Jul-2026

Sales

Trend

6-Month

Product Count

SKUs

Avg Price

YoY Sales Change

YoY Price Change

Where to Buy

1988 is stocked at 127 licensed dispensaries across Washington and Illinois, 107 of them in Washington, with the deepest coverage in Seattle, Spokane, Bellingham, Tacoma, and Bellevue. Search by ZIP code or city below to find the closest one, or filter by product type if you are after a specific format.

Market Insights Snapshot

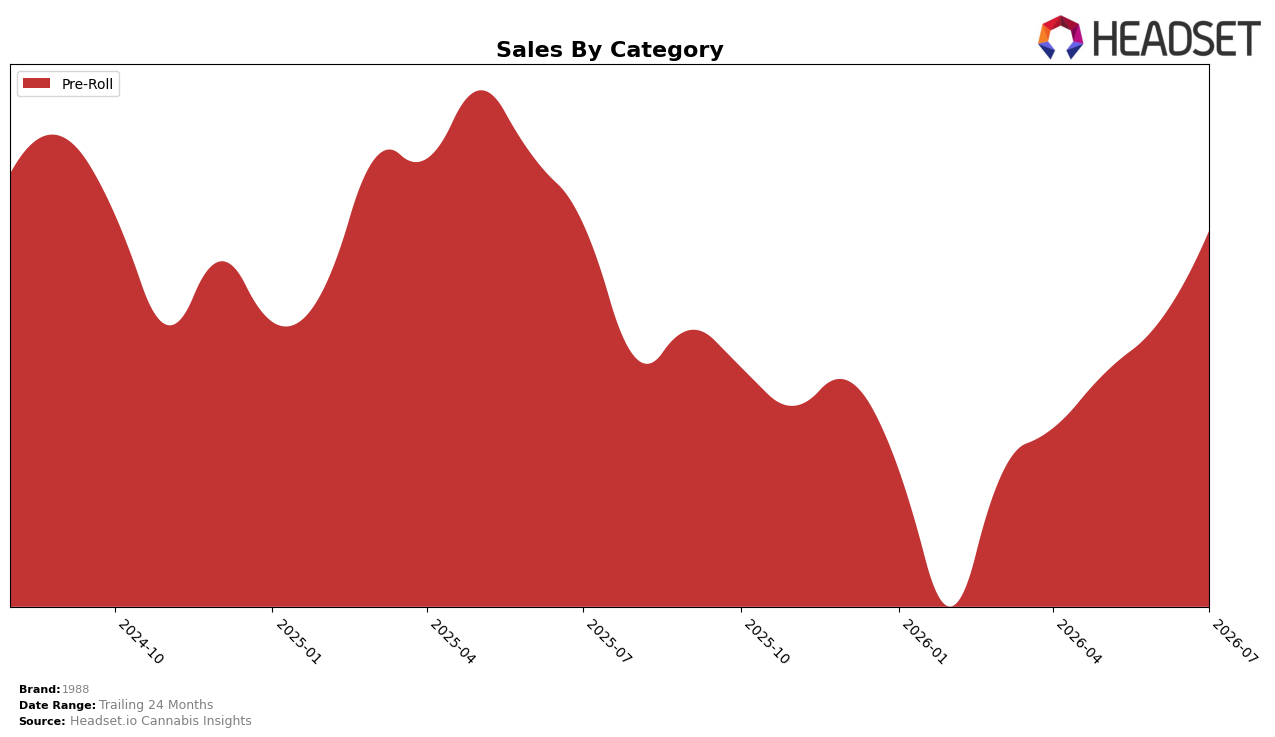

In July 2026, 1988’s mix concentrated 100.0% in Pre-Roll, with category share unchanged from earlier months while the Pre-Roll line itself moved +12.6% month over month and -88.7% year over year. Average price declined -7.1% year over year alongside a 100.0% category allocation, and the brand held rank 14 in Pre-Roll within Washington. The pattern implies a single-category dependence where short-term MoM lift coexists with a steep YoY contraction, signaling throughput recovery at current price points but exposure to annual volatility.

Given a sole reliance on Pre-Roll at 100.0% of sales and a rank position of 14 in Washington, the -88.7% year-over-year swing against a +12.6% month-over-month uptick suggests that 1988’s positioning is tied to episodic demand rather than diversified demand capture. With average price down -7.1% YoY and a 24‑month sales change of +78.5%, the mix points to a value-leaning stance that can gain near-term velocity without broadening reach, implying the brand’s path to sustained rank improvement likely depends on either reinforcing Pre-Roll penetration at lower price tiers or reintroducing category breadth to smooth YoY volatility.

Competitive Landscape

1988 is currently ranked #14 in WA Pre-Roll, improving 2 positions from #16 year over year and climbing 5 spots from #19 over the last three months, reaching its peak rank of #14 in July 2026. In contrast, Ooowee advanced from #2 to #1 while posting a 59.5% year-over-year sales increase, and Phat Panda slipped from #1 to #2 despite a 1.2% sales uptick, indicating that 1988’s upward rank shift is occurring alongside intensified movement at the top. With Lifted Cannabis Co jumping from #7 to #4 and Fire Bros. rising from #11 to #5 on 52.0% growth, the middle tier is compressing as faster climbers occupy share, implying that 1988’s incremental ascent from #16 to #14 requires acceleration to avoid being outpaced by brands posting 30–60% growth.

Notable Products

Honey Infused Blunt (1g) posted the largest momentum shift in July 2026 with +26.3% MoM at rank 2, while the category leader African Mango Infused Blunt (1g) grew +10.4% MoM at rank 1; Strawberry Jam Infused Blunt (1g) added +25.3% MoM while holding rank 8. With ranks 1 through 10 all Pre-Roll SKUs and four of the top five posting double-digit MoM gains between +10.4% and +26.3%, the mix indicates demand is concentrating in fruit-forward infused formats, implying 1988 should lean into flavor line-extensions and trade-up packs to consolidate share.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.