Jun-2026

Sales

Trend

6-Month

Product Count

SKUs

Avg Price

YoY Sales Change

YoY Price Change

Market Insights Snapshot

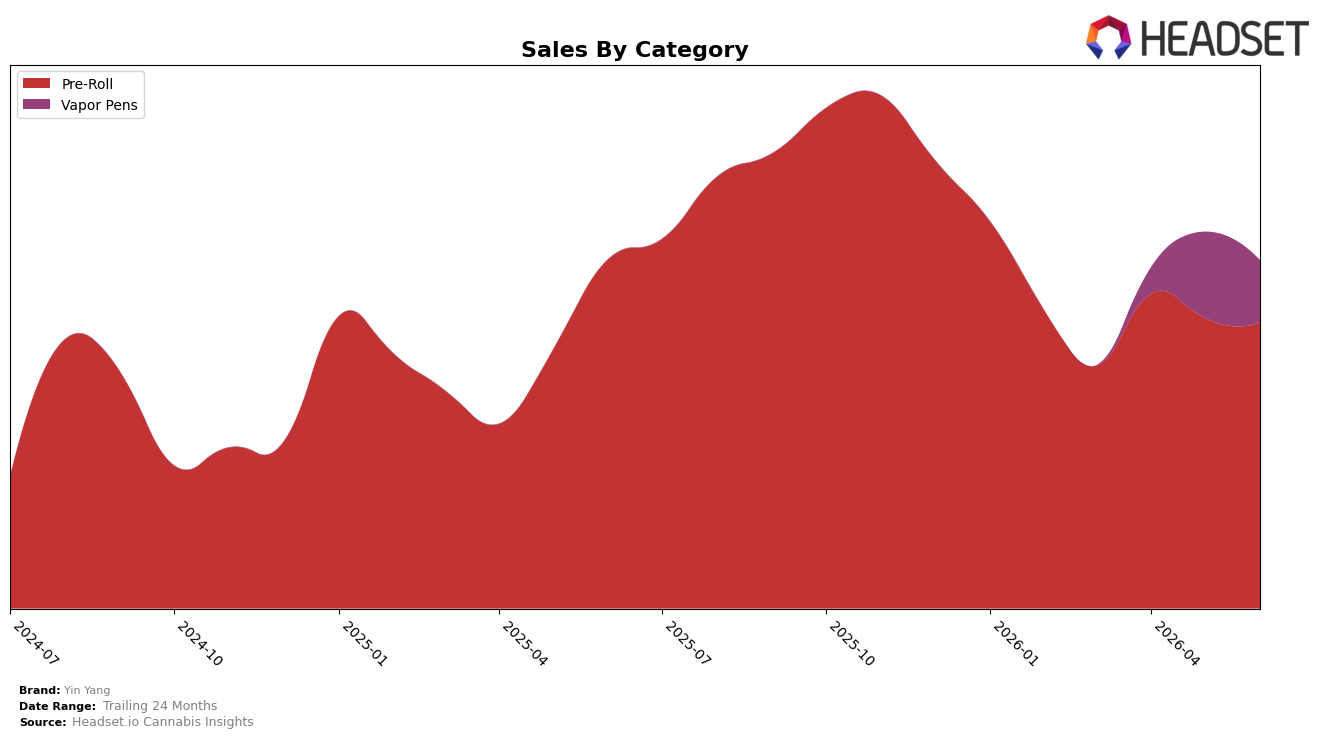

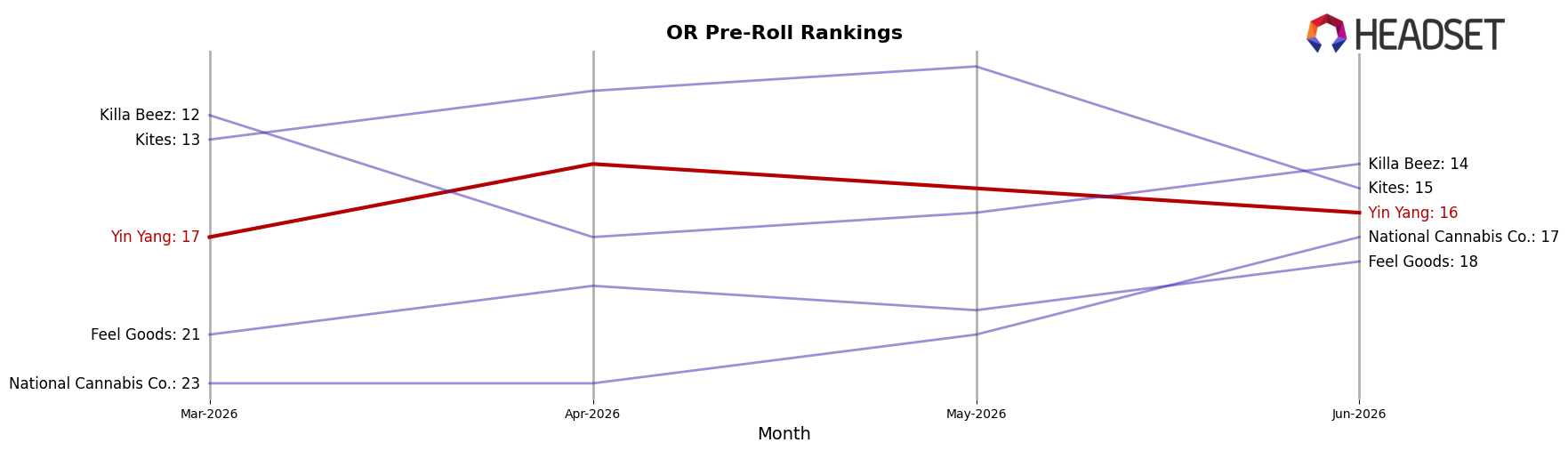

In June 2026, Yin Yang concentrated 82.08% of sales in Pre-Roll while Vapor Pens accounted for 17.92%, indicating a two-category footprint tilted toward value-priced Pre-Roll. Pre-Roll declined 18.22% year over year and 1.72% month over month, while Vapor Pens contracted 27.30% month over month with no year-over-year baseline, pointing to a pullback rather than seasonal expansion. The brand’s average price fell 37.81% year over year to $19.49, and overall brand sales decreased 36.32% year over year even as the 24‑month trajectory rose 149.42%, which suggests recent compression amid longer-horizon expansion. In Oregon Pre-Roll, the brand held rank 16, and with Pre-Roll’s 82.08% mix alongside a 1.72% month-over-month decline, the category dependency is exerting drag on near-term momentum.

These shifts imply that Yin Yang’s positioning leans into lower-priced Pre-Roll scale rather than margin-rich diversification, as evidenced by the 37.81% average price decline paired with an 18.22% Pre-Roll year-over-year contraction. With Vapor Pens down 27.30% month over month while holding only 17.92% mix, the portfolio lacks a counterweight to category-specific volatility, which contributes to the 36.32% brand sales year-over-year decline despite a 149.42% increase over 24 months. Holding rank 16 in Oregon Pre-Roll while Pre-Roll is down 1.72% month over month signals that defending share requires price-pack architecture or format innovation within Pre-Roll rather than incremental Vapor Pen reliance, because the current mix concentration (82.08% vs. 17.92%) amplifies downside when Pre-Roll softens.

Competitive Landscape

Yin Yang ranks #16 in Oregon Pre-Roll in June 2026, down 7 positions year over year from #9, and up 1 spot from #17 three months ago; by contrast, STiCKS climbed from #2 to #1 with 164.98% YoY sales growth while Hellavated slipped from #1 to #3 despite 15.90% YoY growth. Yin Yang’s peak was #8 in November 2025 before a 8-place slide to today, whereas Kaprikorn rose from #5 to #2 on 113.36% YoY growth and Portland Heights fell from #3 to #4 with a 26.34% YoY decline, indicating that Yin Yang’s downward rank trajectory amid both accelerating climbers and weakening incumbents signals share being ceded to faster-growing leaders rather than a category-wide contraction.

Notable Products

We're Not Worthy x Ballroom Blitz Pre-Roll 10-Pack (5g) posted the largest month-over-month gain at +163.5% and still sat only at rank 4, while Foxy Brown x Big Yang Theory Pre-Roll 2-Pack (1g) declined -15.2% and slipped to rank 8. Sometimes You're the Windshield x Sometimes You're the Bug Pre-Roll 10-Pack (5g) climbed +92.4% to rank 3, and the Guava Distillate Cartridge (1g) held rank 9 despite no reported Mom change, indicating limited vapor pen traction versus the surge in multi-pack pre-rolls. With eight of the top ten in Pre-Roll and two SKUs posting +90% or more while a 2-pack fell -15.2%, the mix points to Yin Yang consolidating demand around larger-count Pre-Roll formats over smaller packs and non-Pre-Roll options.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.