Jul-2026

Sales

Trend

6-Month

Product Count

SKUs

Avg Price

YoY Sales Change

YoY Price Change

Where to Buy

Torus is stocked at 125 licensed dispensaries across Washington, with the deepest coverage in Seattle, Tacoma, Bellingham, Spokane, and Bellevue. Search by ZIP code or city below to find the closest one, or filter by product type if you are after a specific format.

Market Insights Snapshot

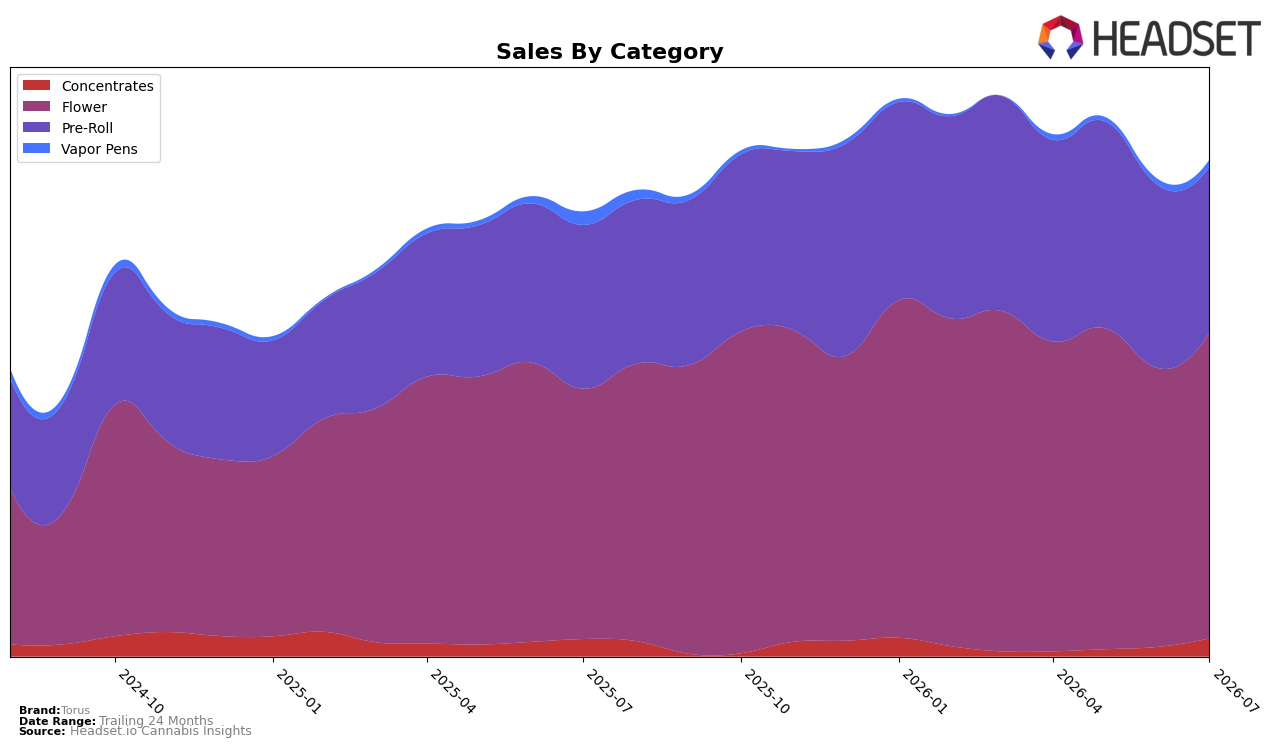

In July 2026, Torus shifted further toward Flower, where share reached 60.13% and category sales grew 21.72% year over year alongside a 9.50% month-over-month lift, while Pre-Roll contracted to 33.06% share with only 1.25% YoY growth and a -9.07% MoM decline. Concentrates expanded to 4.49% share with 3.06% YoY growth and a sharp 58.13% MoM spike, whereas Vapor Pens slipped to 2.32% share with -34.93% YoY contraction despite a 9.86% MoM uptick. With Torus ranked 15 in Flower in Washington and the brand’s average price down 3.59% YoY to $15.24, the pattern implies deliberate volume capture in Flower and opportunistic re-entry in Concentrates, while Pre-Roll is being pared back.

The category mix suggests Torus is concentrating competitive energy where ranking leverage exists in Flower (rank 15) and where near-term velocity is accelerating, as indicated by +9.50% MoM in Flower and +58.13% MoM in Concentrates, while containing exposure in Pre-Roll where MoM fell -9.07% and in Vapor Pens where YoY fell -34.93%. Given overall brand sales up 11.15% YoY and a price-led strategy (-3.59% YoY on average price) coinciding with Flower share at 60.13% and Concentrates momentum, the implication is a positioning pivot toward value-led core Flower volume and selective premiumization in Concentrates, using price and assortment to defend rank in Washington while deprioritizing slower-turn formats.

Competitive Landscape

Torus is ranked #15 in WA Flower for July 2026, improving 2 positions from #17 year over year but falling 5 spots from #10 in April 2026, with a prior peak at #8 in February 2026; meanwhile, Lifted Cannabis Co advanced from #8 to #3 and Sweetwater Farms moved from #14 to #5 as sales grew 48.17%, while Legends held #2 despite a 22.95% sales decline year over year. Compared with Phat Panda steady at #1 with 18.58% YoY sales growth and Mama J's steady at #4 despite a 3.89% decline, Torus’s 2-rank YoY gain alongside a 5-rank three-month slide indicates mid-pack slippage driven by faster-moving rivals, implying that without near-term share wins the brand risks ceding further rank to accelerating competitors.

Notable Products

White Lobster (3.5g) posted the standout move in July 2026 with a +30.7% month-over-month increase, rising to rank 2 while Mint Milkshake (3.5g) advanced +21.6% at rank 3. Four of the top ten are Flower SKUs concentrated between ranks 2 and 6, while Pre-Rolls occupy ranks 1, 5, 7, 8, and 9, indicating share is split between unit-driven Pre-Rolls and premium-priced Flower, with White Lobster Pre-Roll 2-Pack (1g) at rank 1 despite an unreported MoM rate. The mix suggests Torus is leaning into a two-lane strategy where Flower drives growth velocity via double-digit MoM gains and Pre-Rolls anchor breadth at the very top of the ranking, pointing to portfolio balance rather than single-format dependence.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.