Jul-2026

Sales

Trend

6-Month

Product Count

SKUs

Avg Price

YoY Sales Change

YoY Price Change

Market Insights Snapshot

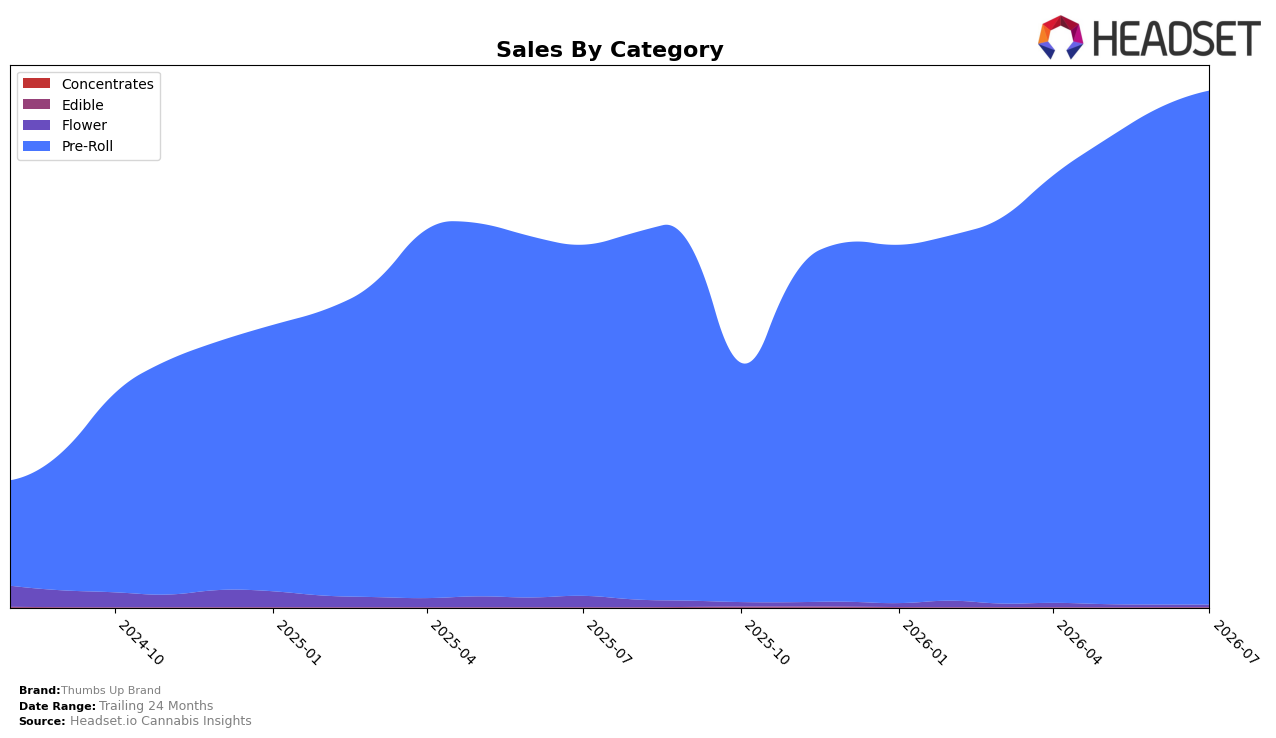

Thumbs Up Brand concentrated 99.57% of July 2026 sales in Pre-Roll, up 3.62% month over month and 46.45% year over year, while the smaller Flower line fell 0.60% MoM and 80.65% YoY to a 0.41% share. Edible contracted sharply with a 69.90% MoM decline and 34.69% YoY drop to a 0.00% share, whereas Concentrates inched up 5.58% MoM to a 0.02% share with no year-ago baseline, indicating a near-single-category identity that is tightening further as Pre-Roll expands and secondary bets retrench.

The July 2026 rank of 4 in Ontario Pre-Roll and a 7.87% YoY decrease in average price alongside a 46.45% YoY Pre-Roll growth rate suggest price elasticity is fueling volume gains, while a 3.62% MoM lift paired with a 0.60% MoM decline in Flower points to deliberate share consolidation into the leading format. With total brand sales up 42.64% YoY and Pre-Roll holding 99.57% mix, the positioning leans into scale and price-driven throughput rather than portfolio breadth, implying that sustaining rank will depend on maintaining price-value while selectively rebuilding complementary categories to hedge against single-format volatility.

Competitive Landscape

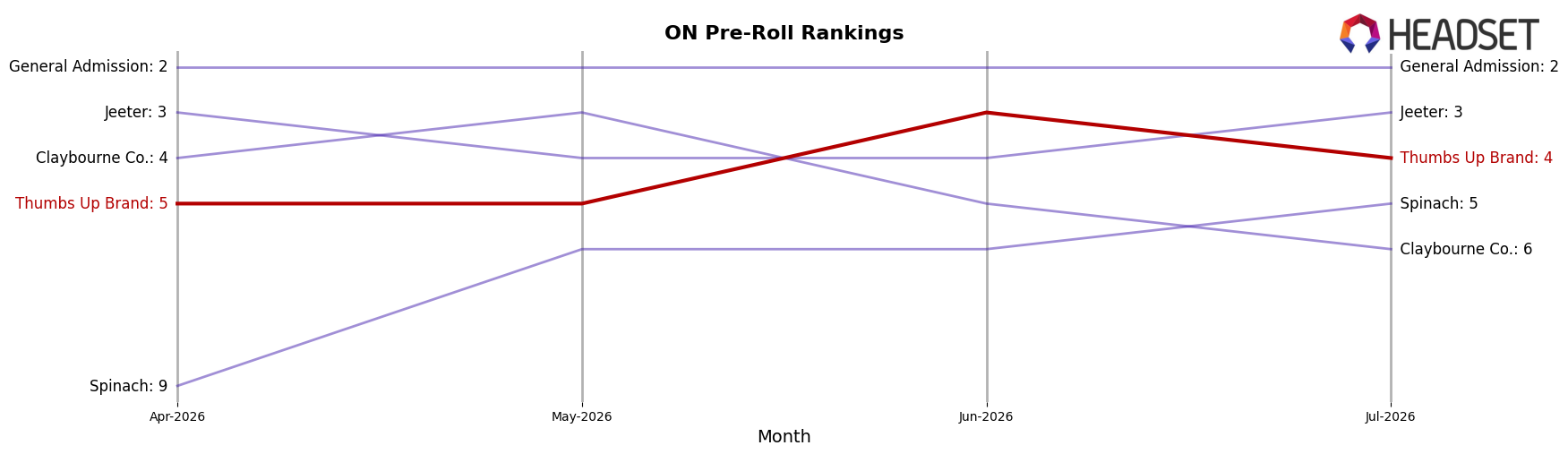

Thumbs Up Brand is currently ranked #4 in ON Pre-Roll, improving 5 positions year over year from #9 to #4 and gaining 1 spot since April 2026’s #5, while its peak rank of #3 in June 2026 indicates brief outperformance; meanwhile, Back Forty / Back 40 Cannabis moved from #2 to #1 with a 67.4% YoY sales increase and General Admission slid from #1 to #2 with a 23.2% YoY sales decline, and Jeeter held #3 despite a 37.9% YoY drop, while Spinach advanced from #14 to #5 on 65.3% YoY growth; this configuration implies Thumbs Up Brand’s rank trajectory toward the top tier is driven more by competitor volatility than runaway category share capture, and sustaining a top-3 position will require converting June 2026’s #3 spike into durable gains against a faster-rising #1 and #5.

Notable Products

Hybrid Pre-Roll 2-Pack (2g) delivered the most pronounced movement in July 2026 with a 64.0% month-over-month gain while holding rank 3, contrasting with Indica x Sativa Pre-Roll 2-Pack (2g) falling 27.1% at rank 6 and Sativa Pre-Roll 10-Pack (5g) down 12.3% at rank 10. Indica Pre-Roll 2-Pack (2g) rose 105.4% and stayed at rank 1, while Sativa Pre-Roll 2-Pack (2g) jumped 189.5% at rank 2, and eight of the top ten are Pre-Roll 2-Packs or 4-Packs anchoring velocity over multi-pack 10-Pack formats. Variety Pack Pre-Roll 2-Pack (2g) slid 42.5% at rank 9 even as Indica Pre-Roll 10-Pack (5g) grew 25.6% at rank 8, indicating mixed traction for larger counts versus clear momentum in lighter-count formats concentrated in the top five. The pattern implies Thumbs Up Brand is consolidating share through fast-rotating 2-Pack SKUs while selectively pruning or repositioning 10-Packs that underperform despite isolated gains.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.