Jun-2026

Sales

Trend

6-Month

Product Count

SKUs

Avg Price

YoY Sales Change

YoY Price Change

Market Insights Snapshot

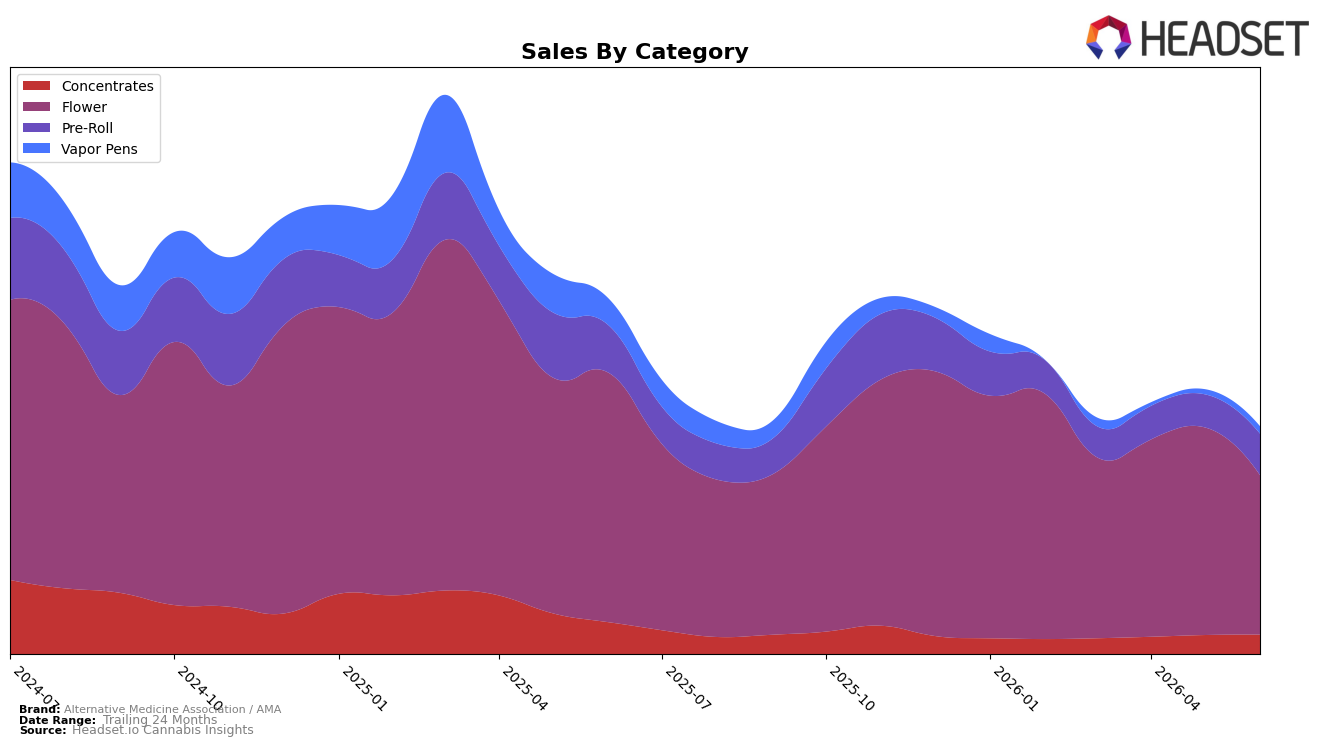

Alternative Medicine Association / AMA’s category mix in June 2026 is concentrated in Flower at 63.3% share with year-over-year down 34.8% and month-over-month down 22.2%, while Pre-Roll holds 19.2% share with year-over-year down 10.6% but month-over-month up 19.7%. Concentrates carry 11.1% share with year-over-year down 29.7% and month-over-month up 1.3%, and Vapor Pens sit at 6.4% share with year-over-year down 53.0% alongside a 15.6% month-over-month rise. With brand-wide sales down 32.4% year over year and average price down 7.6%, the mix indicates a pivot from high-exposure Flower declines toward recovering Pre-Roll and Vapor Pens, implying the brand is relying on lower-priced, faster-turn formats to buffer core-category retrenchment.

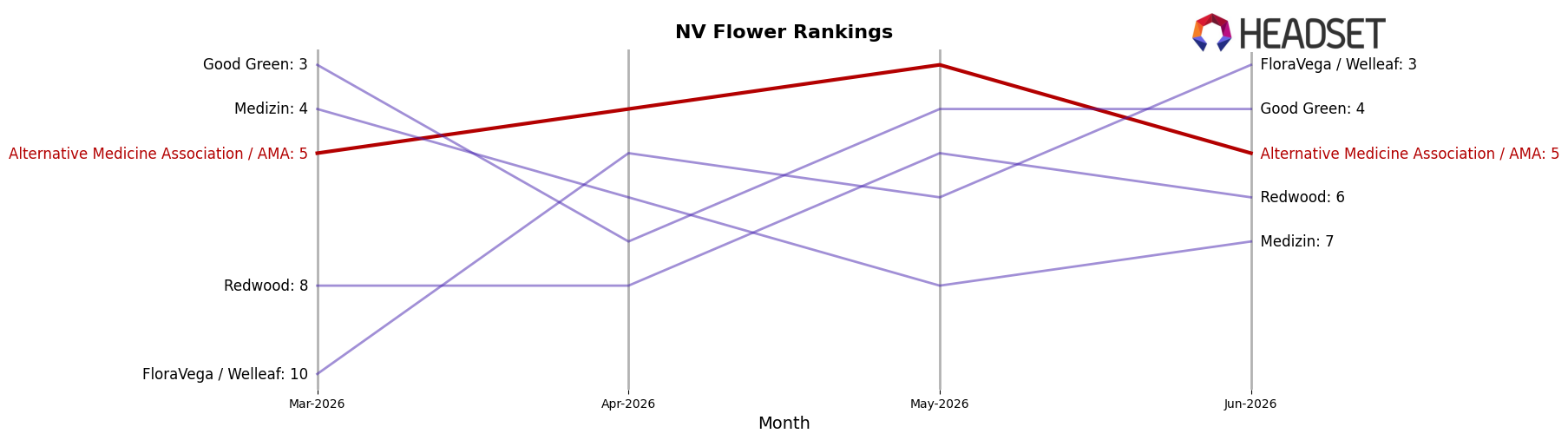

In Nevada Flower, the brand’s rank is 5, a position that contrasts with Flower’s 22.2% month-over-month contraction and 34.8% year-over-year decline, while Pre-Roll’s 19.7% month-over-month lift and Vapor Pens’ 15.6% month-over-month gain suggest momentum in impulse and convenience-led segments. Given the 61.3% sales contraction over 24 months and a 7.6% average price reduction, holding rank 5 in Flower while mix shifts toward Pre-Roll and Vapor Pens implies a defensive repositioning: protect baseline visibility in Flower to sustain shelf presence, while reallocating emphasis to quicker-recovery formats that can stabilize traffic and margin velocity despite category-specific volume pressure.

Competitive Landscape

Alternative Medicine Association / AMA sits at rank #5 in NV Flower in June 2026, down two spots from #3 year over year, while holding flat versus March 2026 at #5; that slip contrasts with STIIIZY maintaining #1 year over year (up 5.2% in sales YoY) and FloraVega / Welleaf surging to #3 from #22 YoY (up 260.4% in sales), even as Good Green dropped to #4 from #5 YoY with a 22.0% sales decline and RYTHM moved to #2 from #4 YoY despite a 6.9% sales contraction; given AMA’s peak at #1 in February 2026 and current #5 placement, the pattern implies share is being ceded to faster-rising peers and that current positioning risks further slippage if the upward trajectories of competitors persist.

Notable Products

Truffle Skunk Pre-Roll (1g) led the movement with a -11.4% month-over-month drop to rank 3, while Scoby (14g) fell -33.6% but still held rank 1. Kush Cake (14g) also declined -33.3% and placed at rank 2, and four of the top ten are Pre-Roll SKUs clustered at ranks 3, 4, 6, and 8 with additional declines of -29.4% and -16.5% among named items. This pattern implies the portfolio is relying on high-share Flower to anchor the leaderboard even as both Flower and Pre-Roll lines contract, signaling a need to rebalance toward fewer, higher-velocity Pre-Rolls to sustain rank stability.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.