Where to Buy

Appalachian Pharm is stocked at 45 licensed dispensaries across Ohio, with the deepest coverage in Cincinnati, Columbus, Lorain, Canton, and Mansfield. Search by ZIP code or city below to find the closest one.

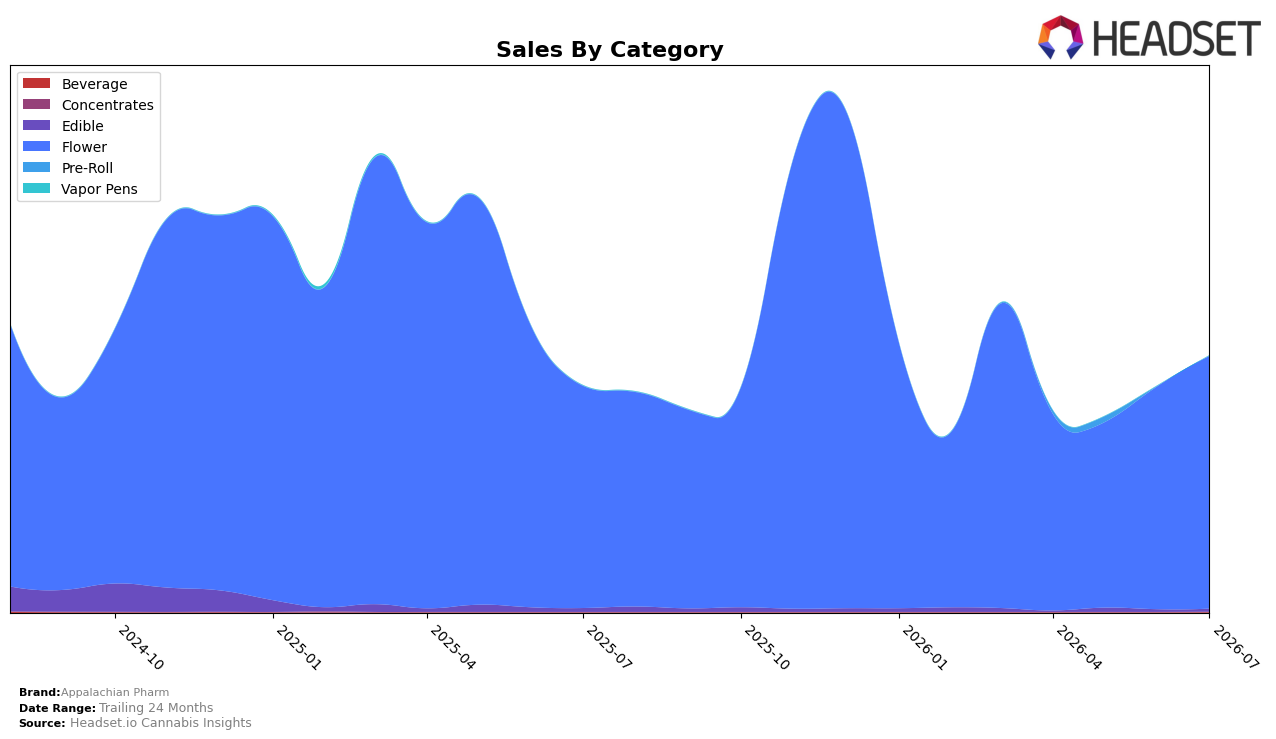

Market Insights Snapshot

Appalachian Pharm’s mix is overwhelmingly concentrated in Flower at 98.90% share, with Flower sales up 13.77% year over year and 13.12% month over month in July 2026, while Edible holds 1.03% share with a 23.61% year-over-year decline but a 16.95% month-over-month lift. Beverage remains nascent at 0.07% share with insufficient trend data. The brand’s average price rose 36.51% year over year to $41.28, while Flower’s average price sits at $42.06, indicating price-led contribution alongside volume; paired with a 13.29% brand-level sales increase year over year, this signals a price-mix strategy anchored in Flower rather than breadth expansion.

The shift points to deeper positioning within Flower rather than diversification: in Ohio Flower the brand sits around rank 23, and a 13.12% month-over-month Flower gain versus a 16.95% month-over-month Edible rebound suggests tactical testing in Edible without material share change from 1.03%. With 62.57% sales growth over 24 months and a 36.51% jump in average price against a 13.77% Flower sales increase, July 2026 implies the brand is prioritizing premiumization in its core category over scaling secondary formats, which concentrates competitive exposure but reinforces a clear single-category value proposition.

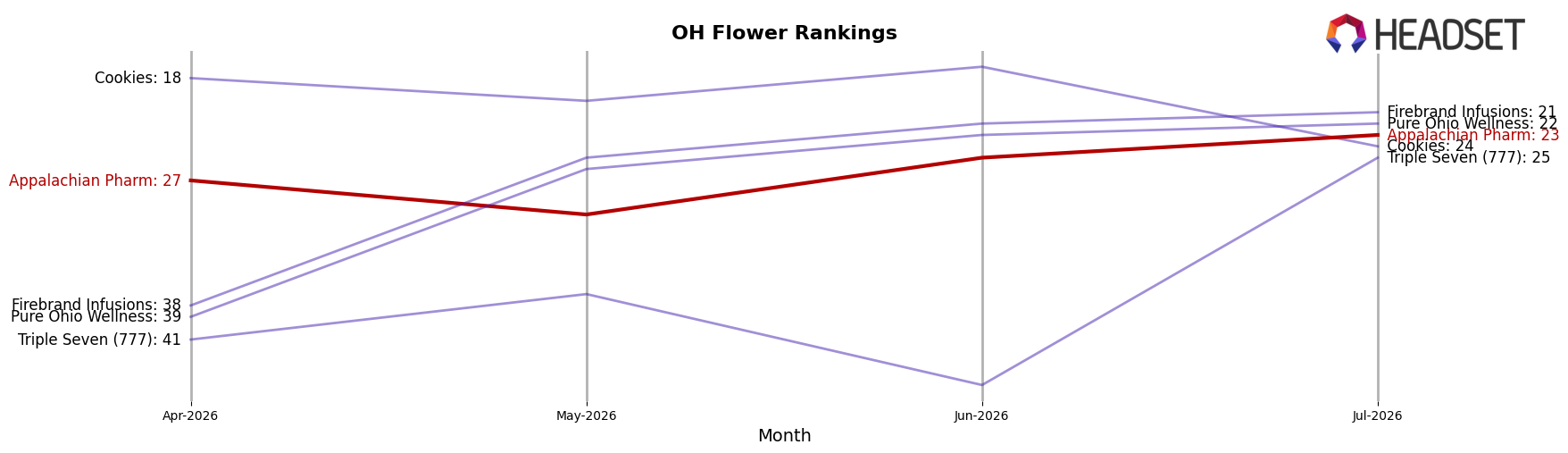

Competitive Landscape

Appalachian Pharm sits at rank #23 in OH Flower in July 2026, unchanged YoY from #23, but up 4 positions from #27 three months ago; that stability contrasts with competitors’ sharper moves, as RYTHM advanced to #1 from #6 YoY with a 74.99% sales increase and Klutch Cannabis jumped to #3 from #21 on 403.04% YoY growth. The brand’s current position trails its peak of #14 reached in March 2025, even as Riviera Creek holds #2 despite a -15.97% YoY sales decline and Certified (Certified Cultivators) climbed to #5 from #14 with 92.83% YoY growth; this mix of upward and downward competitor momentum implies Appalachian Pharm’s static YoY rank masks a loss of relative pace, and the modest 3-month improvement suggests maintenance rather than recovery toward prior peak standing.

Notable Products

Astro Fizz (3.5g) posted the largest month-over-month gain at 129.2% to rank 5 in July 2026, while Holler Hustle (3.5g) doubled at 100.9% to take rank 1, signaling aggressive velocity at both the premium-eighth and value-eighth ends. Against those gains, Alien Mints (2.83g) fell 54.1% to rank 4 and R Rtz (14.15g) declined 30.6% to rank 8, creating a split where fast-rising 3.5g SKUs offset pressure in select 2.83g and 14.15g formats. With all top ten items in Flower and four of the top ten concentrated in 3.5g SKUs, the mix tilts toward smaller-pack units that can scale quickly. The pattern implies Appalachian Pharm is consolidating share via 3.5g innovation while deemphasizing larger and legacy weights that are losing momentum.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.