Jul-2026

Sales

Trend

6-Month

Product Count

SKUs

Avg Price

YoY Sales Change

YoY Price Change

Where to Buy

Blem is stocked at 418 licensed dispensaries across California, with the deepest coverage in Los Angeles, San Diego, Long Beach, La Mesa, and Sacramento. Search by ZIP code or city below to find the closest one, or filter by product type if you are after a specific format.

Market Insights Snapshot

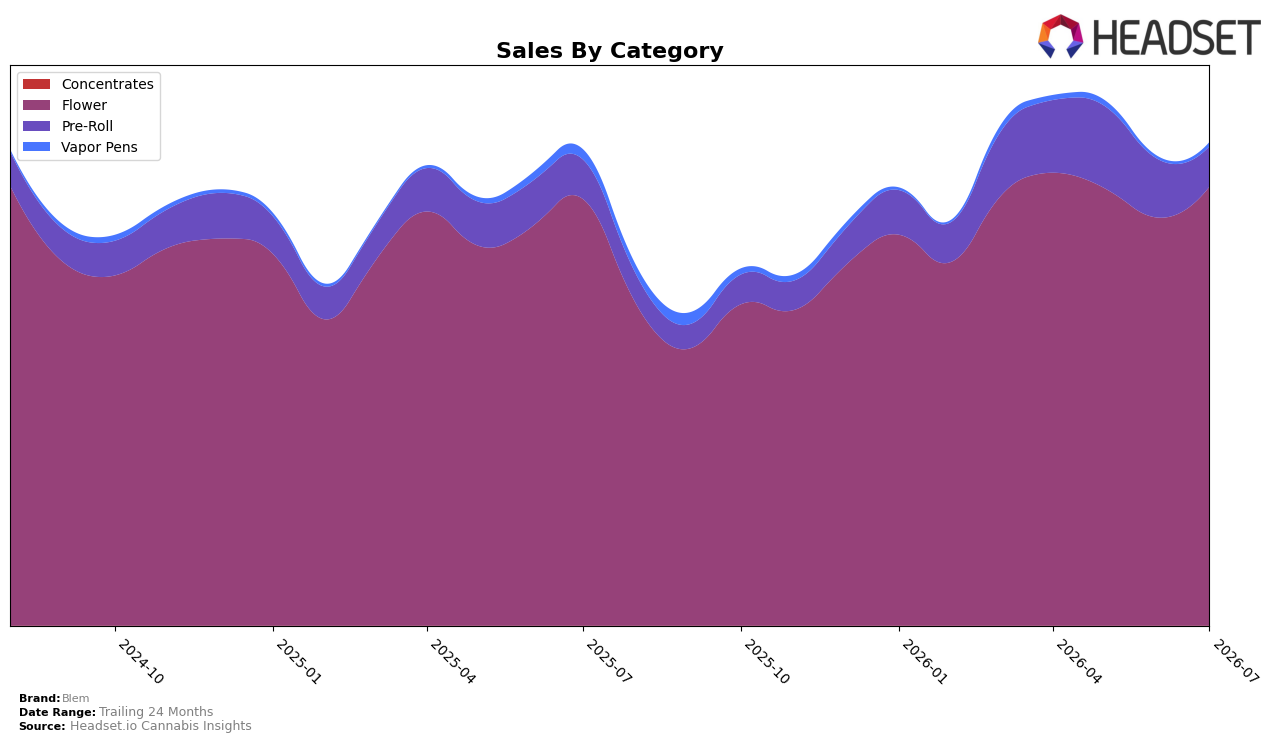

In July 2026, Blem’s category mix concentrated 90.92% of sales in Flower with a 2.94% year-over-year increase and a 7.59% month-over-month lift, while Pre-Roll held 8.28% share with 2.06% YoY growth but a 31.17% MoM decline; Vapor Pens remained a 0.81% sliver with a 60.77% YoY contraction yet a 54.26% MoM rebound. Average price fell 3.90% YoY to $43.36 even as overall brand sales rose 1.54% YoY and 27.25% over 24 months, and Blem ranked 6 in Flower in California. The juxtaposition of a rising Flower share and price deflation implies Blem is using tactical pricing to defend and expand unit velocity in its core category while letting smaller categories absorb volatility.

The 7.59% MoM Flower growth alongside a 31.17% MoM pullback in Pre-Roll indicates a deliberate reallocation toward higher-share SKUs, and the 54.26% MoM uptick in Vapor Pens despite a 60.77% YoY drop suggests opportunistic restocking rather than a strategic pivot. Coupled with a 2.06% YoY gain in Pre-Roll and a 2.94% YoY gain in Flower, the mix shift points to Blem prioritizing depth over breadth to reinforce its rank 6 Flower position in California, implying the brand is trading near-term category diversity for sustained share defense where it already has scale.

Competitive Landscape

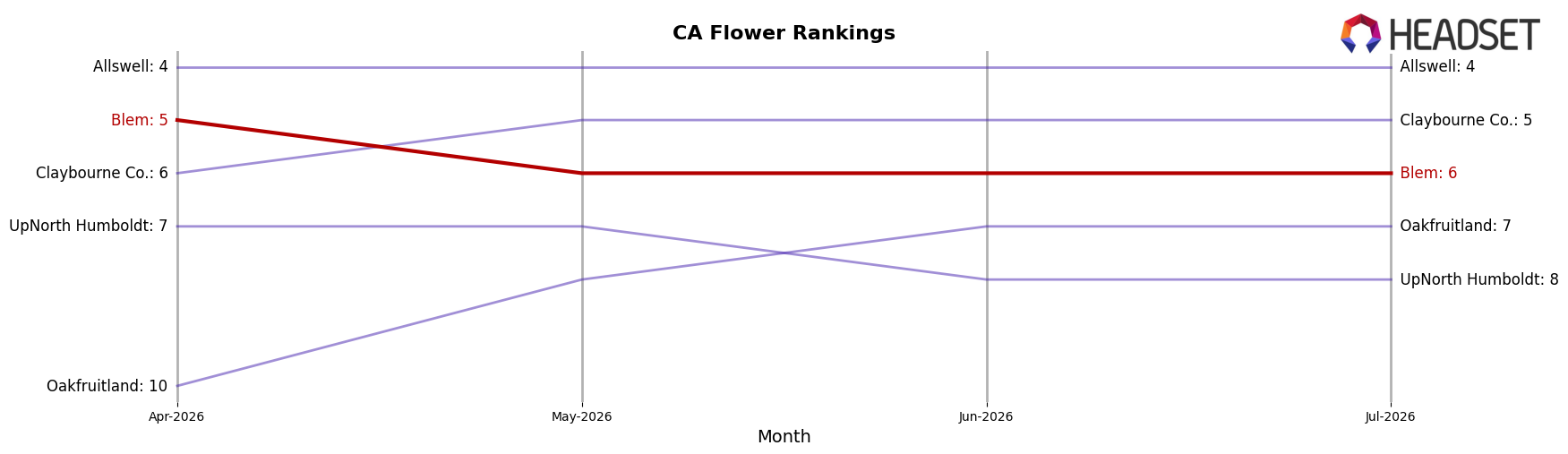

Blem sits at #6 in California Flower in July 2026 with no year-over-year rank movement from #6, and a three-month slide from #5 to #6 that follows a prior peak at #4 in December 2024; in contrast, STIIIZY climbed from #2 to #1 year over year while growing sales by 59.7%, and CAM advanced from #4 to #3 alongside 52.2% sales growth, indicating that upward mobility is concentrating among faster-accelerating peers. With CannaBiotix (CBX) slipping from #1 to #2 despite 7.0% sales growth and Claybourne Co. falling from #3 to #5 with a 1.4% sales decline, Blem’s flat year-over-year rank at #6 and quarter-over-quarter dip from #5 to #6 imply a stall where maintaining share requires reversing the recent down-tick rather than relying on competitor volatility.

Notable Products

Unrully OG Pre-Roll (0.75g) delivered the steepest movement in July 2026 with a -41.4% month-over-month drop while sliding to rank 10, contrasting with Unruly OG (3.5g) rising 11.8% MoM at rank 1. Fiyah (3.5g) climbed 41.9% MoM at rank 4, yet the Unruly Pre-Roll 5-Pack (3.75g) fell -17.7% at rank 5; together these shifts indicate pre-rolls are losing share even as core Flower regains momentum. Four of the top ten are Flower SKUs, including Unruly OG (10g) holding rank 2 with a 4.3% MoM uptick and Tangie Ting (3.5g) at rank 3 with a 3.1% MoM gain, while BluBeri (3.5g) dipped -8.1% at rank 6; this concentration suggests assortment depth in Flower is driving placement resilience. With July 2026 revenue anchored by Unruly OG (10g) at $656,390 and multiple Flower SKUs posting positive MoM while pre-rolls contract, the product mix points toward prioritizing high-velocity Flower formats over pre-roll extensions for near-term growth.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.