Jul-2026

Sales

Trend

6-Month

Product Count

SKUs

Avg Price

YoY Sales Change

YoY Price Change

Where to Buy

The Happy Cannabis is stocked at 90 licensed dispensaries across Washington, Michigan, and 4 other states, 29 of them in Washington, with the deepest coverage in Seattle, Olympia, Tacoma, Des Moines, and Rochester. Search by ZIP code or city below to find the closest one, or filter by product type if you are after a specific format.

Market Insights Snapshot

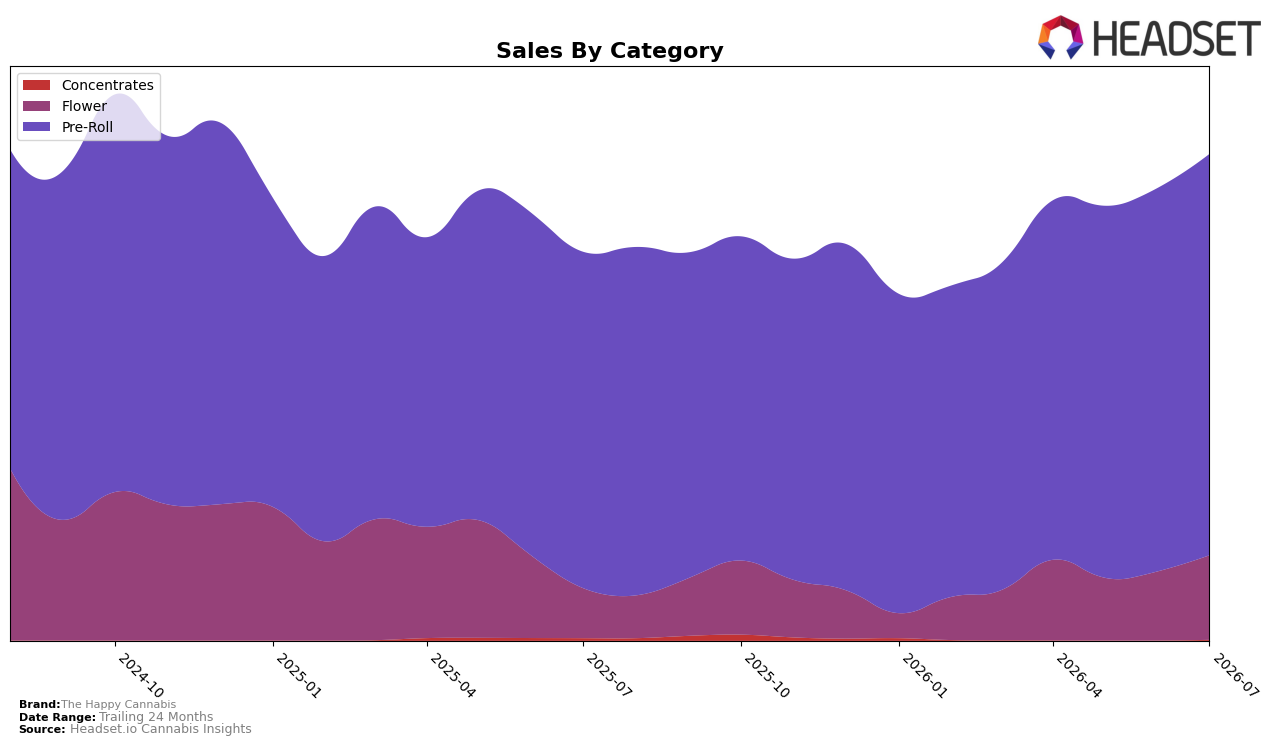

The Happy Cannabis concentrated 82.54% of July 2026 sales in Pre-Roll, with Flower at 17.33% and Concentrates at 0.13%, indicating a mix tightly skewed to a single category while a secondary foothold expands. Pre-Roll grew 19.33% year over year and 4.63% month over month, while Flower accelerated at 69.60% YoY and 22.36% MoM; in contrast, Concentrates fell 72.01% YoY with no measurable month-over-month signal. With average price down 7.07% YoY to $12.49 and Pre-Roll pricing at $11.48 versus Flower at $21.39, the volume-weighted shift and price architecture imply a strategy that trades higher ticket per unit in Flower for wider reach via Pre-Roll. The thesis is that July 2026 marks reinforcement of a Pre-Roll-led core while a faster-growing Flower segment starts to rebalance risk away from single-category dependence.

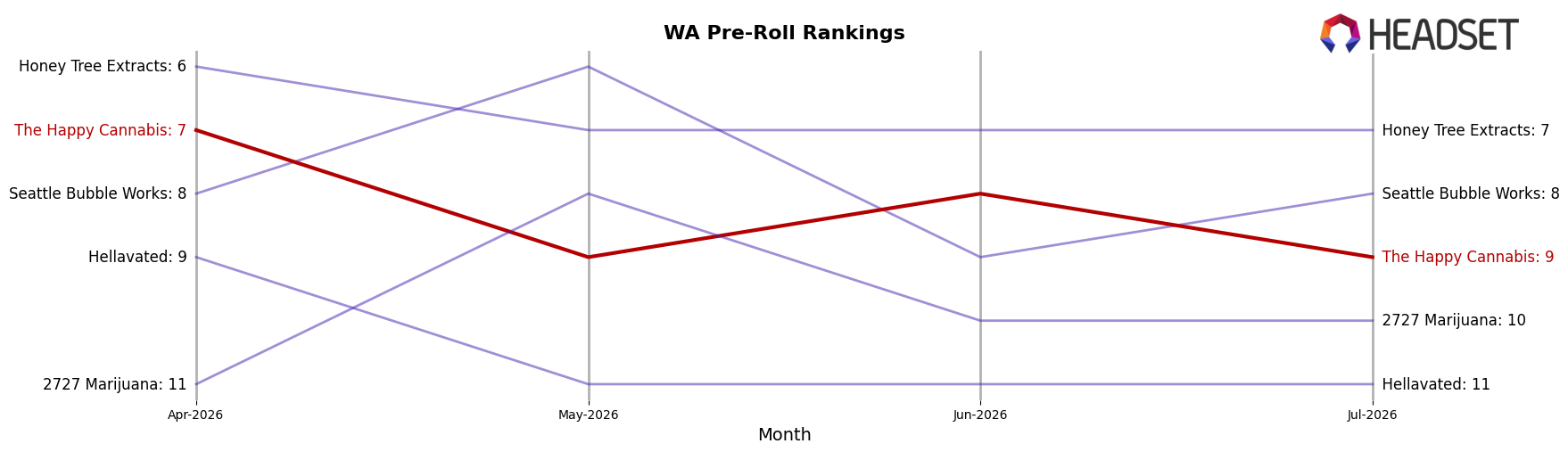

Holding rank 9 in Pre-Roll in Washington alongside 4.63% MoM growth suggests headroom tied to incremental distribution or assortment depth rather than price-driven share capture, since category-level pricing sits below the brand’s overall average. The 69.60% YoY surge and 22.36% MoM step-up in Flower, despite only 17.33% share, implies a pipeline that can convert shelf gains into mix shift without undermining the Pre-Roll franchise; conversely, the 72.01% YoY decline in Concentrates limits cross-category halo. The implication is that near-term positioning should emphasize dual-lane momentum—protecting a rank-9 Pre-Roll beachhead while compounding Flower’s faster trajectory—to diversify revenue while keeping price architecture coherent.

Competitive Landscape

In Washington Pre-Roll, The Happy Cannabis sits at rank 9 in July 2026, a 1-position improvement from rank 10 year over year, but a 2-position slide from rank 7 in April 2026, indicating momentum cooled after a spring peak. Competitors moved more decisively: Ooowee climbed from rank 2 to rank 1 while growing sales 59.5% year over year, and Fire Bros. jumped from rank 11 to rank 5 alongside a 52.0% sales increase, whereas The Happy Cannabis declined 2 ranks since April 2026 despite a 1-rank YoY gain. The pattern implies The Happy Cannabis is holding its place against the broader field but ceding relative momentum to faster-rising leaders, so without share-accretive moves it risks drifting further from its April 2026 peak.

Notable Products

Gelato Cake Pre-Roll 2-Pack (1g) delivered the standout movement in July 2026 with a +54.7% month-over-month surge that pushed it to rank 2, while Zig-A-Zig Ah Shatter Infused Pre-Roll 2-Pack (1.2g) slipped 4.3% and held at rank 5, indicating consumer trade-up within the same format. Sex On The Beach Infused Pre-Roll 2-Pack (1.2g) grew 16.2% to retain rank 1, and Laughing Gas Infused Pre-Roll 2-Pack (1g) climbed 32.3% to rank 4, while King Louie Pre-Roll 2-Pack (1g) advanced 24.1% to rank 3; this rank consolidation at the top implies momentum concentrating in a few SKUs. With all top-10 entries in the Pre-Roll category and the Gelato Cake Pre Roll 5-Pack (2.5g) up 37.9% at rank 8, the mix tilts toward multi-pack and infused options, signaling a strategy centered on basket-building and potency-driven differentiation.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.