Jun-2026

Sales

Trend

6-Month

Product Count

SKUs

Avg Price

YoY Sales Change

YoY Price Change

Market Insights Snapshot

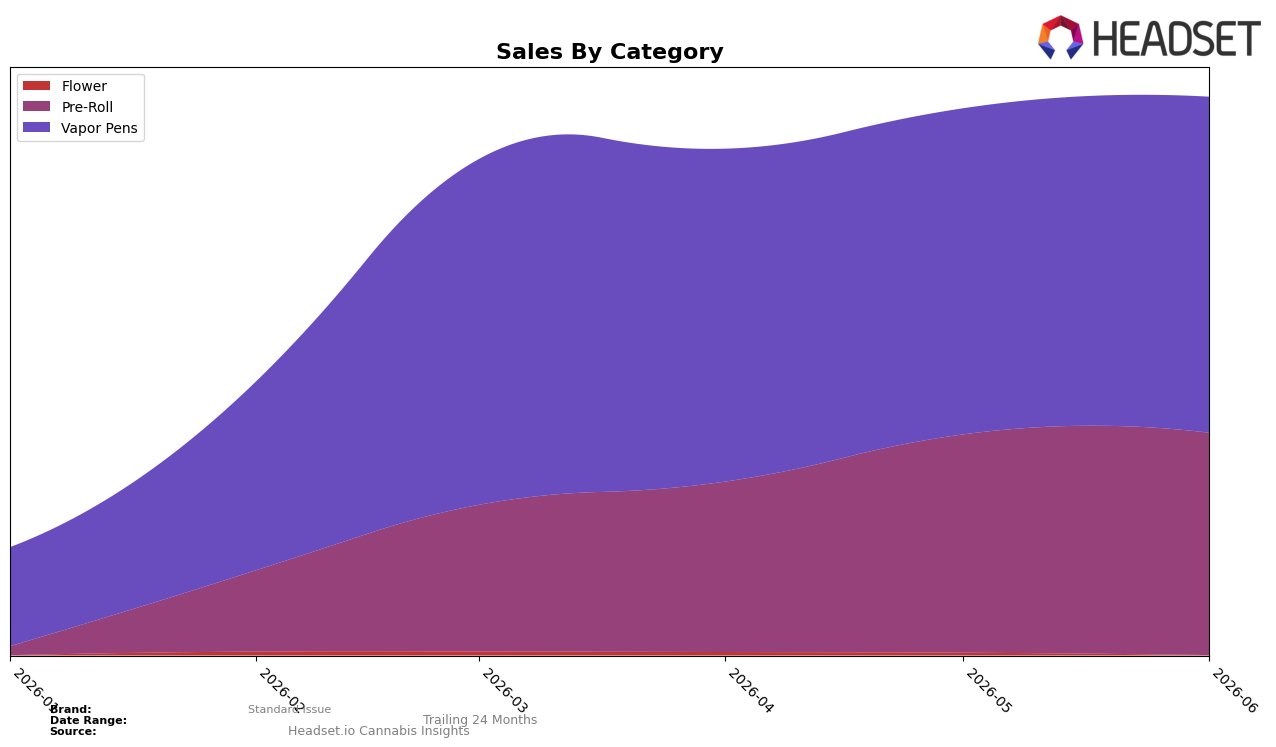

In June 2026, Standard Issue concentrated 59.49% of sales in Vapor Pens and 39.62% in Pre-Roll, with Flower at 0.89% share; month over month, Vapor Pens grew 2.99% while Pre-Roll rose 1.81% and Flower fell 31.89%. The average price spread reinforces this tilt, with Vapor Pens at $27.27 versus Pre-Roll at $19.00 and Flower at $26.48, indicating the 2.99% MoM lift is occurring where price points are highest while the 31.89% MoM decline is isolated to a sub‑1% share tail. The pattern implies Standard Issue is consolidating around two categories that together hold 99.11% share, with incremental growth favoring the premium‑priced Vapor Pens while de‑prioritizing Flower.

Given this mix, positioning skews to inhalable convenience anchored by Vapor Pens’ 59.49% share and a secondary Pre-Roll base at 39.62%, with sequential gains of 2.99% and 1.81% suggesting reliability in repeat purchase formats rather than breadth. With Vapor Pens ranked 4 in British Columbia, the brand sits just outside top‑tier leadership and benefits more from deep penetration in a primary category than from diversification, implying that defending a top‑five slot will hinge on sustaining low‑single‑digit MoM growth in Vapor Pens while accepting volatility in the 0.89% Flower niche.

Competitive Landscape

Standard Issue is ranked #6 in AB Vapor Pens in June 2026, slipping 1 position from #5 in March 2026 while also dropping 1 spot versus its 3-month rank of #5; the brand’s peak rank remains #5 in March 2026, indicating a minor step down as category leaders reshuffle. In the same window, Spinach held #1 year over year and posted a 43.97% sales increase, while General Admission sits at #5 with a -14.82% sales decline year over year, suggesting that Standard Issue’s move from #5 to #6 aligns more with share consolidation at the top than broad-based pressure from mid-pack rivals. The pattern implies a stall near the #5–#6 boundary, where modest relative underperformance against leaders and volatility among immediate neighbors could translate into sustained mid-tier positioning unless momentum shifts.

Notable Products

The steepest decline sets the tone: Strawberry Lemonade Distillate Infused Pre-Roll 2-Pack (1g) fell 10.4% month over month to rank 6 while Sour Raspberry Distillate Cartridge (1g) dropped 13.2% to rank 4, indicating pullback concentrated in flavored line extensions rather than across-the-board weakness. Offsetting that, Watermelon Infused Pre-Roll 5-Pack (2.5g) gained 4.3% at rank 8 and Peach Distillate Disposable (1g) rose 3.8% at rank 10, and five of the top ten are Pre-Roll SKUs, signaling mix resilience anchored by multi-pack Pre-Rolls even as single-flavor variants churn.

At the top, Bing Cherry Distillate Infused Pre-Roll 2-Pack (1g) held rank 1 despite a 1.2% dip, while Strawberry Lemonade Distillate Cartridge (1g) slid 7.5% at rank 2 and Wild Berry Distillate Cartridge (1g) was nearly flat at -0.9% at rank 3, pointing to tighter competition inside Vapor Pens than in Pre-Rolls. With Vapor Pens occupying ranks 2–4 and 9–10 but mixed MoM trajectories and only one SKU showing a positive pen move, June 2026 indicates Standard Issue is leaning toward Pre-Roll-led revenue stability rather than pen-led expansion, with a logical near-term focus on defending top Pre-Roll positions while pruning underperforming flavors.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.