Jul-2026

Sales

Trend

6-Month

Product Count

SKUs

Avg Price

YoY Sales Change

YoY Price Change

Where to Buy

Good Chemistry Nurseries is stocked at 136 licensed dispensaries across Massachusetts and Colorado, 114 of them in Massachusetts, with the deepest coverage in Brockton, Worcester, Northampton, Boston, and Fall River. Search by ZIP code or city below to find the closest one, or filter by product type if you are after a specific format.

Market Insights Snapshot

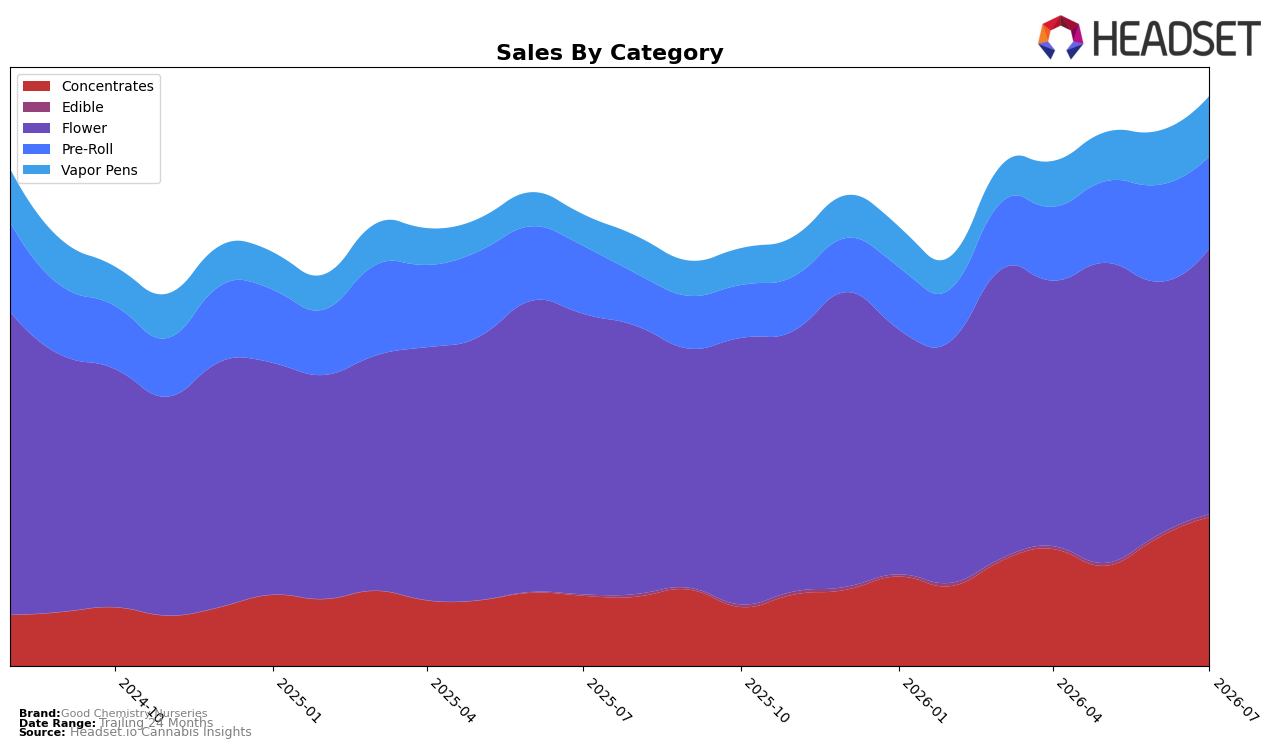

Good Chemistry Nurseries shifted its category mix in July 2026 with Flower still at 46.69% share but down year over year by 5.21% even as month over month rose 4.99%, while Concentrates climbed to 26.12% share with 111.88% YoY growth and 16.16% MoM, indicating a pivot toward higher-intensity formats. Pre-Roll held 16.11% share with 35.45% YoY growth but slipped 4.98% MoM, and Vapor Pens reached 10.59% share with 92.86% YoY and 12.17% MoM gains; Edible remained marginal at 0.48% share despite 136.38% YoY and 3.36% MoM increases. With brand-level sales up 26.30% YoY and average price up 8.61%, the pattern implies that mix-led growth is being driven by rapid expansion in Concentrates and Vapor Pens offsetting Flower’s YoY softness, while Flower’s MoM uptick stabilizes the base.

These shifts reposition Good Chemistry Nurseries toward a two-engine portfolio where Concentrates and Vapor Pens provide velocity (up 111.88% and 92.86% YoY respectively) and Flower anchors scale (46.69% share with a 4.99% MoM rise), suggesting defensible breadth across inhalable formats. The combination of a 16.16% MoM surge in Concentrates and a 4.98% MoM dip in Pre-Roll implies share recycling within inhalables toward potency and convenience, which supports price resilience given the 8.61% average price increase. In Colorado Flower, a category rank of 3 paired with a 5.21% YoY decline but positive MoM indicates that maintaining top-three visibility can coexist with shifting internal emphasis toward faster-growing subcategories, implying that the brand can leverage Flower rank to cross-pull consumers into adjacent formats.

Competitive Landscape

Good Chemistry Nurseries sits at rank #3 in Colorado Flower in July 2026, down 2 positions year over year from #1, with rank stability versus April 2026 at #3 suggesting the drop is not a one-month anomaly; meanwhile, Seed & Strain Cannabis Co. moved up to #1 from #2 with 76.2% YoY sales growth, and Triple Seven (777) advanced to #2 from #3 with 56.8% YoY growth, while Green Dot Labs holds #4 with 21.8% YoY growth and Natty Rems surged to #5 from #23 on 168.5% YoY growth; the pattern implies Good Chemistry Nurseries must counter faster-climbing rivals to avoid further share erosion implied by a two-rank YoY slide from a peak at #1 in December 2025.

Notable Products

With no month-over-month percentages reported for July 2026, the headline shifts to rank dynamics: Peach Maraschino (3.5g) sits at rank 1 while Lift Ticket (3.5g) holds rank 8, a spread that signals concentration at the top despite two Flower SKUs in the top two positions. Blueberry Muffin (3.5g) at rank 2 and GMO Zkittlez (3.5g) at rank 4 reinforce that Flower accounts for six of the top ten, whereas Pre-Roll placements at ranks 3, 6, 9, and 10 indicate a secondary role even with a top-three foothold. Peach Maraschino (3.5g) also leads on absolute sales at $133,785 while the highest-ranked Pre-Roll, Lift Ticket Pre-Roll (1g), lands at rank 3, pointing to a portfolio where flagship Flower drives visibility and Pre-Roll depth fills out volume tiers. The pattern implies Good Chemistry Nurseries is leaning into premium Flower leadership while using multiple Pre-Roll entries to broaden basket reach rather than to displace the Flower core.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.