Jun-2026

Sales

Trend

6-Month

Product Count

SKUs

Avg Price

YoY Sales Change

YoY Price Change

Market Insights Snapshot

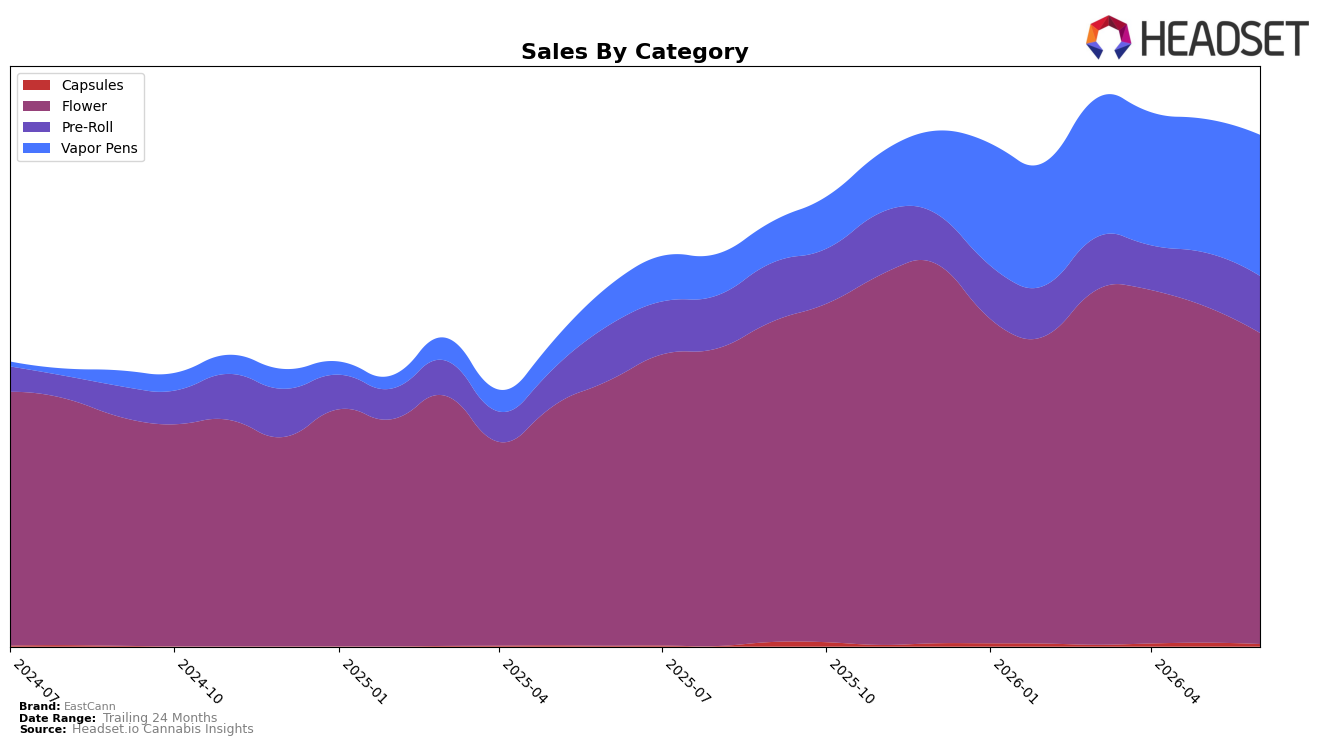

EastCann’s mix in June 2026 skews toward Flower at 60.9% share despite a month-over-month decline of 7.6%, while Vapor Pens climbed to 27.6% share on 262.6% year-over-year growth and a 5.7% month-over-month increase. Pre-Roll holds 11.1% share with modest 3.4% year-over-year growth and a 6.3% month-over-month uptick, as Capsules remain niche at 0.46% share with a 256.2% year-over-year surge but a 35.8% month-over-month drop. The brand’s average price rose 7.1% year over year to $42.95, and Flower’s average price sits higher at $50.27 relative to Vapor Pens at $38.42, indicating a premium-weighted core even as the growth engine shifts. Taken together, the expansion of Vapor Pens alongside Flower’s pullback implies that June 2026 marks a pivot from a single-category anchor toward a dual-engine portfolio, with mix risk reducing as share concentrates less in Flower and more in faster-growing Vapor Pens.

With Flower ranked 25th in the category in Ontario, the 17.4% year-over-year gain but 7.6% month-over-month dip suggests competitive pressure within the core, while Vapor Pens’ 262.6% year-over-year growth and 5.7% month-over-month rise signal a route to improve shelf relevance without relying on Flower rank alone. Pre-Roll’s 6.3% month-over-month increase alongside only 3.4% year-over-year growth indicates tactical upside but limited structural contribution versus Vapor Pens, and Capsules’ 35.8% month-over-month decline despite 256.2% year-over-year growth points to volatility best treated as opportunistic rather than strategic. The pattern implies EastCann’s positioning should lean into Vapor Pens to capture momentum while defending Flower share and price architecture, using Pre-Roll as a consistency buffer and keeping Capsules as a low-risk test bed.

Competitive Landscape

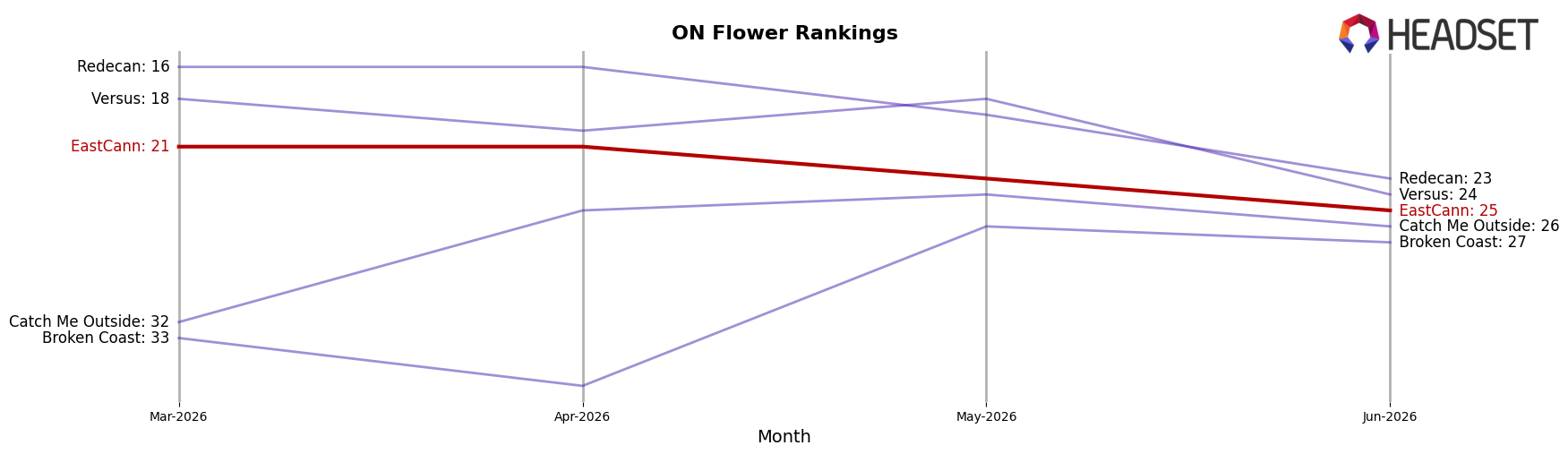

EastCann sits at rank #25 in ON Flower in June 2026, improving 2 spots from rank #27 year over year, but sliding 4 positions from its three-month peak at #21 in April 2026; against this backdrop, Spinach climbed from #4 to #1 while growing sales by 38.3%, and Back Forty / Back 40 Cannabis fell from #1 to #4 with an 11.3% sales decline, indicating that EastCann’s modest rank gain alongside top-tier volatility points to a mid-pack foothold that requires sharper share capture to avoid further drift from its April 2026 peak.

Notable Products

Chopper's Pick (28g) posted the steepest movement in June 2026 with a -33.8% month-over-month drop while sliding to rank 6, and Frozen Lemons Live Resin Cartridge (1g) fell -36.9% to rank 9; this tandem decline alongside Purple Kush Live Resin Cartridge (1g) at -11.6% and rank 4 signals a reset in larger pack Flower and select Live Resin SKUs. Velvet Z (7g) held rank 1 despite a -4.2% dip, while Velvet Z (1g) rose +21.4% to rank 3 and Mango Sour Cured Resin Cartridge (1g) climbed +34.3% to rank 2, indicating the brand is concentrating volume into a few leaders even as mid-pack volatility rises. Four of the top ten are Vapor Pens while four are Flower, and the mixed direction—Vapor Pens split between +34.3% at rank 2 and declines of -11.6% and -36.9%—implies tighter SKU pruning around winners and de-emphasis of lagging Live Resin formats. The pattern points to EastCann tilting assortment toward high-velocity sizes and curated vape offerings to stabilize rank leadership and margin amid sharper declines in bulk Flower.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.