.0% YoY price decrease, implies the brand is competing on accessible price points to gain or defend shelf presence while ceding per-unit revenue. The 13.3% YoY brand growth against a 1.8% MoM contraction signals momentum driven by price-led velocity that may not consistently overcome month-to-month demand noise; with 100.0% category concentration, maintaining or improving rank 21 depends on sustaining double-digit volume growth or easing price cuts to stabilize revenue per unit. The thesis is that Space Gem’s single-category focus positions it as a value-velocity player in Edibles, trading margin for share and requiring careful price calibration to progress from rank 21 amid ongoing price compression.

Competitive Landscape

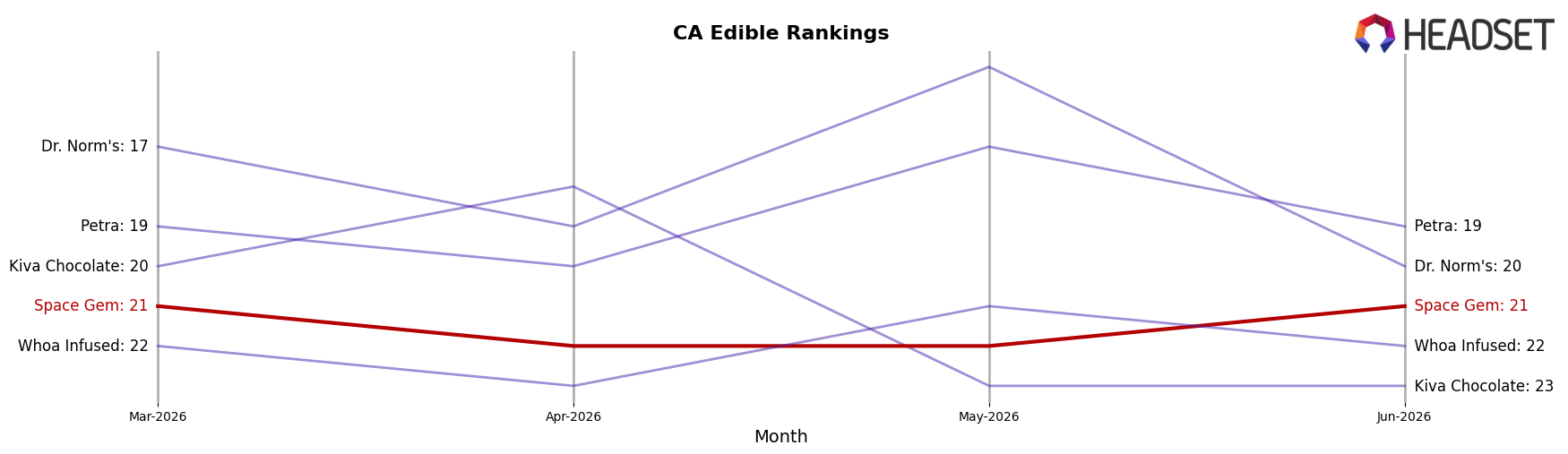

Space Gem sits at rank #21 in California Edible for June 2026, improving 1 position from #22 year over year, while holding flat versus March 2026 at #21; that stability contrasts with Wyld holding #1 despite a -1.9% year-over-year sales change and Good Tide fixed at #5 alongside a 28.5% year-over-year sales increase. Space Gem’s peak at #18 in October 2024 places it 3 ranks above the current #21, and the brand’s zero-rank movement over the last three months versus Kanha / Sunderstorm holding #3 with a 10.9% year-over-year gain suggests that share is being defended rather than expanded. The pattern implies a plateau: incremental rank gains year over year (+1) without intra-quarter uplift, while top-5 competitors are either growing double digits or absorbing minor declines, indicating Space Gem must convert stability into advancement to re-approach the #18 peak.

Notable Products

Vibrant Focus Sativa Sweet Cherry + Lemonade Mini Gems Gummies 20-Pack (100mg) posted the steepest month-over-month decline in June 2026 at -25.7%, sliding to rank 6 while top-two SKUs fell a milder -1.3% at rank 1 and -1.1% at rank 2, implying a pivot away from newer mini formats toward entrenched leaders. Flying Saucer -Sour Tangerine Gummy (100mg) at rank 3 dropped -8.1% and Sour Assorted Space Drops Gummies 10-Pack (100mg) at rank 5 fell -8.6%, yet Vitality - Hybrid Sour Lime + Lemon Boost Gummies 20-Pack (100mg) in rank 10 grew +13.9%, suggesting shoppers trimmed secondary flavors but still trialed function-led line extensions. With eight of the top ten SKUs in the Space Drops and Flying Saucer gummy families, concentration remains high even as the CBD/THC 1:1 Assorted Rainbow Flavored SpaceDrops Gummies 10-Pack (50mg CBD, 50mg THC) rose +29.1% to rank 7, indicating wellness-leaning ratios can gain share within the same gummy core. The pattern implies Space Gem’s commercial direction is consolidating around classic gummy platforms while selectively nurturing differentiated formats, with room to re-evaluate mini gems positioning and flavor breadth.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.