Jul-2026

Sales

Trend

6-Month

Product Count

SKUs

Avg Price

YoY Sales Change

YoY Price Change

Where to Buy

Kynd Cannabis Company is stocked at 265 licensed dispensaries across Pennsylvania, Florida, and 4 other states, 72 of them in Pennsylvania, with the deepest coverage in Philadelphia, Pittsburgh, Lancaster, Altoona, and Cranberry Twp. Search by ZIP code or city below to find the closest one, or filter by product type if you are after a specific format.

Market Insights Snapshot

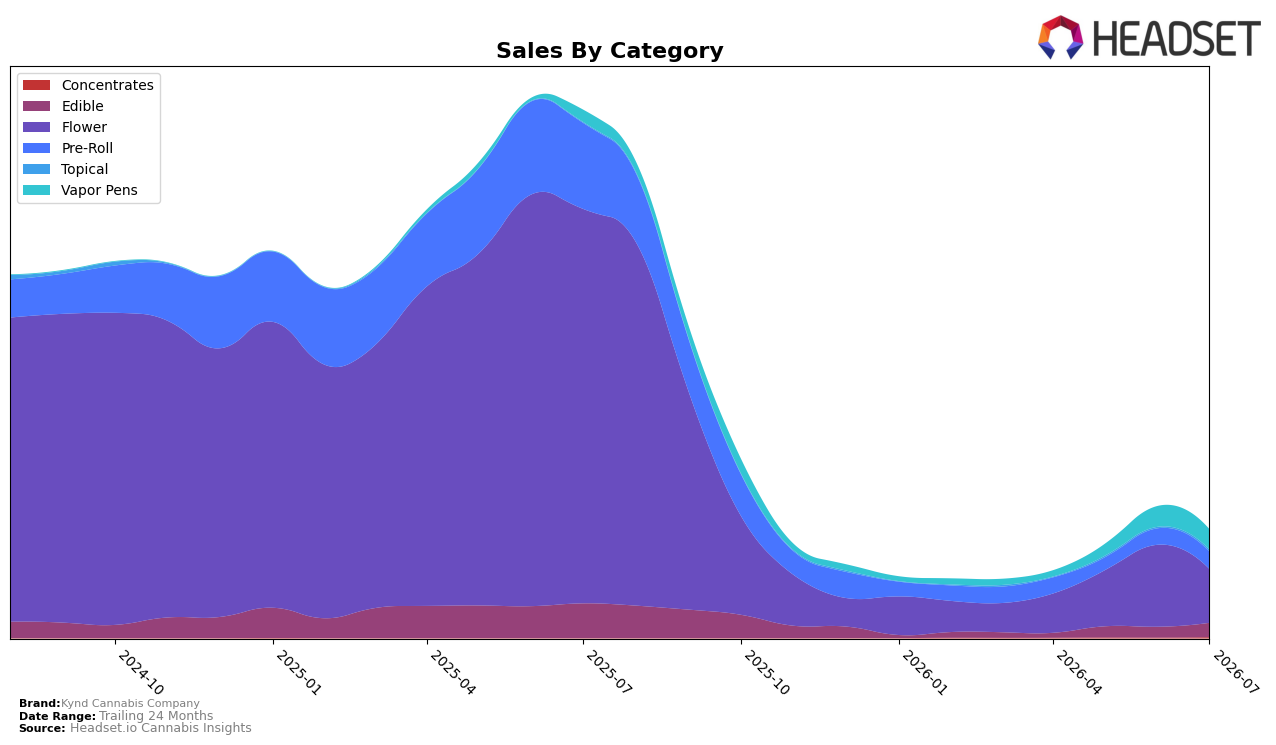

Kynd Cannabis Company’s July 2026 category mix tilts toward Flower at 49.89% share, but Flower volume deteriorated with a -86.46% year-over-year drop and a -34.58% month-over-month decline, while the brand’s average price fell -3.87% YoY. Vapor Pens expanded year-over-year by 67.21% yet slipped -2.45% month-over-month to 18.71% share, and Pre-Roll contracted -80.08% YoY but grew 5.85% MoM to 15.94% share. Edible rose 33.98% MoM despite a -59.13% YoY decline to 13.12% share, and smaller niches moved sharply with Topical up 214.64% YoY and 55.17% MoM, and Concentrates up 78.91% MoM. With Flower ranked 39th in Ohio and brand sales down -79.68% YoY, the pattern implies the legacy Flower anchor is shrinking faster than emerging segments can offset, pointing to a mix-led transition that has not yet stabilized.

The shift toward faster-growing pockets like Vapor Pens (+67.21% YoY) and Topical (+214.64% YoY) alongside month-over-month lifts in Edible (+33.98%) and Concentrates (+78.91%) indicates Kynd Cannabis Company is leaning into higher-velocity, lower-ticket formats as Flower (-86.46% YoY; -34.58% MoM) and overall average price (-3.87% YoY) compress. Holding 18.71% share in Vapor Pens with only a -2.45% MoM dip and gaining 5.85% MoM in Pre-Roll at 15.94% share suggests a tactical pivot away from large-basket Flower toward accessible price points, but the 39 rank in Ohio Flower and a -65.43% decline over 24 months imply the brand’s positioning hinges on accelerating non-Flower penetration faster than Flower erodes.

Competitive Landscape

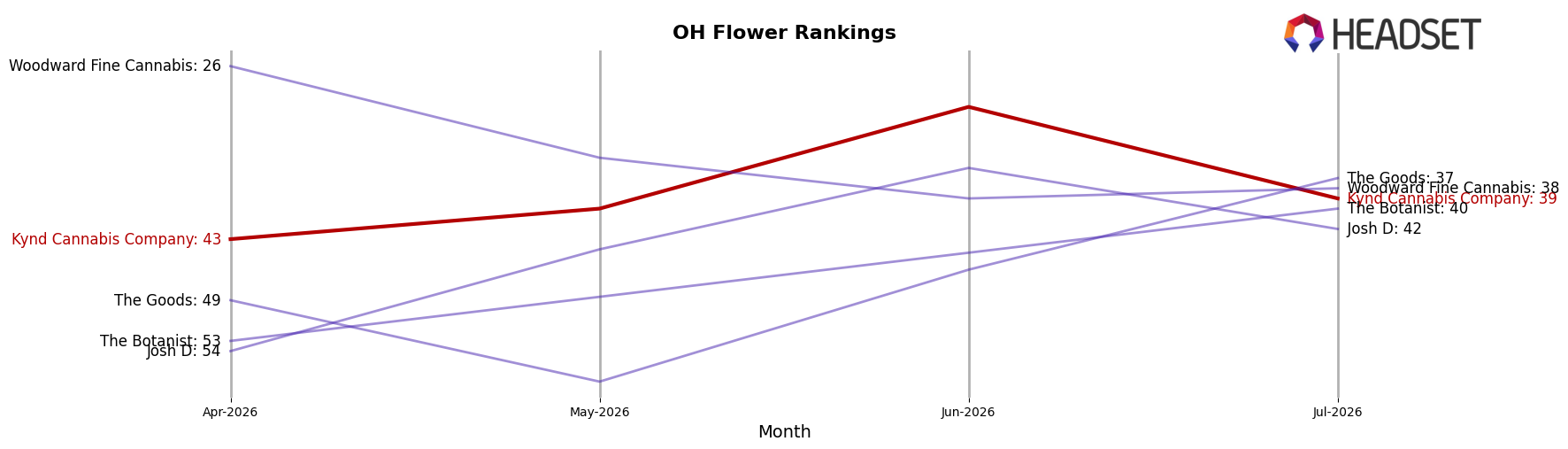

Kynd Cannabis Company ranks #39 in OH Flower in July 2026, slipping 8 positions year over year from #31 while improving 4 spots versus April 2026’s #43, and it remains well below its peak of #22 from April 2025. In contrast, RYTHM climbed from #6 to #1 with 74.99% YoY sales growth, and Klutch Cannabis surged from #21 to #3 on 403.04% YoY sales growth, whereas Riviera Creek edged down from #1 to #2 alongside a 15.97% YoY sales decline. The mix of a year-over-year rank drop of 8 places and a recent three-month gain of 4 places implies Kynd Cannabis Company is stabilizing month to month but losing relative position against faster-rising leaders.

Notable Products

Lollipopz (3.5g) posted the steepest move with a -31.3% month-over-month drop while holding rank 10, signaling a pullback at the value end even as Caesar (2.83g) surged +87.2% to rank 1. Belly Laugh (14.15g) climbed +55.1% while sitting at rank 6, and Bolo Runtz Pre-Roll (1g) advanced +50.4% at rank 2, creating a split where gains concentrate at the top ranks while a lower-ranked Flower SKU retreats. With Flower occupying six of the top ten positions alongside three Pre-Roll entries, the assortment skews toward inhalables, implying Kynd Cannabis Company is consolidating share around higher-velocity Flower leaders while pruning or repositioning lagging Flower formats; the current mix concentrates volume in a few fast-rising SKUs rather than broad uniform growth.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.