Jun-2026

Sales

Trend

6-Month

Product Count

SKUs

Avg Price

YoY Sales Change

YoY Price Change

Market Insights Snapshot

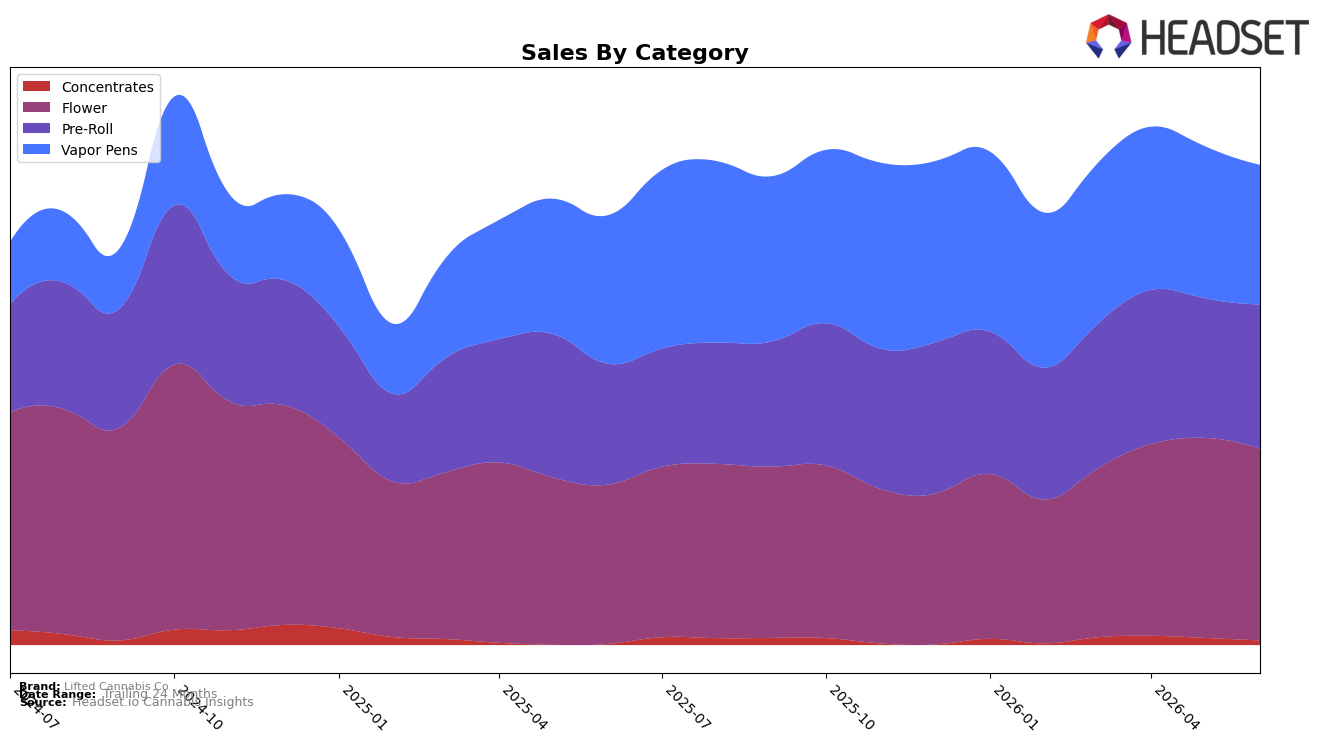

Lifted Cannabis Co concentrated nearly two-thirds of June 2026 sales in Flower and Pre-Roll, with Flower at 37.76% share (ranked 3 in Washington) and Pre-Roll at 29.33% share; YoY, Flower grew 17.93% and Pre-Roll rose 16.80%, while MoM the same categories diverged at -3.79% and +2.92% respectively. Vapor Pens held 28.47% share but declined -5.41% YoY and -7.30% MoM, and Concentrates at 4.43% share rose 16.46% YoY but fell -9.29% MoM; this mix implies the June 2026 topline was carried by combustibles despite headwinds in inhalable extracts.

The shift toward Flower and Pre-Roll, alongside a -7.30% MoM drop in Vapor Pens and a -9.29% MoM dip in Concentrates, suggests Lifted Cannabis Co gained relative price-value traction in combustibles while ceding momentum in oil-based formats; the 1.18% YoY increase in average price and a 17.93% YoY Flower lift indicate pricing latitude where the brand ranks 3 in Washington Flower. With Vapor Pens now contributing nearly parity with Pre-Roll at 28.47% vs. 29.33% share but posting a -5.41% YoY slide, June 2026 positioning tilts toward higher-volume, lower-ticket units that can stabilize share in Washington while the brand rebalances assortment away from softening oil SKUs.

Competitive Landscape

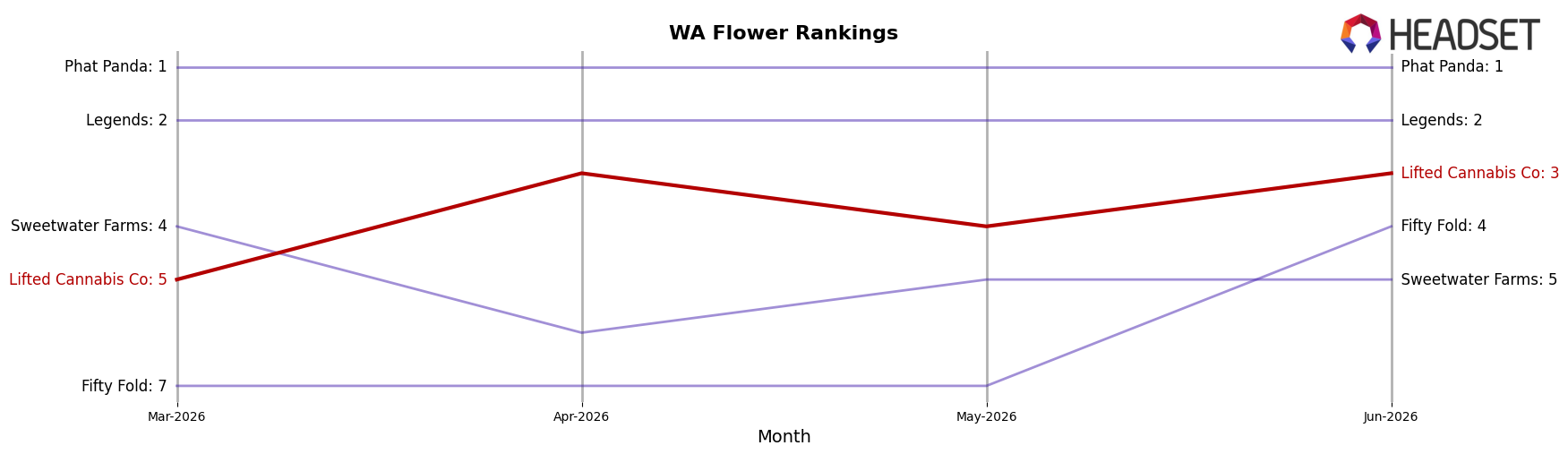

Lifted Cannabis Co sits at rank #3 in Washington Flower in June 2026 after rising 5 positions year over year from #8, and it also climbed 2 spots since March 2026 when it was #5; this June 2026 position matches its peak rank of #3, indicating upward momentum concentrated in the last quarter. In directional context, Phat Panda held #1 both year over year (#1 to #1) while growing sales 16.6%, and Legends stayed flat at #2 (from #2 to #2) despite a 19.8% sales decline, whereas Fifty Fold improved from #9 to #4 on 22.3% sales growth, tightening the gap directly behind Lifted Cannabis Co. The pattern implies Lifted Cannabis Co’s rank trajectory—+5 ranks YoY to a peak-tying #3—positions it as the current challenger to #2 in the near term while needing to defend against a fast-rising #4 competitor.

Notable Products

SugarStix - Permanent Marker Infused Pre-Roll (1g) posted the largest month-over-month surge at +66.2% to rank 4, while Blue Lobster SugarStix Infused Pre-Roll (1g) fell -19.3% to rank 7, indicating volatility within infused pre-rolls. Wedding Cake (3.5g) retained rank 1 despite a -12.1% decline, whereas Wedding Cake Pre-Roll (1g) slid -40.7% to rank 8, signaling divergence between the flagship flower and its pre-roll extension. With seven of the top ten being SugarStix infused pre-rolls, the portfolio is tilting toward infused formats even as core flower anchors the top slot, implying Lifted Cannabis Co is consolidating around high-velocity infused SKUs while managing attrition in non-infused pre-rolls.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.