May-2026

Sales

Trend

6-Month

Product Count

SKUs

Avg Price

YoY Sales Change

YoY Price Change

Market Insights Snapshot

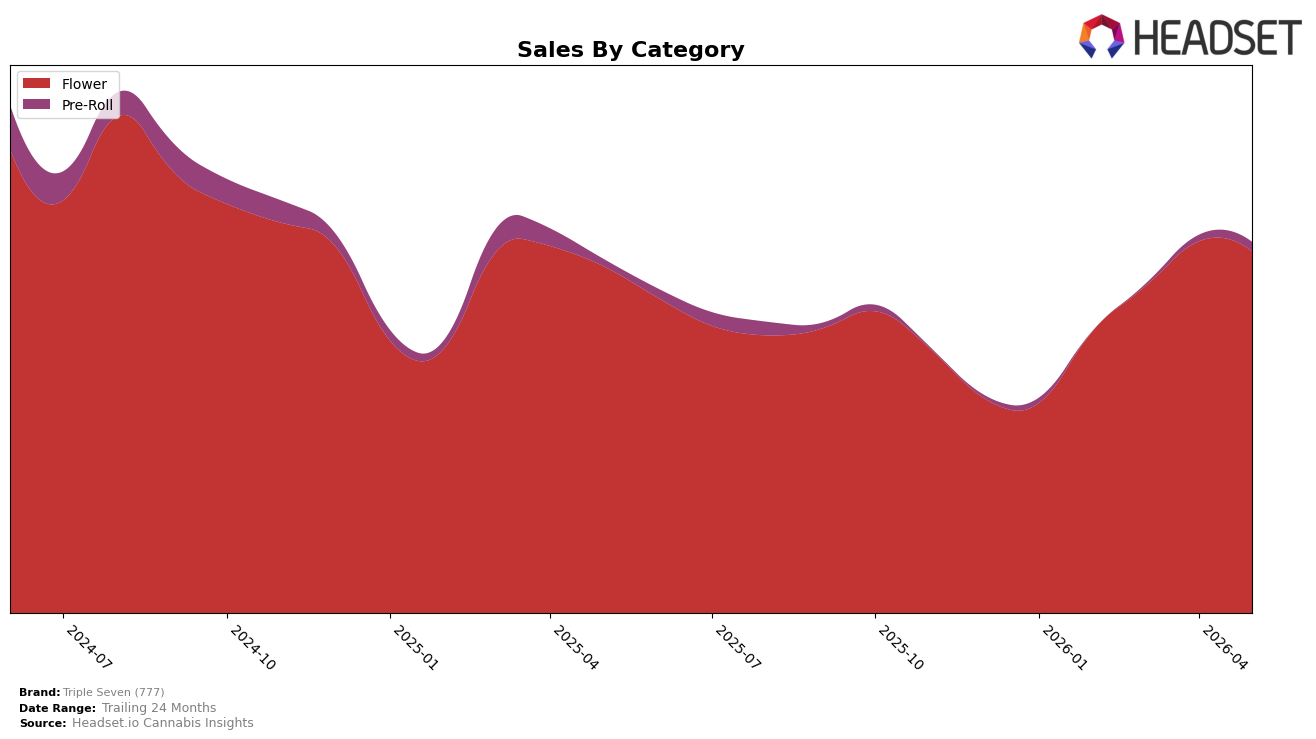

In May 2026, Triple Seven (777) concentrated 94.60% of sales in Flower with a 4.16% year-over-year increase but a 2.58% month-over-month decline, while Pre-Roll held 5.40% share with 11.20% year-over-year growth and a 15.95% month-over-month rise. The average price fell 10.86% year over year to $27.32 as overall brand sales grew 4.52% year over year, implying mix-driven volume gains despite a 24-month sales contraction of 29.57%. The pattern indicates a Flower-led base that is softening month over month while Pre-Roll is accelerating, suggesting near-term momentum is coming from smaller-format units rather than the core.

Holding rank 3 in Flower in Colorado alongside a 2.58% month-over-month Flower dip and a 15.95% month-over-month Pre-Roll lift points to share defense in the core category while leveraging trading down or trial via lower-priced Pre-Rolls. With Flower’s 94.60% share and only 5.40% in Pre-Roll, the widening growth gap between a 4.16% year-over-year Flower uptick and an 11.20% year-over-year Pre-Roll rise implies the brand’s positioning is anchored in premium Flower but increasingly reliant on value-access SKUs to sustain traffic and mitigate price compression.

Competitive Landscape

Triple Seven (777) sits at rank #3 in CO Flower in May 2026, unchanged from #3 year over year, and also flat versus three months ago at #3, while its historical peak was #2 in November 2024; in contrast, Seed & Strain Cannabis Co. holds #1 now and also held #1 a year ago with a 62.8% YoY sales lift, and Good Chemistry Nurseries is stable at #2 with a 40.2% YoY increase, indicating that top-tier momentum is accruing above Triple Seven (777) while Green Dot Labs remains at #4 despite a 45.6% YoY gain and LIT (CO) stays at #5 with a 3.2% YoY rise; the pattern implies that Triple Seven (777)’s steady #3 rank reflects competitive entrenchment—growth from leaders is widening the gap above while mid-pack advances are insufficient below, so reclaiming #2 will likely require outperforming the 40%–63% YoY pace set by the brands ahead.

Notable Products

Longbottom Boogie (14g) posted the largest month-over-month move in May 2026 at +60.97%, climbing into rank 2 while Ky Jealous (3.5g) rose +14.21% to hold rank 1. Commando Pre-Roll (1g) slipped -4.70% at rank 3 and Black Triangle (14g) fell -7.19% at rank 4, yet eight of the top ten are Flower SKUs, concentrating mix away from Pre-Roll. The addition of multiple new 14g entries at ranks 5–9 with no prior-month comps, alongside one standout 14g surge above +50% and a Pre-Roll decline under -5%, implies Triple Seven (777) is tilting toward larger-pack Flower volume even as smaller formats soften.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.