Jul-2026

Sales

Trend

6-Month

Product Count

SKUs

Avg Price

YoY Sales Change

YoY Price Change

Where to Buy

Valhalla is stocked at 202 licensed dispensaries across New Jersey, Maryland, and 5 other states, 79 of them in New Jersey, with the deepest coverage in Egg Harbor Township, Franklin Township, Camden, Atlantic City, and Elizabeth. Search by ZIP code or city below to find the closest one, or filter by product type if you are after a specific format.

Market Insights Snapshot

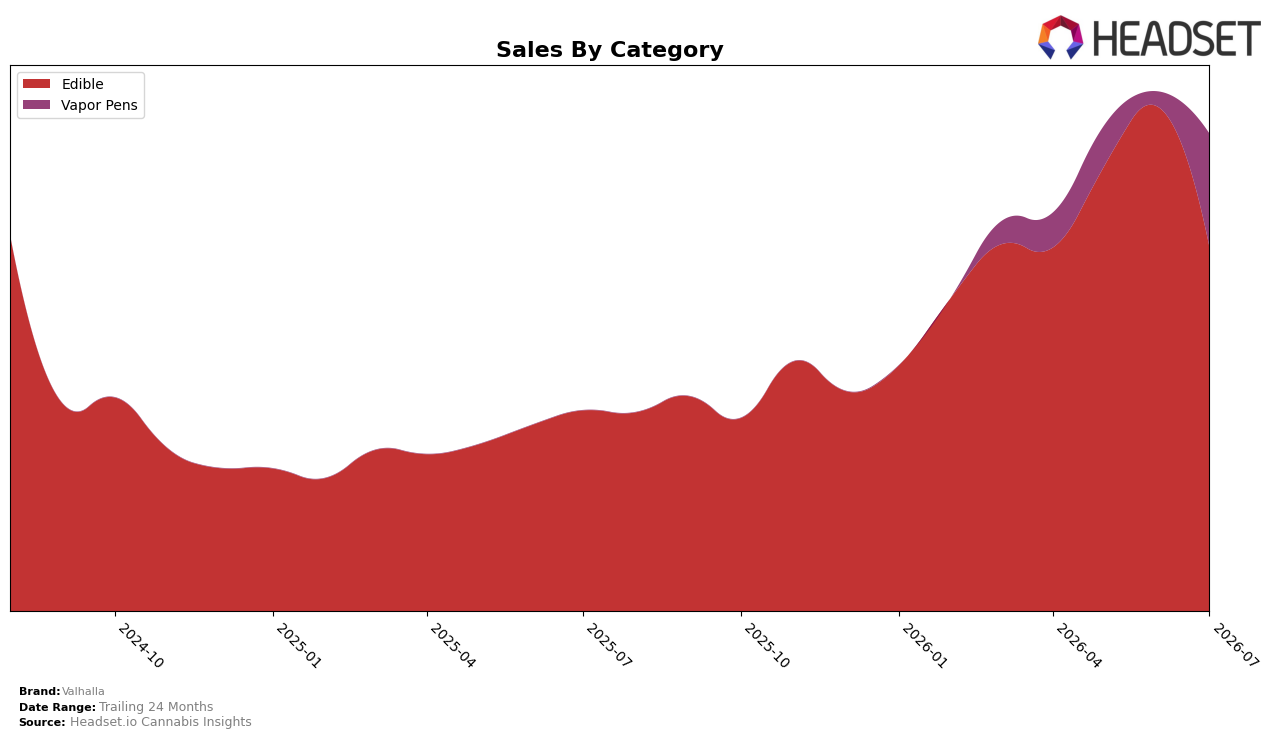

In July 2026, Valhalla’s mix concentrated 76.30% of sales in Edible, down month over month by 27.81% but up year over year by 81.46%, while Vapor Pens expanded to 23.70% share with a 651.31% month-over-month surge and no year-over-year baseline yet. Despite the average price rising 0.88% year over year to $14.78, Edible pricing within the mix sat lower at $13.00 versus $26.37 in Vapor Pens, indicating a material trade-up in basket composition even as the core Edible unit velocity cooled. With an Edible rank of 12 in New Jersey and a brand-level sales increase of 137.84% year over year, the mix shift implies that near-term growth is being pulled by re-entry or expansion in Vapor Pens rather than incremental depth in the Edible core.

The category pivot suggests a positioning broadening: the 651.31% month-over-month jump in Vapor Pens alongside a 27.81% decline in Edible points to resource allocation and retail attention moving toward higher-price devices, helping lift average realized price 0.88% even as Edible dominates 76.30% of volume. Holding a rank of 12 in New Jersey Edible while Vapor Pens climb to 23.70% share in July 2026 indicates Valhalla can leverage Edible awareness to seed faster-velocity pen formats; the implication is a dual-track strategy where Edible sustains baseline distribution and Vapor Pens drives ticket-size growth, positioning the brand to trade consumers up without abandoning its Edible anchor.

Competitive Landscape

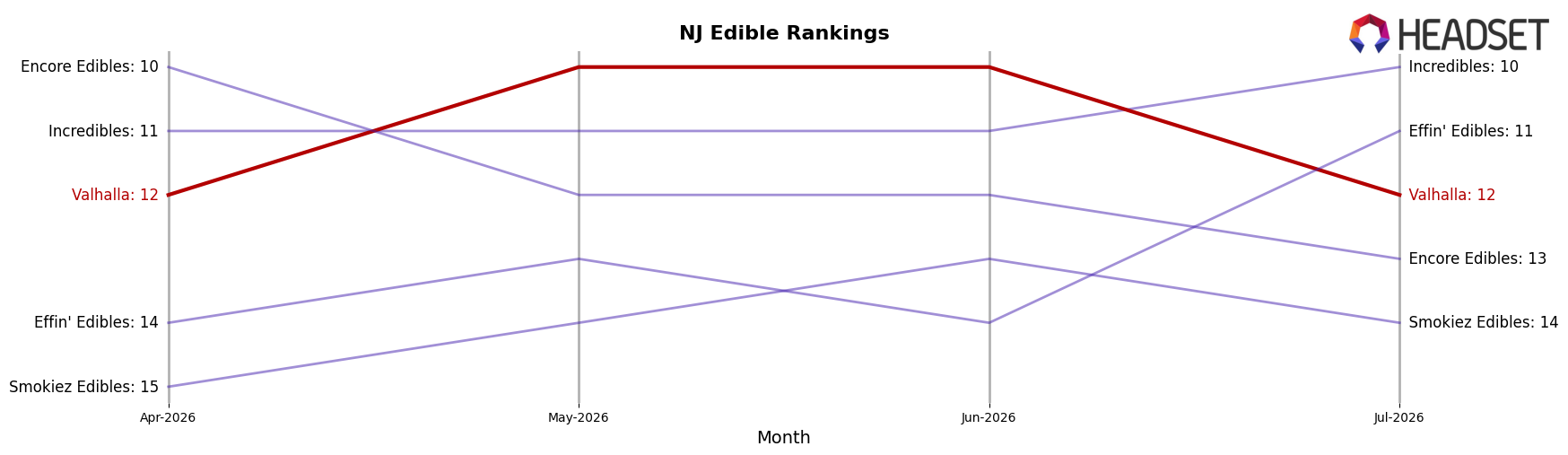

Valhalla ranks #12 in New Jersey Edible for July 2026, improving 4 positions year over year from #16 while holding flat versus April 2026 at #12; the brand also slipped 2 spots from its peak #10 in June 2026, indicating short-term volatility within an upward annual trend. Against peers, Gron / Grön held #1 year over year but did so alongside a 14.9% YoY sales decline, while Wyld climbed from #3 to #2 with 2.8% YoY growth, suggesting Valhalla’s path from #16 to #12 aligns more with share reallocation than broad category expansion. The mix of a 4-rank annual gain, a 2-rank pullback from June 2026’s peak, and competitors shifting in opposite directions implies Valhalla’s rank trajectory is driven by incremental share capture that requires sustained execution to convert transient monthly peaks into a stable top‑10 position.

Notable Products

Strawberry Lemonade Soft Lozenges 10-Pack (100mg) posted the steepest move in July 2026 with a -80.99% month-over-month drop and slid to rank 7, while Indica Blue Raspberry Soft Lozenges 10-Pack (100mg) fell -20.64% yet held rank 1, indicating demand concentrated at the top even as velocity eroded. Green Apple Soft Lozenges 10-Pack (100mg) declined -12.70% at rank 2, and five Soft Lozenges SKUs sit in the top 10, signaling a portfolio still led by the lozenge format despite broad pullbacks. Sativa Pineapple RSO Gummies 10-Pack (100mg) decreased -10.15% at rank 5 as Indica Grape RSO Gummies 10-Pack (100mg) slipped -7.16% at rank 3, and total top-10 mix skews toward Edible staples with only one new entrant lacking a prior-month comp. The pattern implies Valhalla is over-indexed to a few flagship lozenges that maintain rank but face volume compression, pointing to a need for mix diversification rather than deeper price moves around the roughly $53,088 leader.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.