Jul-2026

Sales

Trend

6-Month

Product Count

SKUs

Avg Price

YoY Sales Change

YoY Price Change

Where to Buy

Benson Arbor is stocked at 174 licensed dispensaries across Oregon, with the deepest coverage in Portland, Eugene, Bend, Salem, and Medford. Search by ZIP code or city below to find the closest one, or filter by product type if you are after a specific format.

Market Insights Snapshot

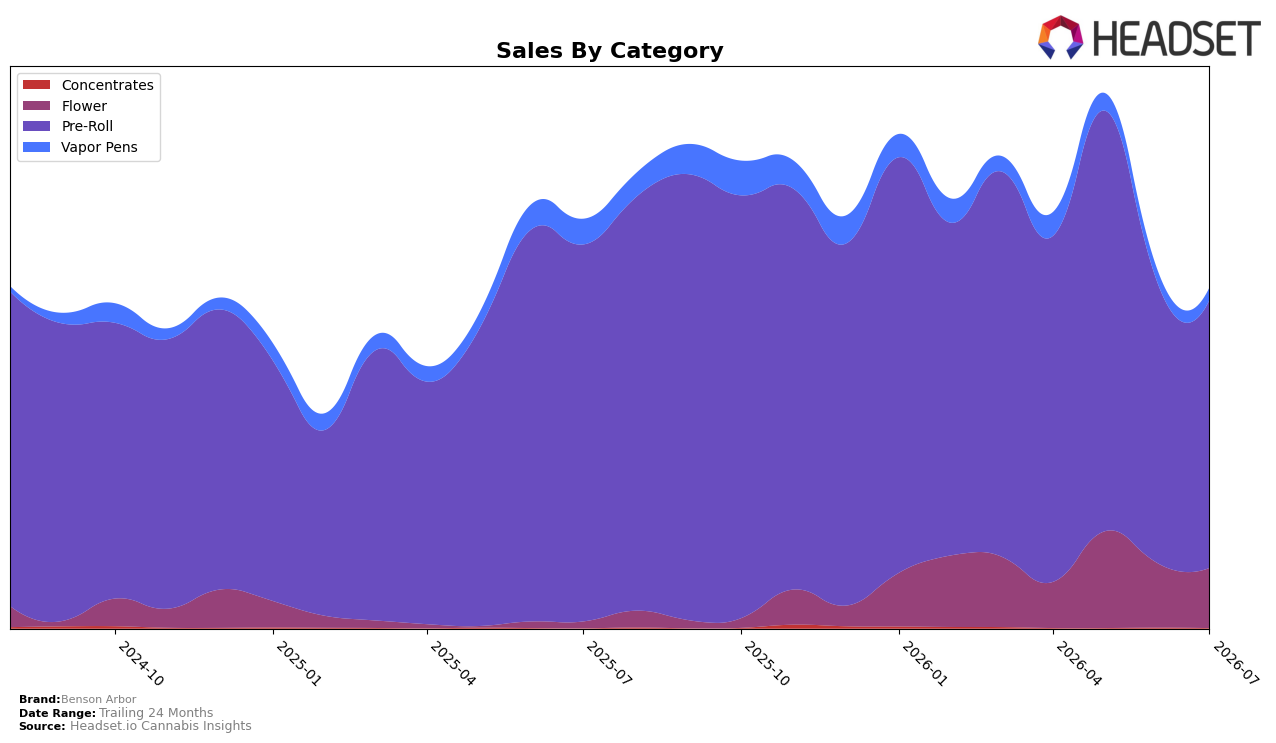

Benson Arbor’s mix in July 2026 is dominated by Pre-Roll at 78.74% share with a year-over-year decline of 29.01% and a month-over-month dip of 4.16%, while Flower climbed to 17.58% share with a year-over-year surge of 828.93% despite a month-over-month decline of 6.47%. Vapor Pens contracted to 3.62% share with a year-over-year decrease of 51.41% and a month-over-month slide of 0.94%, and Concentrates sit at 0.06% share with a steep month-over-month drop of 69.81% and no year-over-year read. With average price down 34.86% year over year to $8.31 and Pre-Roll average price at 7.05, the category mix signals a pivot toward value-led volume in core Pre-Roll while Flower absorbs incremental share despite short-term softness, implying category concentration risk as overall brand sales fell 16.84% year over year.

Holding rank 6 in Pre-Roll in Oregon alongside a 4.16% month-over-month decline and 29.01% year-over-year contraction suggests Benson Arbor is defending a scale position through lower pricing at 7.05 while ceding premium margin to Flower, where average price at 23.87 and 828.93% year-over-year growth indicate a developing upsell lane. The 3.62% Vapor Pens share with a 51.41% year-over-year decline and 0.94% month-over-month dip, combined with Concentrates’ 69.81% month-over-month fall, points to deliberate de-emphasis of small categories; the implied strategy is to stabilize Pre-Roll rank and use Flower’s expanded footprint to diversify revenue so that mix dependence on Pre-Roll (78.74%) does not amplify volatility when pricing compresses.

Competitive Landscape

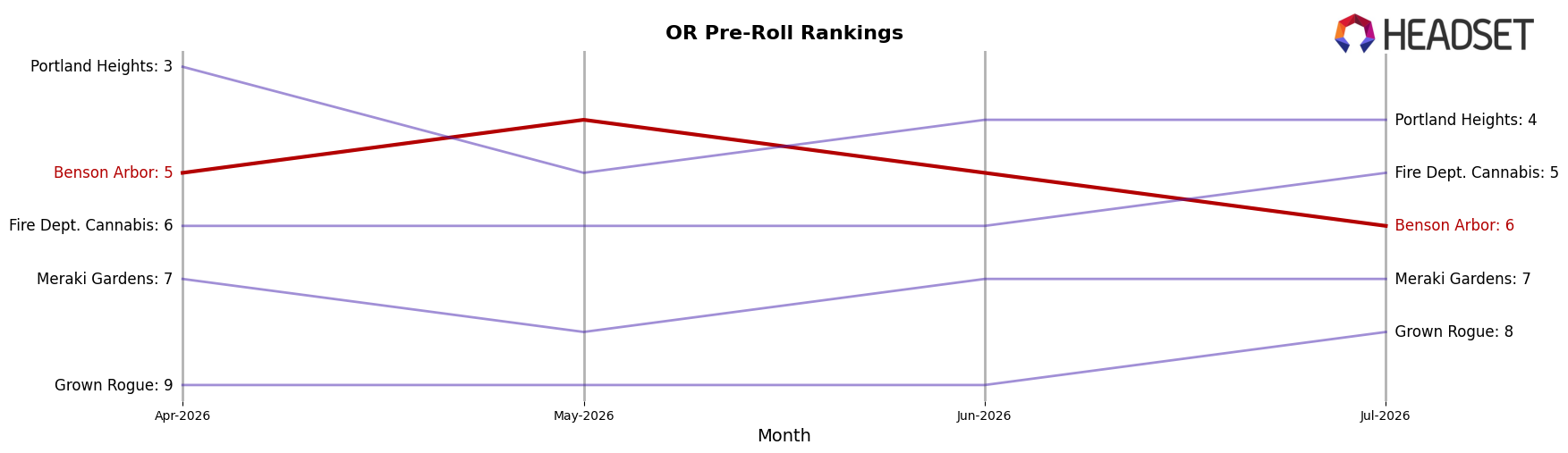

Benson Arbor sits at rank #6 in OR Pre-Roll in July 2026, down 2 positions year over year from #4, after slipping 1 spot from #5 over the last three months; this follows a peak at #2 in January 2026, indicating a downward drift despite prior momentum. In contrast, STiCKS held #1 with a 148.4% YoY sales increase while Kaprikorn advanced from #6 to #2 alongside 144.3% YoY growth, whereas Portland Heights is ranked #4 with a -23.1% YoY sales change; relative to these moves, Benson Arbor’s rank erosion from #2 in January 2026 to #6 in July 2026 implies share is consolidating toward faster-rising leaders and that merely holding mid-table positions risks further displacement.

Notable Products

Chem Fuego #15 Pre-Roll (1g) posted the standout move in July 2026 with a month-over-month gain of 67.0% while climbing to rank 2, whereas Donny Burger Pre-Roll (1g) fell 9.5% and slid to rank 7. Two SKUs share the rank 9 position, indicating compression in the lower top 10, and Tropic Oranges Pre-Roll (1g) dropped 24.4% despite holding that tie, which contrasts with South Fork Kush Pre-Roll (1g) up 11.5% at rank 5. With eight of the top ten as Pre-Roll formats and a single 10-pack drawing $19,469 at rank 8, the mix implies Benson Arbor is concentrating assortment around Pre-Rolls with selective bets on higher-count packs to capture volume without diluting top-tier ranks.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.