Jul-2026

Sales

Trend

6-Month

Product Count

SKUs

Avg Price

YoY Sales Change

YoY Price Change

Where to Buy

Claybourne Co. is stocked at 587 licensed dispensaries across California, New York, and Nevada, 423 of them in California, with the deepest coverage in Los Angeles, San Diego, Sacramento, Santa Ana, and San Jose. Search by ZIP code or city below to find the closest one, or filter by product type if you are after a specific format.

Market Insights Snapshot

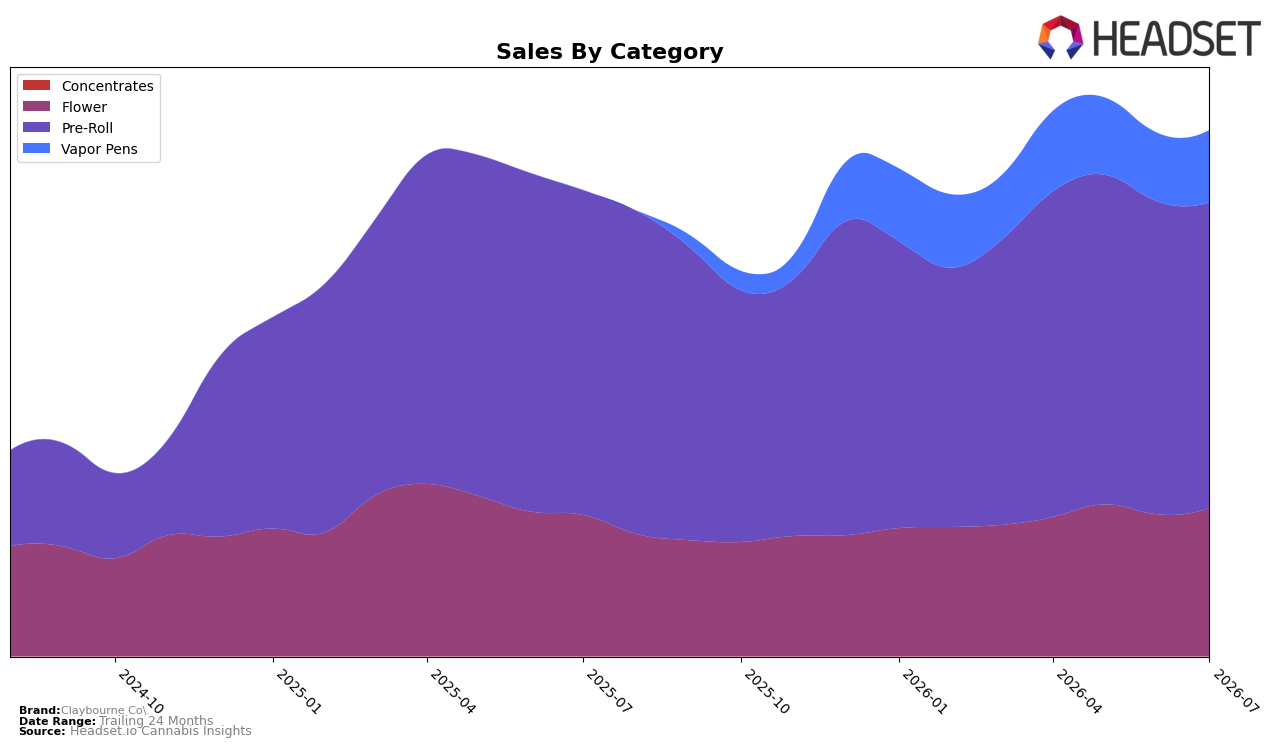

Claybourne Co.'s mix in July 2026 is concentrated in Pre-Roll at 58.16% share, yet that category declined both year over year by 5.82% and month over month by 2.21%, while Flower rose 4.90% YoY and 4.44% MoM to 28.14% share. Vapor Pens expanded to 13.69% share with a 5.55% MoM gain, and Concentrates contracted to 0.00% share with a 34.19% MoM drop, alongside a brand-level average price decline of 2.27% YoY to $30.46. This pattern implies the brand is relying less on a shrinking Pre-Roll base and gradually rebalancing toward Flower and Vapor Pens to stabilize topline growth of 12.89% YoY despite price compression.

Holding rank 5 in Flower in California while Flower sales grew 4.90% YoY and 4.44% MoM suggests Claybourne Co. can lean on mid-tier leadership to offset Pre-Roll softness of 5.82% YoY and 2.21% MoM. With Vapor Pens adding 5.55% MoM on a 13.69% mix and the brand’s average price down 2.27% YoY, the attainable path is to deepen Flower positioning where it already ranks 5 and use pricing latitude to convert Pre-Roll shoppers, implying a shift toward categories with better momentum and rank headroom.

Competitive Landscape

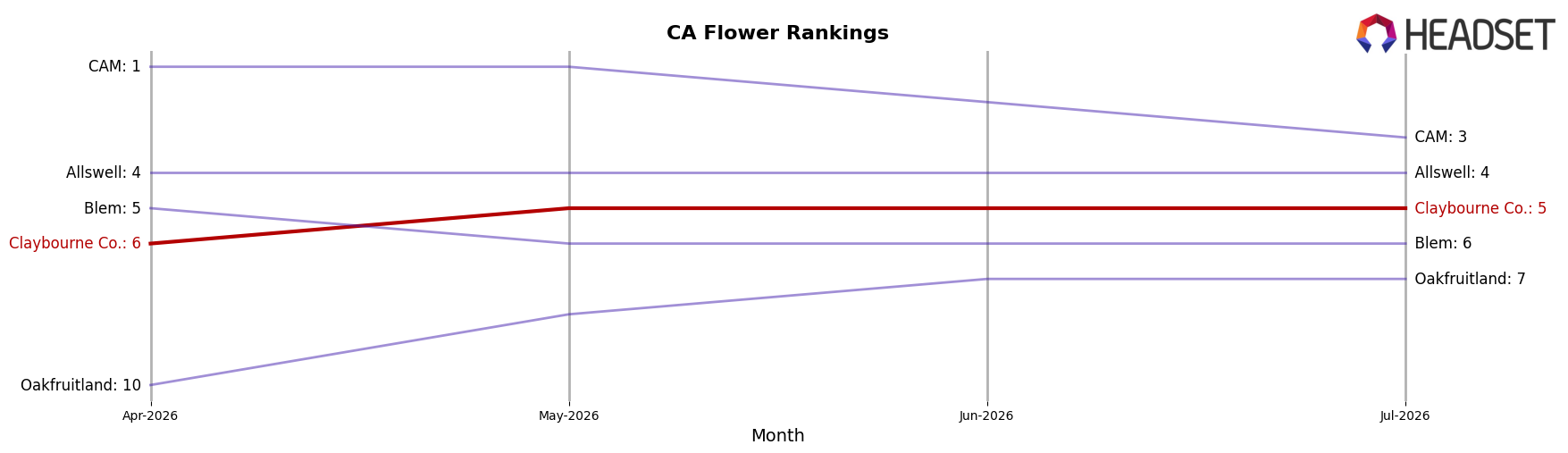

Claybourne Co. sits at rank #5 in California Flower in July 2026, down 2 positions year over year from #3, and up 1 spot from #6 three months ago; against this backdrop, STIIIZY advanced to #1 from #2 with sales up 59.7% YoY while CAM climbed to #3 from #4 with 52.2% YoY growth. Claybourne Co. last peaked at #2 in April 2025 and now trails Allswell, which moved to #4 from #5 with 17.3% YoY growth; the combination of a 2-rank YoY slide and only a 1-rank recovery since April 2025 implies the brand is losing relative velocity to faster-rising leaders and must outperform category growth to regain a top-three position.

Notable Products

Flyers - Blue Dream Frosted Liquid Diamond Infused Pre-Roll 8-Pack (2.8g) posted the sharpest movement in July 2026 with a -33.3% month-over-month drop and slid to rank 10, while the adjacent Blue Dream 3-Pack fell -17.9% at rank 4. In contrast, Frosted Flyers - Variety Pack Infused Pre-Roll 5-Pack (2.5g) inched up +4.6% and held rank 1, and Flower anchor Mule Fuel (3.5g) rose +4.8% to rank 5. With eight of the top ten coming from Pre-Rolls yet two Blue Dream formats declining by double digits, the pattern implies concentration risk in one flavor profile even as the flagship multipack sustains leadership.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.