Jul-2026

Sales

Trend

6-Month

Product Count

SKUs

Avg Price

YoY Sales Change

YoY Price Change

Where to Buy

Summa Cannabis is stocked at 16 licensed dispensaries across Nevada, with the deepest coverage in Las Vegas, North Las Vegas, Henderson, Schurz, and Sparks. Search by ZIP code or city below to find the closest one, or filter by product type if you are after a specific format.

Market Insights Snapshot

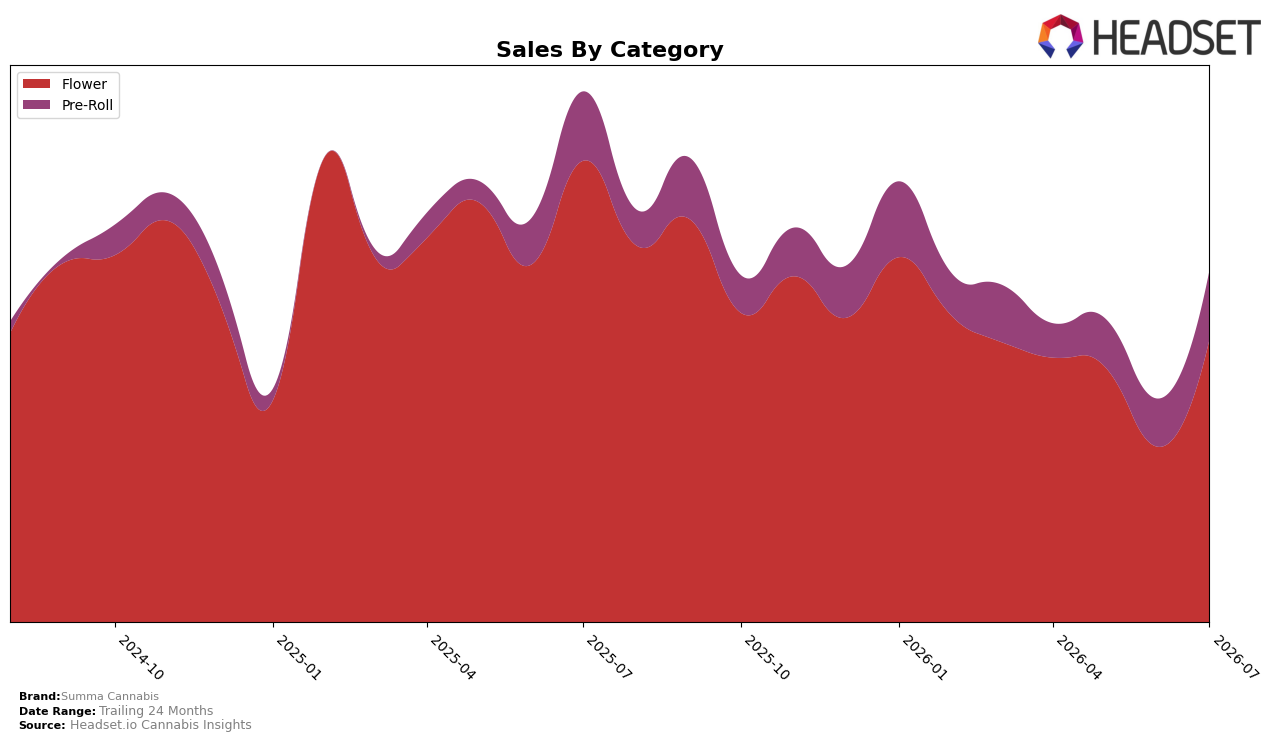

In July 2026, Summa Cannabis concentrated 78.00% of sales in Flower while 22.00% came from Pre-Roll, a skew that widened month over month as Flower grew 56.49% MoM and Pre-Roll rose 33.26% MoM, even as year over year trends diverged with Flower down 37.58% YoY and Pre-Roll essentially flat at -0.33% YoY. Despite brand sales down 31.99% YoY and an average price decline of 24.53% YoY, the category tilt favored higher-ticket Flower at an average of $25.52 versus $5.68 in Pre-Roll, signaling a tactical rebound driven by Flower volume expansion rather than Pre-Roll diversification.

This mix shift implies Summa Cannabis is anchoring positioning around Flower in Nevada, where the brand sits at rank 19 in Flower and expanded share influence through a 56.49% MoM surge even as the YoY drag of -37.58% suggests ongoing churn that the brand is offsetting with price resets of 24.53% YoY. With Pre-Roll holding 22.00% share and only -0.33% YoY change versus a 33.26% MoM lift, the brand is using Pre-Roll as a stabilizer while prioritizing Flower-led recovery, which positions it to trade rank volatility for volume capture in the near term.

Competitive Landscape

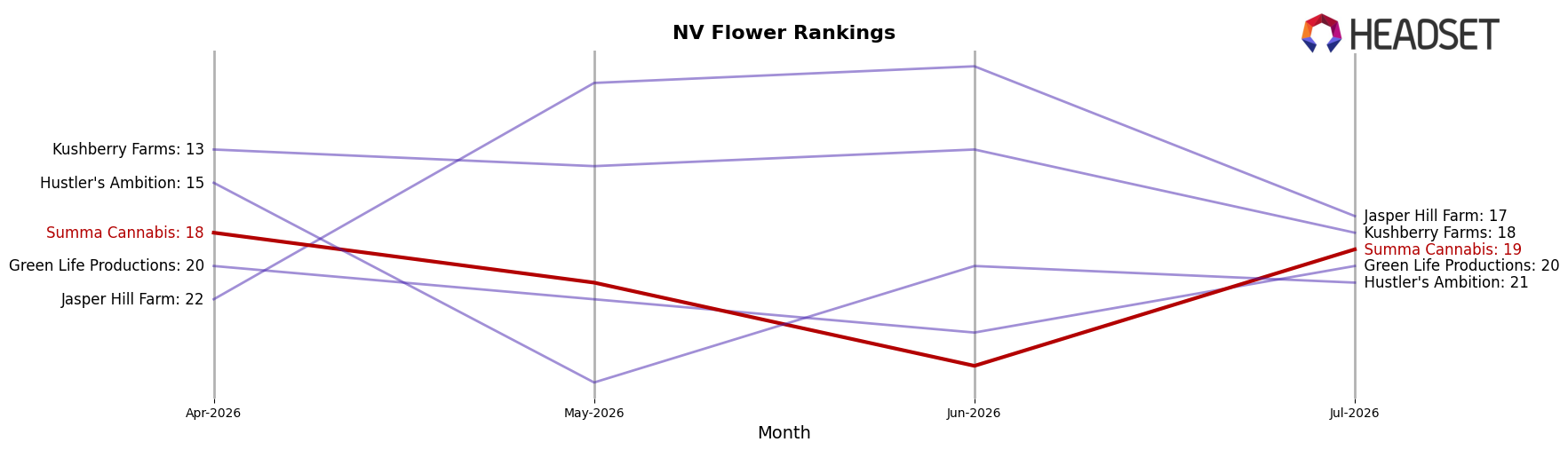

Summa Cannabis sits at rank #19 in NV Flower for July 2026, down 5 positions year over year from #14, and 1 position softer versus April 2026’s #18, while its historical peak of #11 in February 2025 remains a distant high-water mark; in contrast, STIIIZY advanced from #2 to #1 with a 31.5% year-over-year sales gain and FloraVega / Welleaf surged from #24 to #5 on 299.7% growth, whereas RYTHM slipped from #1 to #2 alongside a 12.7% decline; the combination of Summa Cannabis’s 5-rank YoY slide and minimal 1-rank quarter-over-quarter drift implies share is consolidating toward faster risers, and the current trajectory points to further erosion unless mix or distribution changes reverse the rank trend.

Notable Products

Snowball 89 Pre-Roll (1g) delivered the standout move in July 2026 with a 164% month-over-month surge to rank 1, while Rainbow Runtz X Rainbow Belts 7 Pre-Roll (1g) slid 17% to rank 7. Glitter Bomb Pre-Roll (1g) added 22% and sat at rank 4, and five of the top ten were Pre-Roll SKUs concentrated across ranks 1, 2, 4, 5, and 8. Mule Fuel (3.5g) held rank 3 despite no reported month-over-month percentage, and Flower still placed three SKUs in the top ten including Cadillac Rainbow (3.5g) at rank 9, indicating a two-pillar mix where aggressive Pre-Roll gains pull share up front while Flower anchors basket size around a single $33,270 flagship.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.