Where to Buy

The Pharm is stocked at 77 licensed dispensaries across Arizona, with the deepest coverage in Phoenix, Tucson, Mesa, Chandler, and El Mirage. Search by ZIP code or city below to find the closest one, or filter by product type if you are after a specific format.

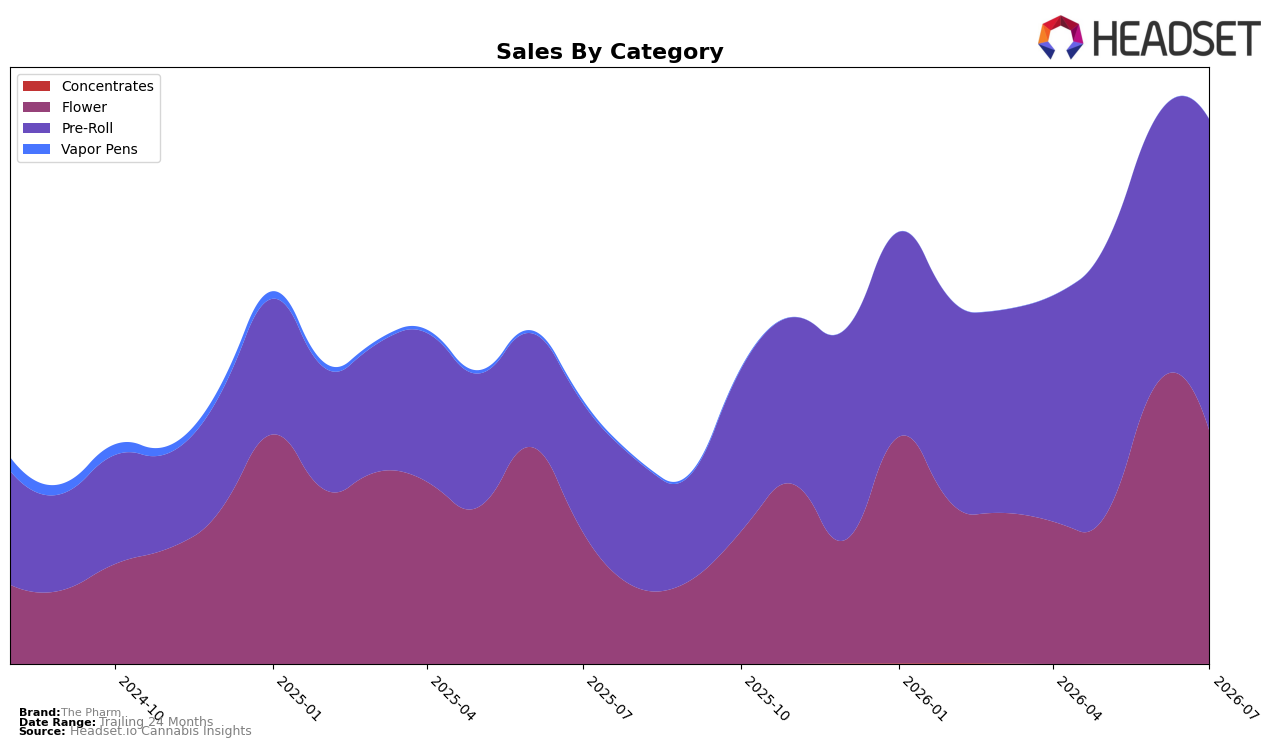

Market Insights Snapshot

In July 2026, The Pharm’s mix tilted further toward Pre-Roll, which held 57.24% share with 141.59% year-over-year growth and a 16.46% month-over-month gain, while Flower fell to 42.75% share with 77.43% year-over-year growth but a -17.41% month-over-month decline; Concentrates remained negligible at 0.01% share with a -20.70% month-over-month move. Coupled with a -23.50% year-over-year average price shift and overall brand sales up 106.87% year over year, the category split implies volume expansion led by Pre-Roll even as pricing compressed, and it positions Pre-Roll to dictate near-term trajectory more than Flower despite the latter’s larger historical base.

The tilt toward Pre-Roll aligns with The Pharm’s rank of 3 in Pre-Roll in Arizona, suggesting the brand can leverage a higher rank position to sustain share while Flower’s -17.41% month-over-month change risks ceding mix. With Pre-Roll up 16.46% month over month and Flower down -17.41% month over month in July 2026, the widening gap concentrates competitive exposure in a single category; the implication is that maintaining the rank-3 foothold while moderating price-driven erosion (avg price -23.50% year over year) is more likely to preserve total share than attempting to push marginal categories like Concentrates at 0.01% share.

Competitive Landscape

The Pharm sits at rank #3 in AZ Pre-Roll in July 2026, unchanged from #3 in July 2025, with a flat rank trajectory over both the year and the last three months at #3; meanwhile, Jeeter holds #1 with a 43.4% YoY sales increase and STIIIZY remains #2 with a 4.1% YoY lift, while Anthem jumped from #41 to #4 alongside a 1082.9% YoY sales surge. This stability at #3 coincides with peers either consolidating at the top or rapidly ascending from lower ranks, implying The Pharm’s current position is defended but increasingly exposed to an upward push from fast-rising challengers.

Notable Products

Dusties - Sapphire Diamond Infused Pre-Roll (1.3g) posted the standout movement in July 2026 with a +37.5% month-over-month gain and sits at rank 5, indicating momentum concentrated in infused singles rather than only multipacks. Dusties - Sapphire Infused Pre-Roll 6-Pack (3.6g) held rank 1 with +23.8% MoM while Dusties - Ruby Infused Pre-Roll 6-Pack (3.6g) at rank 3 rose +16.1%, and seven of the top ten SKUs are Pre-Roll items, pointing to a portfolio skew toward infused Pre-Rolls over Flower. The top Flower SKU, Mothers Milk (4g), slipped -0.5% MoM at rank 7 while Dusties - Emerald Diamond Infused Pre-Roll (1.3g) at rank 9 edged up +3.1%, a directional split that tilts demand toward infused formats even as non-infused Flower lags. This pattern implies The Pharm is consolidating share around Dusties infused Pre-Rolls, prioritizing potency-led formats and multi-pack value over traditional Flower for near-term commercial focus.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.