Jul-2026

Sales

Trend

6-Month

Product Count

SKUs

Avg Price

YoY Sales Change

YoY Price Change

Market Insights Snapshot

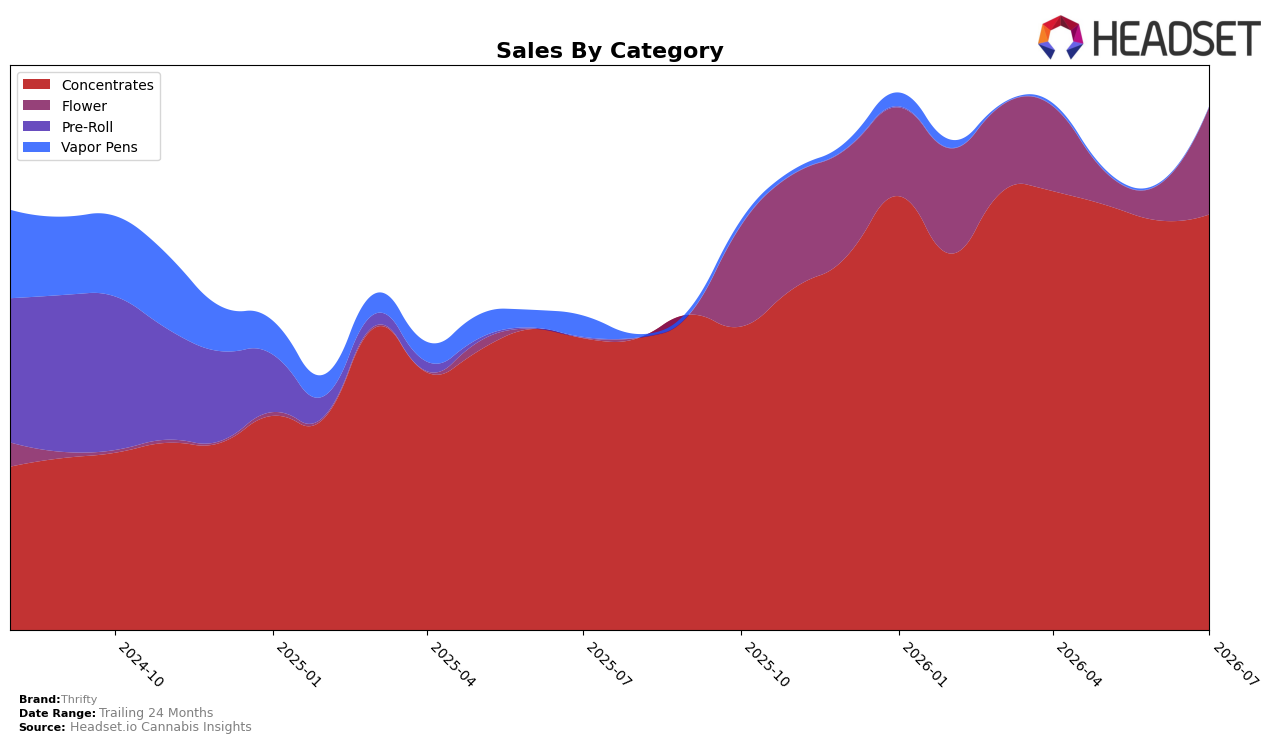

In July 2026, Concentrates held 79.44% share with 42.45% year-over-year growth and a 1.46% month-over-month uptick, while Flower rose to 20.56% share on a 210.49% month-over-month surge despite missing year-over-year data; the brand’s overall sales advanced 67.07% year over year as average price increased 16.49%. With Concentrates average price at $24.65 versus Flower at $66.72, the mix shift toward a high-volume, lower-priced core alongside a rapidly scaling premium-priced Flower tail signals a barbell structure that can widen reach while keeping price-accessible entry points.

Thrifty’s rank of 6 in Concentrates in Ontario alongside Concentrates’ 79.44% share and 1.46% month-over-month growth, paired with Flower’s 20.56% share on a 210.49% month-over-month rise, implies headroom to climb the Concentrates rankings by defending the core while using Flower’s higher ticket to lift blended revenue. The 67.07% year-over-year sales increase against a 16.49% average price lift points to volume-led expansion; sustaining July 2026 momentum likely depends on converting the Flower spike into repeat share while preventing cannibalization that would erode the 42.45% year-over-year gain in Concentrates.

Competitive Landscape

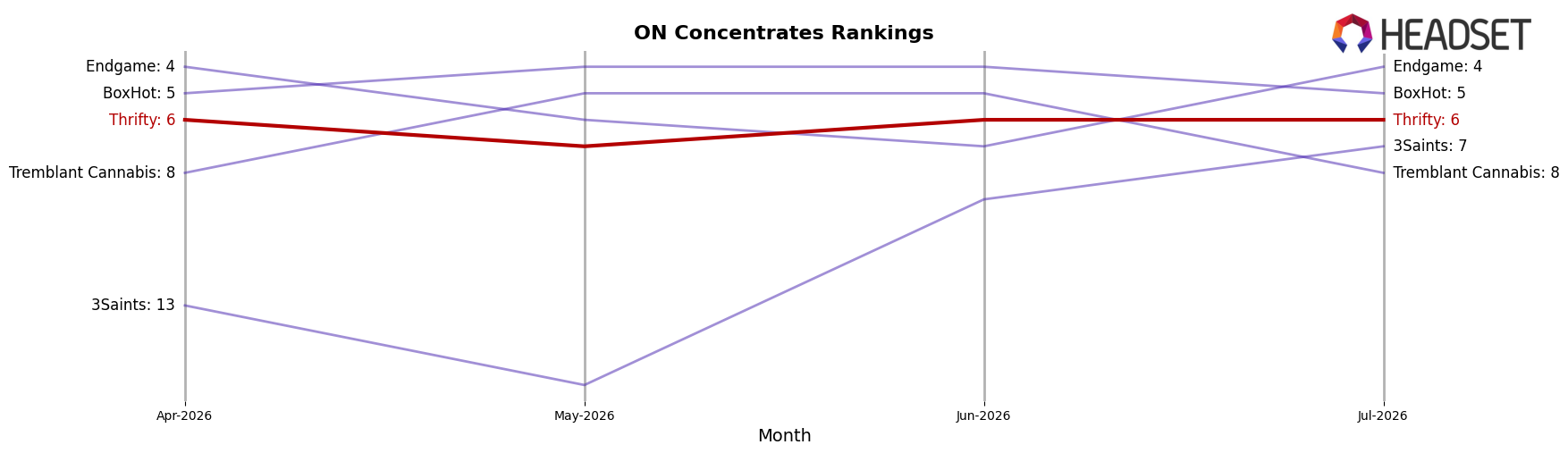

Thrifty is currently ranked #6 in ON Concentrates, a 3-place improvement from #9 year over year, and it held #6 for the last three months while peaking at #5 in March 2026. In contrast, BoxHot advanced from #8 to #5 alongside a 43.3% year-over-year sales lift, while Endgame slid from #2 to #4 with a -42.0% sales change; meanwhile, Pura Vida climbed from #4 to #2 with a 43.9% increase. This mix—Thrifty’s +3 rank gain YoY but flat position quarter-to-date and a competitor leap of three ranks into #5—implies Thrifty’s upward trajectory is moderating and requires either share capture or mix expansion to defend a top-5 target.

Notable Products

Bonkers (28g) posted the largest month-over-month surge at +476% to rank 5, while Big Steal Infused Hash (1.75g) fell -83% to rank 8, a split that points to demand consolidating in value Flower while marginal Concentrates contract. Big Steal Live Rosin (1g) climbed +594% to rank 3 and Big Steal Live Resin Dispenser (1g) jumped +255% to rank 2, but Big Steal Live Resin (1g) at rank 1 rose a more moderate +135%, implying the growth is skewing toward niche formats rather than the flagship. Three Flower SKUs now sit in ranks 4–7 with Mango Sapphire (28g) up +127% at rank 4 and BC Organic Sun Grown Bonkers (28g) up +269% at rank 6, concentrating momentum in large-pack Flower even as one Concentrates SKU collapses. The mix shift toward high-growth Flower and specialty Concentrates suggests Thrifty is pivoting volume into bigger baskets and novelty formats while pruning underperforming extract lines.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.