Jul-2026

Sales

Trend

6-Month

Product Count

SKUs

Avg Price

YoY Sales Change

YoY Price Change

Where to Buy

Stingers is stocked at 282 licensed dispensaries across Washington, Massachusetts, and 3 other states, 171 of them in Washington, with the deepest coverage in Seattle, Tacoma, Spokane, Olympia, and Everett. Search by ZIP code or city below to find the closest one, or filter by product type if you are after a specific format.

Market Insights Snapshot

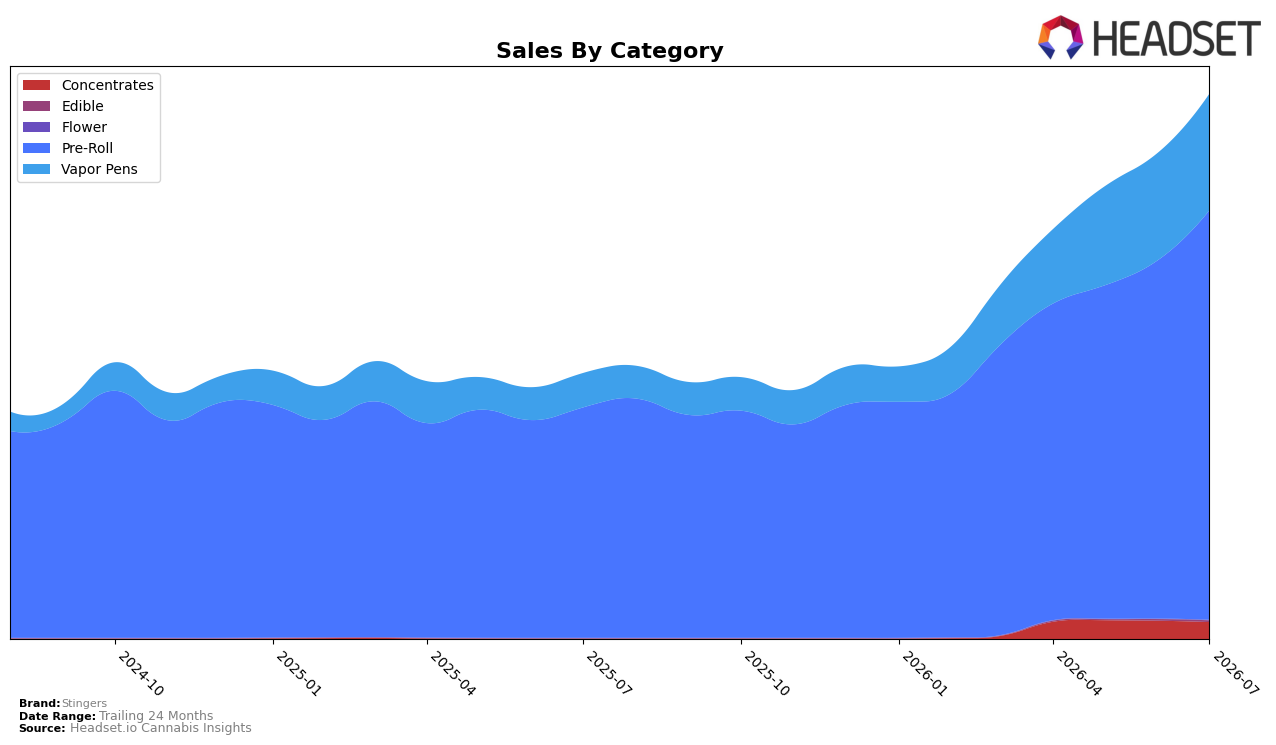

In July 2026, Stingers concentrated 75.27% of sales in Pre-Roll, rising 14.24% month over month and 77.81% year over year, while Vapor Pens expanded to 21.39% share with 8.52% MoM and 241.55% YoY growth. Smaller lines diverged: Concentrates held 3.05% share with a 7.59% MoM decline, Edible sat at 0.25% share with an 8.21% MoM gain, and Flower remained marginal at 0.03% share despite a 150.28% MoM jump. Average price increased 17.74% YoY to $9.28, and Pre-Roll averaged $8.41 versus $13.40 in Vapor Pens. The pattern implies a two-engine portfolio where Vapor Pens’ triple-digit YoY growth reduces overreliance on Pre-Roll, but the 6th rank in Washington Pre-Roll signals that near-term volume still hinges on maintaining price-accessible Pre-Roll while nurturing higher-price Vapor Pens.

With Pre-Roll still three times the share of Vapor Pens (75.27% vs 21.39%) yet Vapor Pens compounding faster (+241.55% YoY vs +77.81% YoY), mix shift risk is manageable if MoM momentum persists (+14.24% in Pre-Roll versus +8.52% in Vapor Pens). The 17.74% YoY brand-wide price lift alongside Pre-Roll’s lower average price ($8.41) suggests pricing headroom remains anchored in Vapor Pens’ higher average ($13.40), while the 7.59% MoM dip in Concentrates and 8.21% MoM rise in Edible indicate peripheral categories will not materially change positioning near term. The implication is a migration path from a value-leaning Pre-Roll base toward a premium-adjacent mix via Vapor Pens, keeping Stingers competitive at rank 6 in Washington Pre-Roll while using pen pricing to lift blended margins.

Competitive Landscape

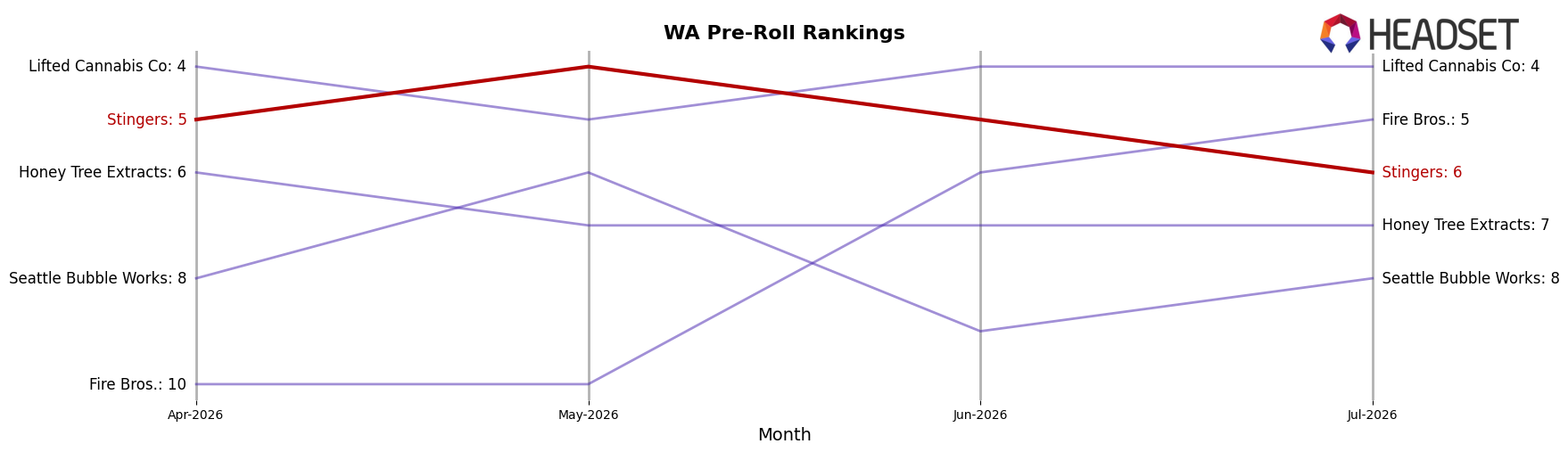

Stingers sits at rank #6 in WA Pre-Roll in July 2026, down 1 position year over year from #5, with a 1-rank slide since April 2026 even after peaking at #4 in May 2026; in contrast, Ooowee climbed from #2 to #1 with 59.5% YoY sales growth, while Fire Bros. moved from #11 to #5 on 52.0% YoY growth, indicating rivals are gaining share faster than Stingers. Over the last three months Stingers eased from #5 to #6 as Lifted Cannabis Co advanced from #7 to #4 with 30.0% YoY growth and Phat Panda slipped from #1 to #2 despite 1.2% YoY growth, pointing to a mid-pack squeeze where incremental rank losses for Stingers translate into reduced visibility against upwardly mobile competitors.

Notable Products

Wedding Cake Infused Pre-Roll (1g) posted the standout move in July 2026 with a 118.9% month-over-month surge to $41,429 and rose to rank 1, while 9lb Hammer Infused Pre-Roll 2-Pack (1g) fell 23.2% and sits at rank 7. Grape Ape Infused Pre-Roll (1g) climbed 40.6% at rank 4, and Pineapple Express Distillate Cartridge (1g) advanced 27.7% at rank 6, indicating gains are not confined to one SKU. With eight of the top ten sitting in the Pre-Roll category and two Vapor Pens at ranks 6 and 9, the mix concentrates demand in infused Pre-Rolls even as Vapor Pens add incremental lift. The pattern implies Stingers is leaning into high-potency infused formats for velocity while using a limited Vapor Pen presence to diversify without diluting focus.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.