Jul-2026

Sales

Trend

6-Month

Product Count

SKUs

Avg Price

YoY Sales Change

YoY Price Change

Where to Buy

Allswell is stocked at 176 licensed dispensaries across California, with the deepest coverage in Los Angeles, San Diego, Sacramento, San Jose, and San Francisco. Search by ZIP code or city below to find the closest one, or filter by product type if you are after a specific format.

Market Insights Snapshot

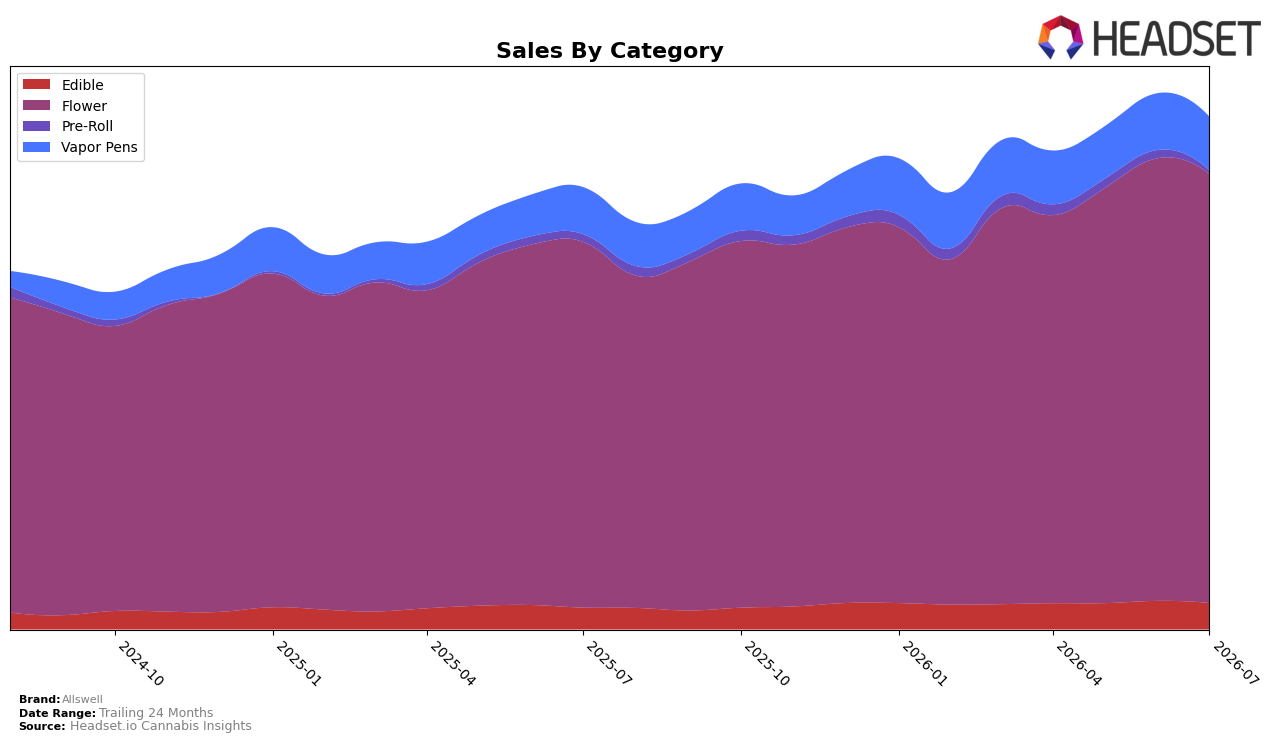

Allswell concentrated 83.06% of July 2026 sales in Flower, up 17.26% year over year but down 3.08% month over month, while Vapor Pens held 10.63% share with 13.76% YoY growth and a 5.27% MoM decline. Edible reached 5.37% share with 19.83% YoY growth but fell 7.03% MoM, and Pre-Roll slipped to 0.93% share with a 46.42% YoY drop and a 49.51% MoM contraction. With overall brand sales up 15.73% YoY and average price down 4.23% YoY to $15.35, the pattern implies volume-led gains concentrated in Flower are offsetting near-term pullbacks across smaller formats.

The heavy Flower mix aligns with a rank of 4 in Flower in California, but the 3.08% MoM retreat in Flower alongside a 5.27% MoM decline in Vapor Pens indicates exposure to short-cycle volatility; simultaneously, Edible’s 19.83% YoY growth versus Pre-Roll’s 46.42% YoY decline signals a bifurcation toward ingestibles over impulse formats. Given a 57.35% two-year sales increase and a 4.23% YoY price deflation, the positioning implication is value-forward in Flower with selective upside in Edible, while Vapor Pens requires stabilization and Pre-Roll likely warrants deprioritization to preserve rank and margin consistency.

Competitive Landscape

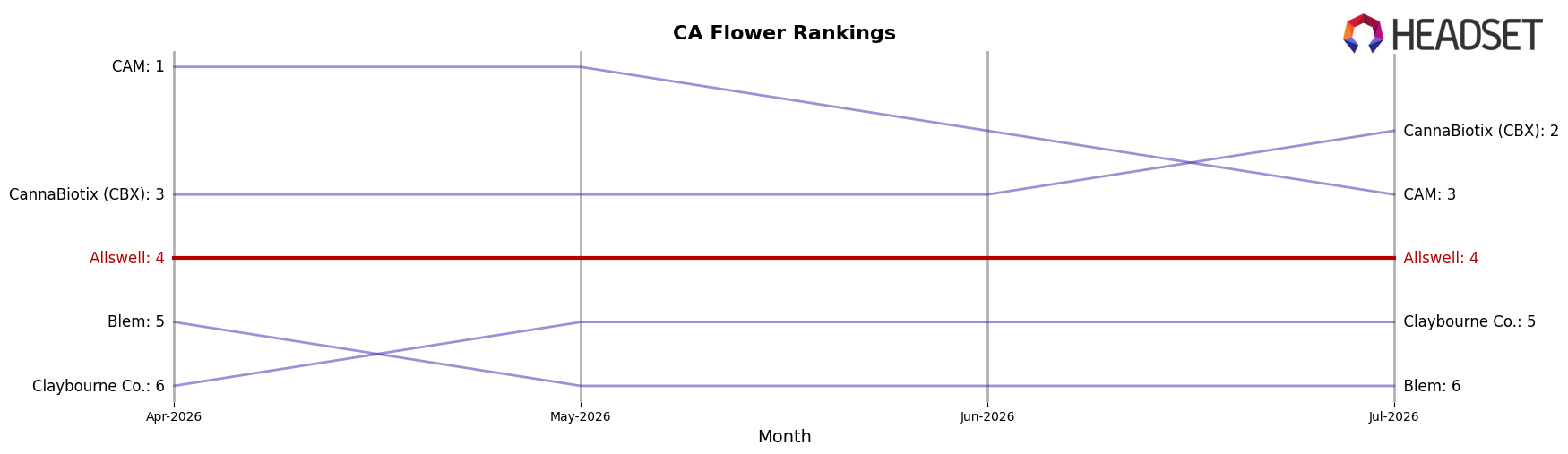

Allswell is ranked #4 in California Flower in July 2026, improving 1 position from #5 year over year, while holding the same #4 spot over the past three months; this places it just behind CAM, which advanced from #4 to #3 as its sales grew 52.19% year over year, and below STIIIZY, which climbed from #2 to #1 with 59.66% YoY sales growth, whereas Claybourne Co. fell from #3 to #5 with a -1.37% YoY decline; compared to July 2026 peak alignment at #4 and a modest 1-rank YoY gain, the pattern implies Allswell has stabilized in upper-tier contention but must convert relative momentum against faster-climbing leaders to break into the top three.

Notable Products

Sweet Fruit Punch Gummies 10-Pack (100mg) posted the steepest decline at -18.5% month over month while holding rank 3, and Sweet Berry Dream Gummies 10-Pack (100mg) slipped -18.4% at rank 4, signaling erosion in mid-tier Edible demand despite stable top-5 placement. Sour Blue Raspberry Gummies 10-Pack (100mg) fell -9.5% yet remained rank 1, whereas Sour Kiwi Strawberry Gummies 10-Pack (100mg) dipped -2.0% at rank 2, and five of the top ten are Edible SKUs, concentrating share in gummies even as growth cools. Orange Phantom (14g) entered at rank 7 with $79,122 and no prior-month baseline, contrasting with Sour Tropical Blast Gummies 10-Pack (100mg) at +8.8% and rank 5, which indicates Flower is re-emerging as a volume counterweight while Edibles consolidate at the top. Taken together, the mix points to Allswell leaning on a broad gummy lineup for rank consistency while seeding Flower to diversify momentum and hedge against Edible volatility.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.