Jul-2026

Sales

Trend

6-Month

Product Count

SKUs

Avg Price

YoY Sales Change

YoY Price Change

Market Insights Snapshot

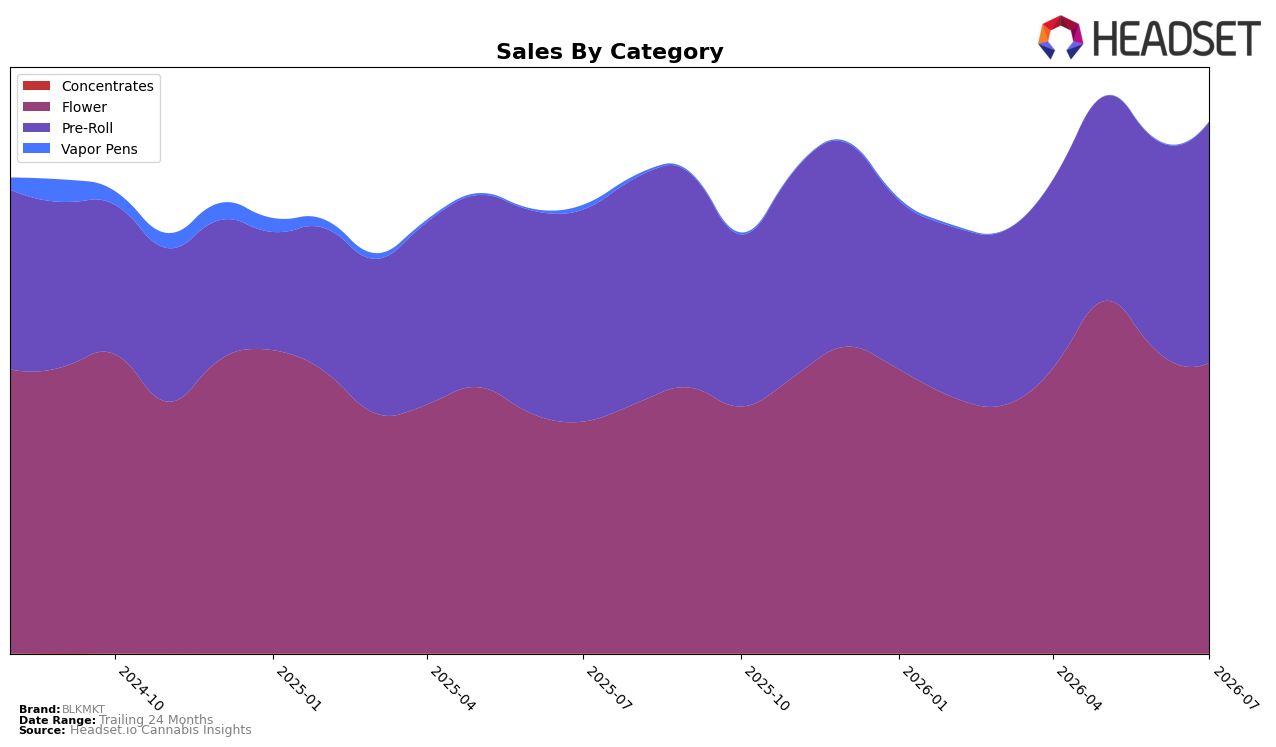

In July 2026, BLKMKT’s category mix is concentrated in Flower at 54.65% share and Pre-Roll at 45.30% share, with Vapor Pens at 0.05% share. Flower grew 25.40% year over year but slid 3.46% month over month, while Pre-Roll rose 13.74% year over year and advanced 14.19% month over month; the combined effect is a tilt toward Pre-Roll momentum despite Flower’s larger base. Vapor Pens contracted 93.61% year over year and 49.94% month over month from a negligible base, indicating deliberate retrenchment. With an average price up 12.46% year over year and the brand ranked 21 in Flower in Ontario, the pattern implies BLKMKT is reinforcing premium Flower while using Pre-Roll growth to buffer short-term volume variability.

The divergence between a 3.46% month-over-month decline in Flower and a 14.19% month-over-month increase in Pre-Roll suggests BLKMKT is shifting incremental effort toward formats that convert faster without diluting the Flower position at rank 21 in Ontario. With brand sales up 18.71% year over year against a 12.46% year-over-year price increase, unit velocity likely expanded, and the near exit from Vapor Pens at 0.05% share removes low-yield complexity. The mix implies a barbell: protect Flower’s 54.65% share for margin while using Pre-Roll’s 45.30% share and double‑digit month-over-month lift to capture replenishment-driven trips, positioning BLKMKT to trade buyers up in Flower while maintaining basket frequency via Pre-Roll.

Competitive Landscape

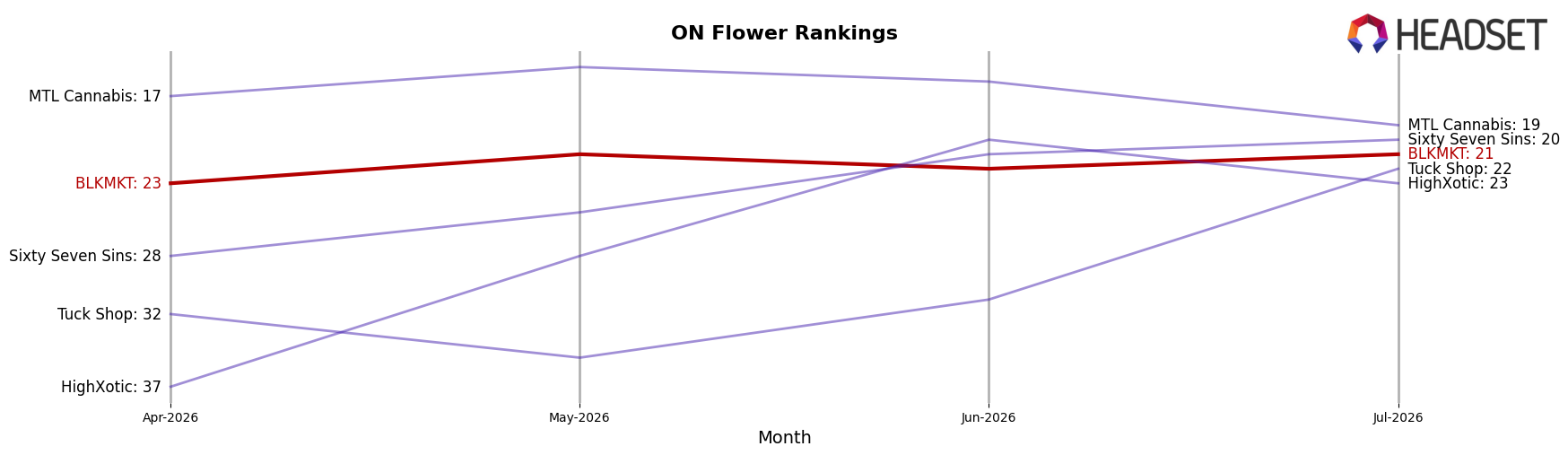

BLKMKT sits at rank #21 in Ontario Flower in July 2026, improving 7 positions year over year from #28, but slipping 2 spots versus April 2026’s #23; against a longer arc, the brand remains below its peak #19 from July 2024, while category leaders moved upward more decisively. For example, Shred advanced from #2 to #1 with 17.2% YoY sales growth, and Spinach climbed from #4 to #2 on 31.1% YoY growth, whereas Back Forty / Back 40 Cannabis fell from #1 to #4 alongside a -5.4% YoY decline; this spread indicates BLKMKT’s YoY rank gain coincides with top-tier consolidation, and the recent 2-position dip suggests the brand risks being squeezed between accelerating leaders and softening incumbents unless it reaccelerates share momentum.

Notable Products

Britscotti Glass Cannon Blunt (1g) posted the steepest decline at -9.3% month over month, slipping while Jealousy Pre-Roll (1g) climbed 15.5% to rank 2 and Rainbow P Pre-Roll (1g) in rank 1 inched up 2.7%. Red Dragon Pre-Roll (1g) advanced 34.0% to rank 6, and Noir Diamant Pre-Roll 5-Pack (2.5g) rose 17.9% while Red Velvet Blunt (1g) was nearly flat at +0.7%. Nine of the top ten are Pre-Roll SKUs, and the lone Flower entry, Exclusives (7g), gained 11.6% to sit at rank 10 with $94,377 in July 2026 sales. The pattern implies BLKMKT is leaning further into Pre-Rolls as the commercial core while treating Flower as a selective, momentum-supporting adjunct.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.