Jul-2026

Sales

Trend

6-Month

Product Count

SKUs

Avg Price

YoY Sales Change

YoY Price Change

Where to Buy

Punch Extracts / Punch Edibles is stocked at 828 licensed dispensaries across California, Oklahoma, and 4 other states, 678 of them in California, with the deepest coverage in Los Angeles, San Francisco, San Jose, Sacramento, and San Diego. Search by ZIP code or city below to find the closest one, or filter by product type if you are after a specific format.

Market Insights Snapshot

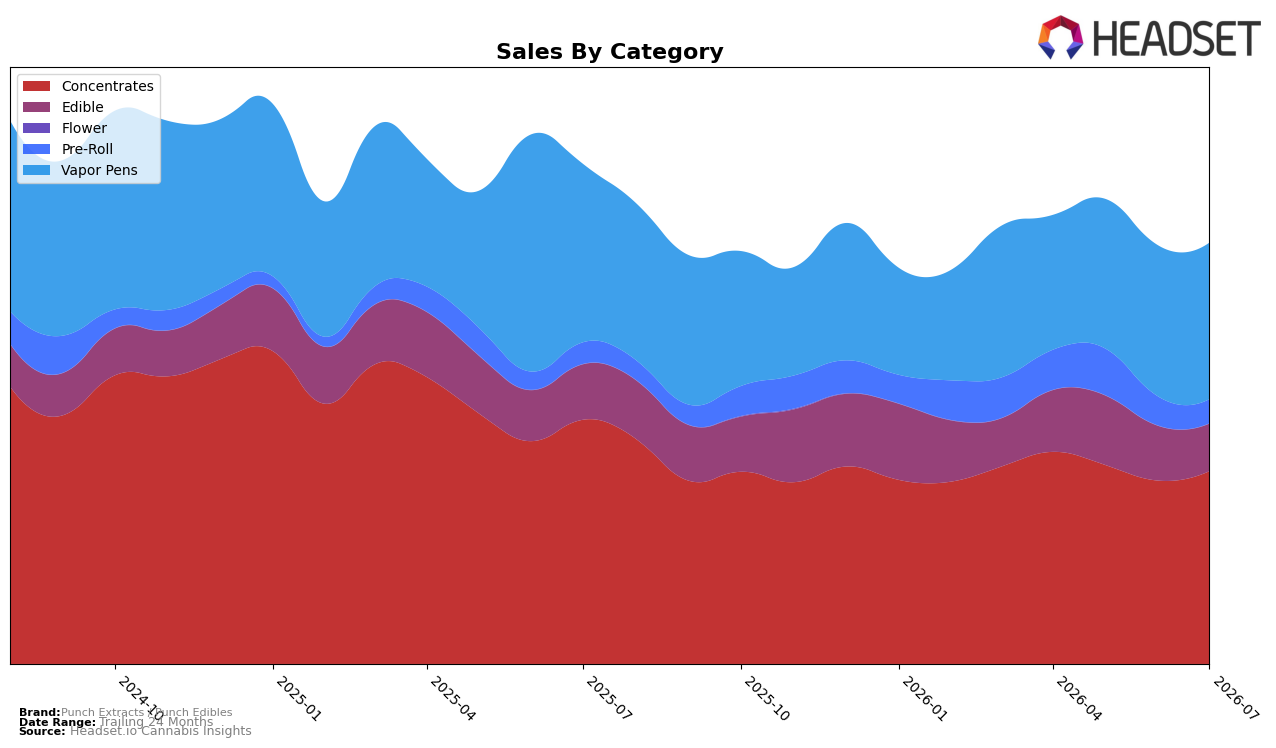

Punch Extracts / Punch Edibles concentrated its July 2026 revenue in Concentrates at 45.85% share with a 5.15% month-over-month uptick despite a 21.09% year-over-year decline, while Vapor Pens held 37.21% share with 3.58% MoM growth and a 12.22% YoY drop. Edible contracted to 11.26% share with a 13.25% MoM fall and a 14.36% YoY decline, and Pre-Roll sat at 5.68% share after a 17.29% MoM pullback but an 11.46% YoY increase. With the brand ranked #4 in Concentrates in California and average price edging down 0.39% YoY to $17.56, the pattern implies a tilt toward higher-ticket inhalables regaining monthly momentum while legacy edible volumes recede, concentrating competitive exposure in the category where the brand already sits inside the top five.

The simultaneous MoM gains in Concentrates (+5.15%) and Vapor Pens (+3.58%) alongside Edible’s double-digit MoM decline (-13.25%) imply a positioning that leans into potency-forward, fast-turn formats rather than value-driven confections, even as total brand sales fell 15.78% YoY and 19.21% over 24 months. Given Pre-Roll’s YoY rise of 11.46% but sharp MoM drop of 17.29%, the brand’s secondary formats are volatile and unlikely to offset the core, so sustaining a #4 Concentrates rank in California will depend on converting the recent monthly lift into share capture while keeping price discipline near the 0.39% YoY decrease to prevent further erosion from the 14.36% YoY edible contraction.

Competitive Landscape

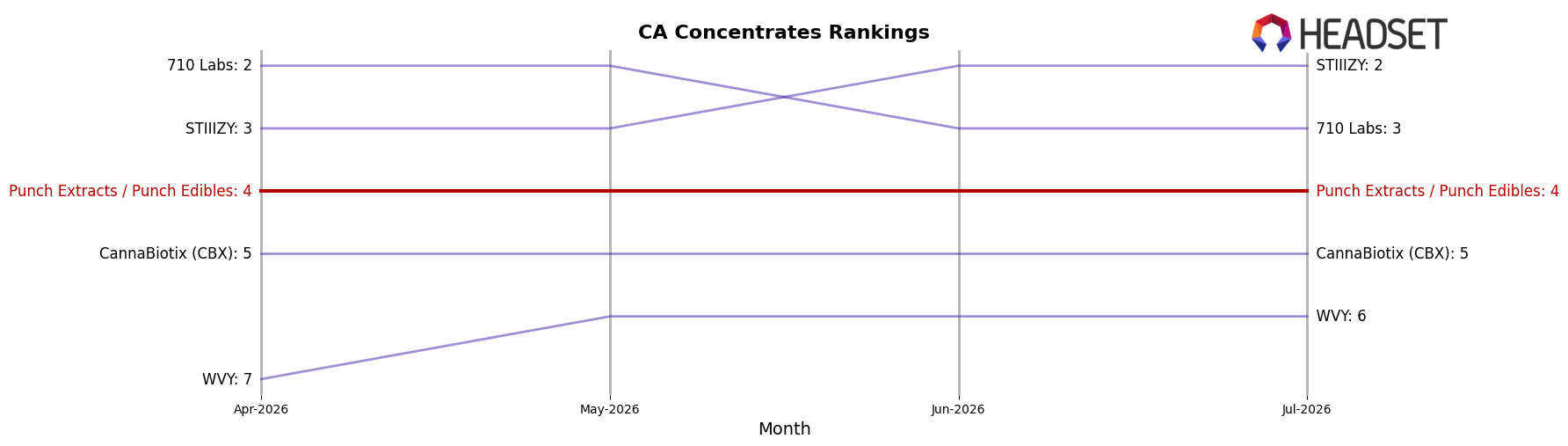

Punch Extracts / Punch Edibles sits at rank #4 in California Concentrates in July 2026, down 1 position from #3 year over year, and flat versus April 2026 with no upward movement from #4, while its historical peak was #2 in April 2025. Competitively, Raw Garden holds #1 with a 14.2% year-over-year sales increase and 710 Labs moved up from #4 to #3 with a 15.9% year-over-year lift, placing Punch Extracts / Punch Edibles on the wrong side of a 1-rank gap that has widened over the past 12 months. Against the broader field, STIIIZY remains #2 despite just a 1.4% year-over-year increase, while CannaBiotix (CBX) sits at #5 yet posted a 37.0% year-over-year rise, suggesting pressure from both above and below in the rankings. The pattern implies that without an offsetting share gain or mix shift, the slide from #3 to #4 amid competitors’ double-digit growth will likely entrench Punch Extracts / Punch Edibles in the #4 slot rather than return it toward the #2 peak.

Notable Products

The Z Distillate Cartridge (1g) posted the steepest decline, down 12.2% month over month and sitting at rank 7, while Blue Z Distillate Cartridge (1g) also slipped 14.8% at rank 9, signaling softness within Z-labeled SKUs. In contrast, Dulce Fresca Distillate Cartridge (1g) climbed 38.4% to rank 1 and Blue Dream Distillate Cartridge (1g) rose 42.5% to rank 2, and six of the top ten are Vapor Pens, concentrating mix away from confections. Edibles were steadier with Peach Mango Gummies 10-Pack (100mg) up 29.5% at rank 4 and two additional gummy SKUs inside the top ten, while Mimosa Distillate Cartridge (1g) dipped 4.0% at rank 6. The pattern implies a pivot toward high-velocity pen flavors leading the lineup while Z variants are deprioritized, with gummies providing a secondary, lower-volatility ballast.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.