Jul-2026

Sales

Trend

6-Month

Product Count

SKUs

Avg Price

YoY Sales Change

YoY Price Change

Market Insights Snapshot

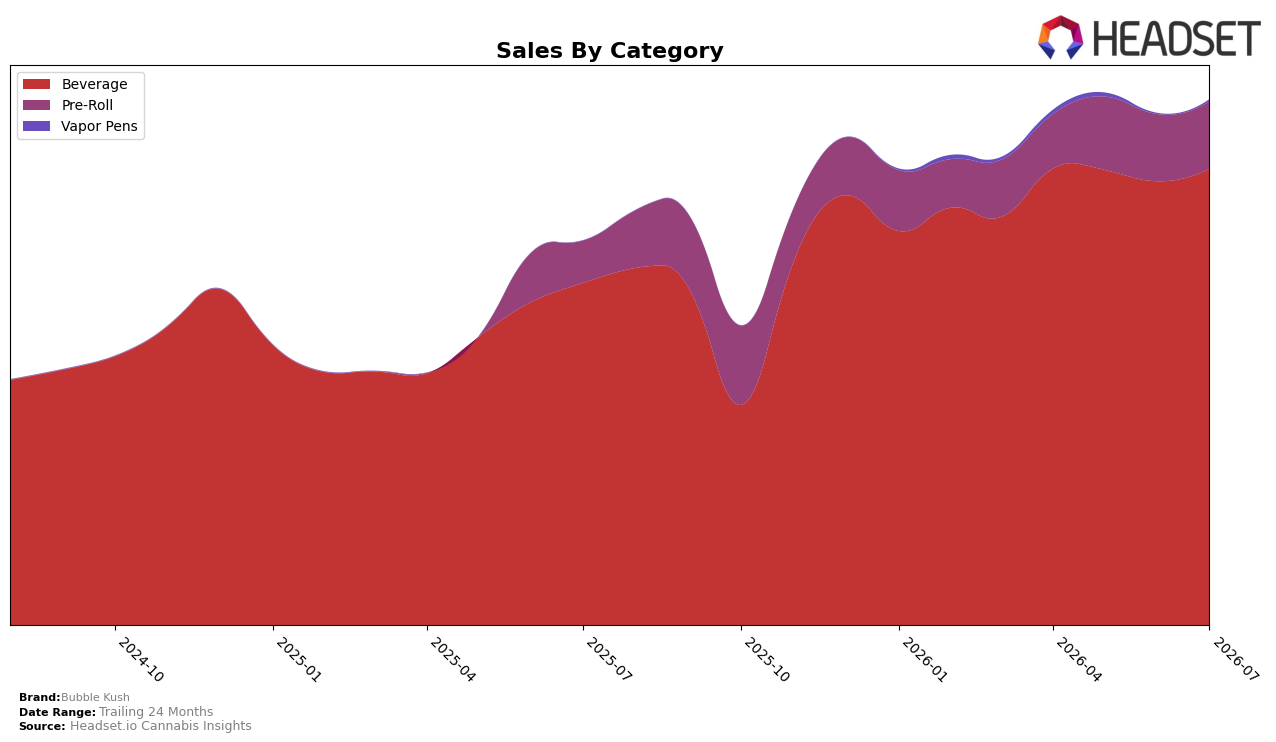

In July 2026, Bubble Kush concentrated 86.87% of sales in Beverage, up 2.79% month over month while growing 33.31% year over year, with Pre-Roll holding 12.79% share on 0.74% MoM and 60.16% YoY growth. Vapor Pens remained a sliver at 0.34% share but surged 126.58% MoM from a low base, with no year-ago comp available; meanwhile, the brand’s overall YoY sales growth of 36.71% outpaced Beverage’s 33.31%, indicating incremental lift from outside the core. Bubble Kush ranked 2 in Beverage in British Columbia, suggesting category-scale reach is intact even as mix broadens; the thesis is that Beverage remains the demand anchor while Pre-Roll expansion is adding marginal growth without diluting category focus.

The mix shifts imply Bubble Kush is reinforcing a Beverage-led positioning while testing adjacencies that lift total growth above the Beverage baseline: Beverage share at 86.87% alongside 2.79% MoM growth keeps the brand anchored for velocity, while Pre-Roll’s 60.16% YoY on 12.79% share signals an effective secondary entry that could cushion seasonal Beverage swings. With rank 2 in Beverage in British Columbia and overall YoY at 36.71% vs. Beverage’s 33.31%, the brand is extracting incremental contribution from Pre-Roll and early-stage Vapor Pens, implying a strategy to defend Beverage leadership while building optionality that can reallocate emphasis if Pre-Roll sustains double-digit share and Vapor Pens maintains triple-digit MoM momentum.

Competitive Landscape

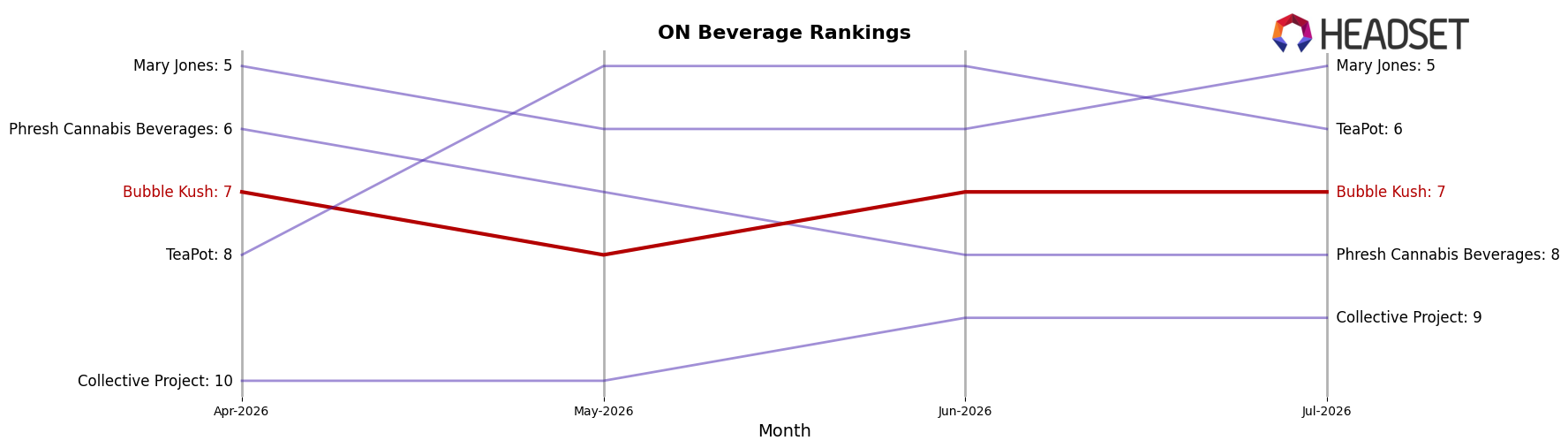

Bubble Kush sits at rank #7 in ON Beverage in July 2026, up 2 positions from #9 in July 2025, and matching its peak rank of #7 in July 2026 while holding flat versus April 2026 at #7; meanwhile, Versus climbed from #3 to #1 and XMG fell from #1 to #2 with a -37.17% year-over-year sales change, indicating that Bubble Kush’s steady two-rank YoY rise amid top-tier reshuffling points to incremental share capture through stability rather than breakout momentum.

Notable Products

Wandz Puffz - Guava Gaz Infused Pre-Roll 5-Pack (2.5g) plunged 50.56% month over month to rank 10, while Rocket Fizz Soda (10mg THC, 355ml) fell 28.16% at rank 5, signaling a bifurcation between stable beverages and volatile tail SKUs. At the top, Root Beer Beverage (10mg THC, 355ml) held rank 1 with a 5.26% lift and Orange Soda (10mg THC, 355ml) at rank 2 climbed 17.40%, together anchoring the category with one beverage above $278,653 in July 2026. In Pre-Roll, Wandz Fruitz - Cobra Blood Distillate Infused Pre-Roll 5-Pack (2.5g) surged 57.53% at rank 8 even as Wandz Fruitz - Dragonfruit Hibiscus Infused Pre-Roll 5-Pack (2.5g) dropped 15.90% at rank 7, and four of the top ten are Pre-Roll SKUs indicating a split portfolio. The pattern implies Bubble Kush is consolidating revenue in a beverage-led core while selectively testing Pre-Roll innovation that carries higher variance and requires tighter SKU governance.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.