Jul-2026

Sales

Trend

6-Month

Product Count

SKUs

Avg Price

YoY Sales Change

YoY Price Change

Where to Buy

Sweet Justice is stocked at 59 licensed dispensaries across Michigan, with the deepest coverage in New Buffalo, Kalamazoo, Portage, Flint, and Grand Haven. Search by ZIP code or city below to find the closest one, or filter by product type if you are after a specific format.

Market Insights Snapshot

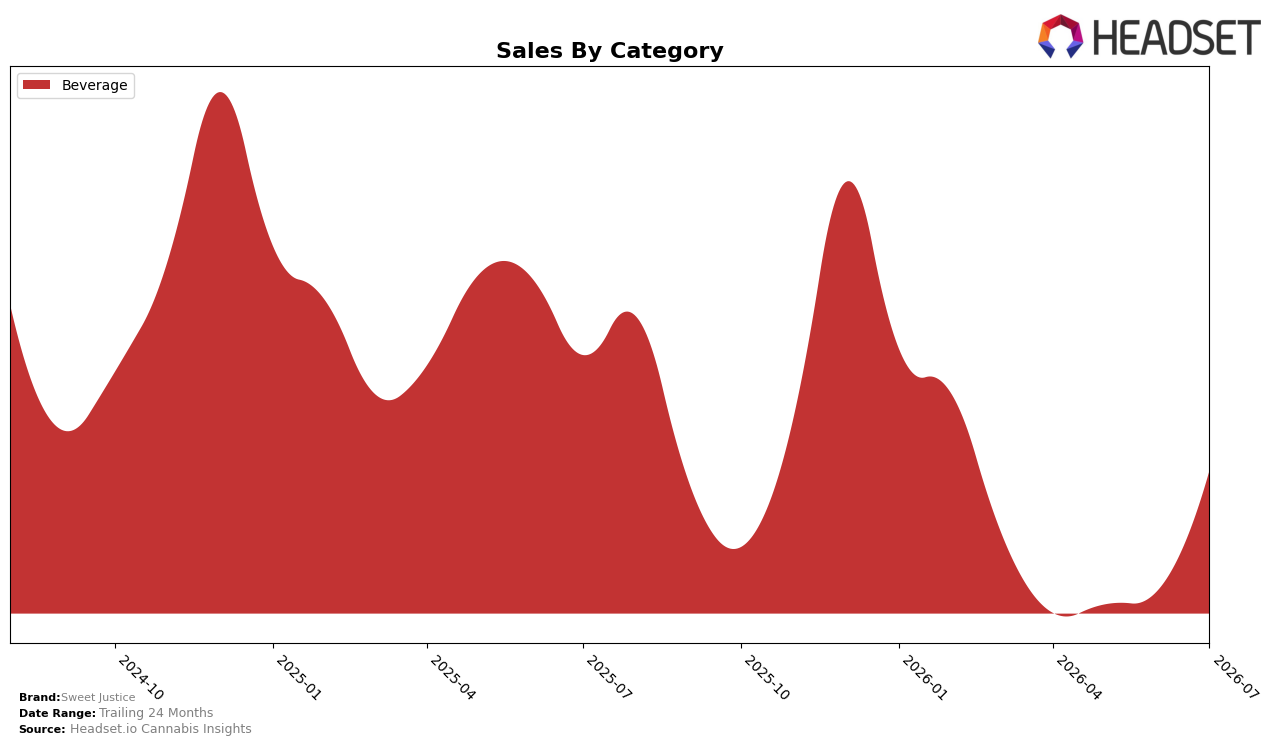

In July 2026, Sweet Justice remained entirely concentrated in Beverage, with category share at 100.0% and rank 4 in Beverage in British Columbia; year over year sales declined 11.2% while month over month sales rose 14.9%. Average price fell 2.1% YoY alongside a single-category focus, and the combination of -11.2% YoY and +14.9% MoM suggests demand is rebounding within the same lane rather than via mix expansion; this implies Sweet Justice is trading volume within Beverage rather than diversifying to offset the annual drag.

The pricing and volume pattern points to a positioning reset inside Beverage: a 2.1% YoY price decrease paired with a 14.9% MoM sales lift indicates elasticity at current price points, while the 11.2% YoY decline and a category rank of 4 in British Columbia signal room to climb the ladder. With 100.0% of revenue in Beverage and a top-market concentration in ON, the thesis is that Sweet Justice can gain share primarily through intra-category pricing-pack architecture and geographic depth, not cross-category expansion in the near term.

Competitive Landscape

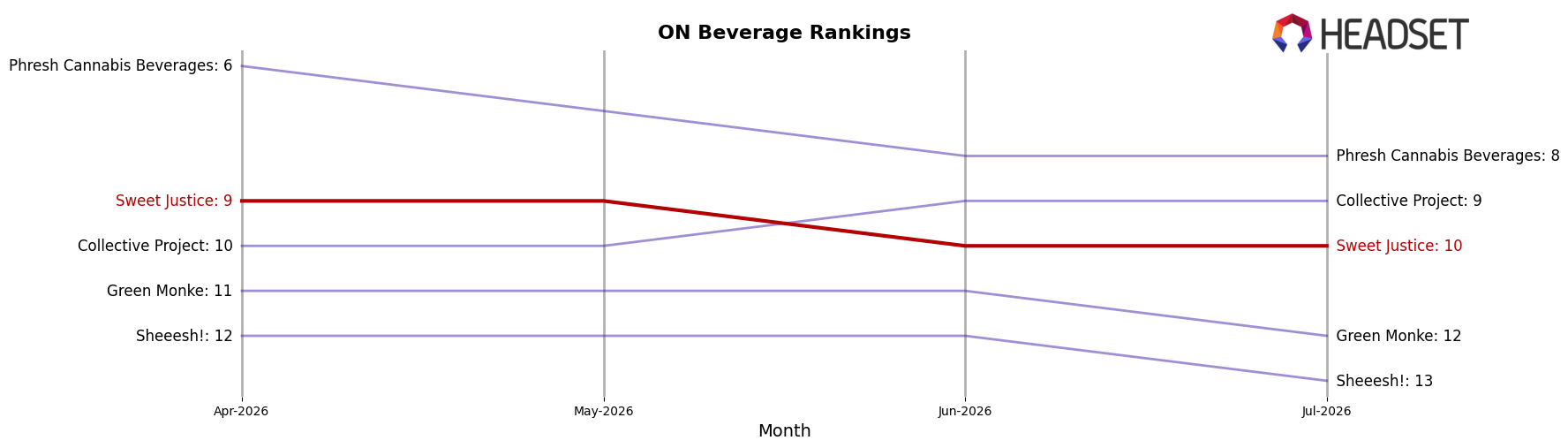

Sweet Justice sits at rank #10 in ON Beverage in July 2026, down 3 positions year over year from #7, and off 1 spot from April 2026’s #9, even after peaking at #4 in February 2026; meanwhile, Versus climbed from #3 to #1 with 18.09% year-over-year sales growth, and XMG fell from #1 to #2 alongside a 37.17% year-over-year sales decline, signaling a reshuffle at the top that Sweet Justice has not capitalized on. With Ray's Lemonade moving up from #5 to #4 on 28.70% growth and Mary Jones advancing from #8 to #5 on 56.06% growth, the brand’s slippage to #10 while peers post double-digit gains implies a trajectory toward the lower tier unless Sweet Justice reverses its relative momentum.

Notable Products

OG Cola (3.5mg THC, 355ml) posted the largest month-over-month move in July 2026 with a 100.0% surge to rank 7, while CBD/THC 1:2 Pacific Island Punch Fruit Drink (5mg CBD, 10mg THC, 355ml ) fell 20.1% at rank 9. At the top, THC/CBG 1:1 OG Root Beer Free Soda (10mg THC, 10mg CBG, 355ml) rose 19.2% to hold rank 1 as Cherry Cola (10mg THC, 12oz, 355ml) advanced 30.5% at rank 3, consolidating a cola-led ladder where eight of the top ten are Beverage SKUs. This pattern implies Sweet Justice is concentrating velocity in familiar cola formats while pruning or deprioritizing niche fruit variants that are showing negative momentum.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.