Jul-2026

Sales

Trend

6-Month

Product Count

SKUs

Avg Price

YoY Sales Change

YoY Price Change

Where to Buy

2727 Marijuana is stocked at 142 licensed dispensaries across Washington and Oregon, 141 of them in Washington, with the deepest coverage in Seattle, Tacoma, Spokane, Bellevue, and Everett. Search by ZIP code or city below to find the closest one, or filter by product type if you are after a specific format.

Market Insights Snapshot

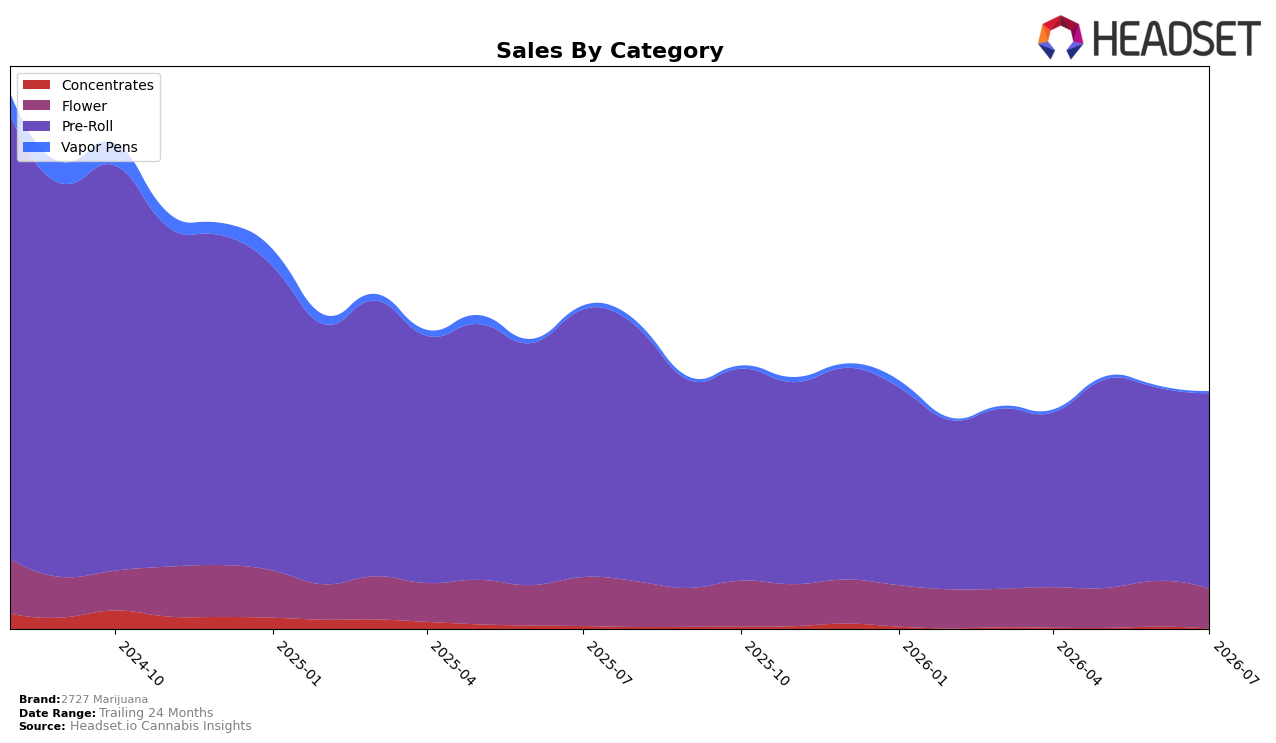

In July 2026, 2727 Marijuana concentrated 80.22% of sales in Pre-Roll, where category revenue declined 26.66% year over year but ticked up 1.25% month over month; Flower held 16.95% share with an 18.35% YoY drop and a 12.84% MoM decline. Vapor Pens accounted for 1.78% share with a 29.14% YoY fall and a 1.87% MoM rise, while Concentrates at 1.06% share contracted 48.73% YoY and 41.80% MoM. Against a brand-level sales decline of 25.76% YoY and a 2.71% YoY lift in average price, the dependency on Pre-Rolls anchors overall volatility, and the 10th-place rank in Washington Pre-Roll suggests stabilization is tied to incremental gains within that single category rather than broad portfolio momentum.

The mix shift implies a positioning that is narrowly price-accessible in Pre-Rolls (average price $9.50 alongside a 1.25% MoM lift) while premium-weighted Flower (average price $35.76) sheds volume at a faster MoM rate of 12.84%, indicating trading down within the brand’s own shelf. With Vapor Pens improving 1.87% MoM yet sitting at only 1.78% share and Concentrates retreating 41.80% MoM to 1.06% share, the portfolio lacks secondary pillars to offset Pre-Roll exposure; combined with a 10th-place Pre-Roll rank in Washington, the pattern points to a defensive posture where sustaining rank depends on reinforcing value tiers in Pre-Roll while selectively rebuilding Flower elasticity rather than leaning on smaller, more volatile formats.

Competitive Landscape

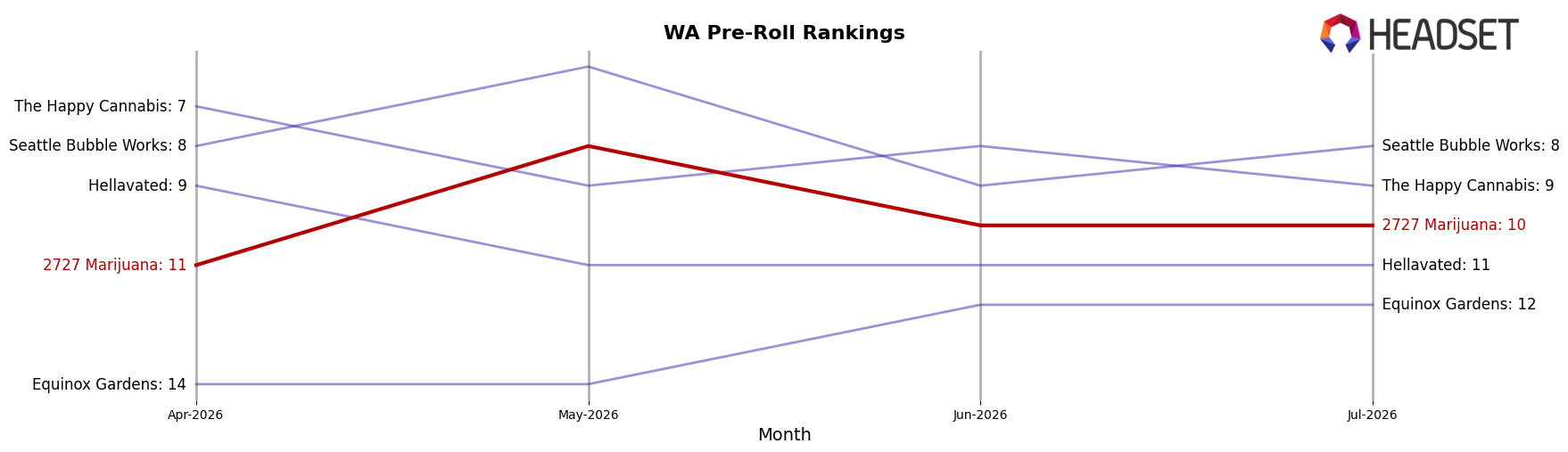

2727 Marijuana sits at rank #10 in Washington Pre-Roll in July 2026 after a year-over-year slide of 6 positions from #4, and it is 1 rank lower than April 2026’s #11 while still far from its #2 peak in July 2024; meanwhile, Ooowee advanced to #1 from #2 with a 59.5% YoY sales increase and Fire Bros. moved to #5 from #11 alongside a 52.0% YoY lift, indicating that competitor momentum at the top end coincides with 2727 Marijuana’s downward rank shift and implies share is consolidating toward faster-rising leaders.

Notable Products

Pineapple Biscotti Pre-Roll 5-Pack (5g) posted the steepest decline in July 2026 at -22.1% MoM while holding rank 4, indicating a pullback even as Acapulco Gold Pre-Roll 5-Pack (5g) led the lineup at rank 1. Blue Lobster Pre-Roll 5-Pack (5g) followed at rank 2 with no reported MoM figure, and Pearadise Infused Pre-Roll (1g) sat at rank 3 without a stated MoM change; nine of the top ten are Pre-Roll 5-Pack formats, concentrating the shelf around multi-pack smokeables. With Acapulco Gold anchoring the top slot and Pineapple Biscotti sliding, the mix points to a portfolio leaning into pack-led velocity while single infused SKUs play a narrower role, implying 2727 Marijuana is prioritizing repeatable multi-pack turns over flavor-led one-offs.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.