Jun-2026

Sales

Trend

6-Month

Product Count

SKUs

Avg Price

YoY Sales Change

YoY Price Change

Market Insights Snapshot

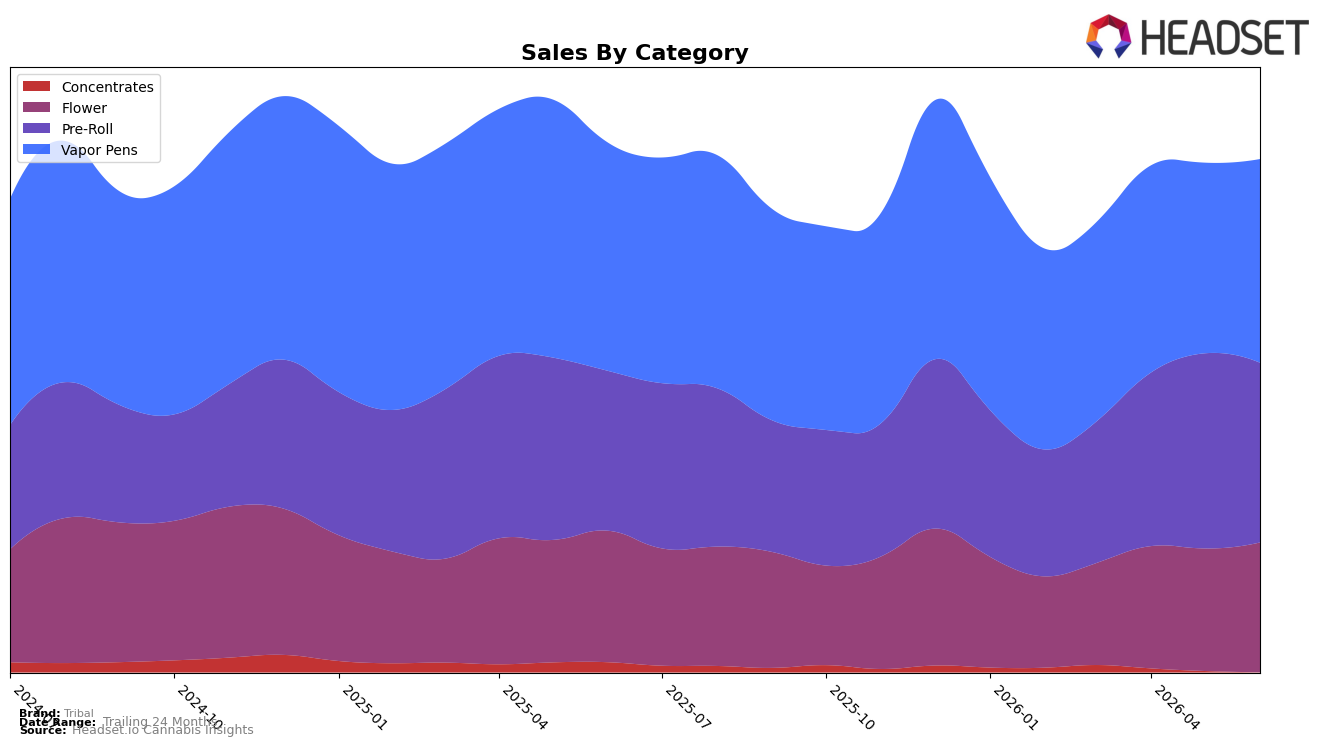

Tribal’s category mix in June 2026 tilted toward Vapor Pens at 38.72% share with a 6.54% month-over-month lift but a 10.31% year-over-year decline, while Pre-Roll held 34.34% share with an 11.77% year-over-year increase but a 7.57% month-over-month drop. Flower accounted for 25.27% share with a 5.55% month-over-month increase and a 1.16% year-over-year dip, and Concentrates fell to 1.67% share with a 12.41% month-over-month contraction and a 52.32% year-over-year pullback. With overall brand sales down 2.88% year over year and average price down 21.08% year over year to $26.27, the mix suggests Tribal is leaning on lower-priced volume in Pre-Roll and stabilizing Flower to offset Vapor Pens’ year-over-year pressure, implying a recalibration toward mid-ticket, high-velocity formats.

These shifts imply Tribal is prioritizing breadth over depth: Vapor Pens still anchor position at 38.72% share and a rank of 7 in Vapor Pens in Ontario, yet the 10.31% year-over-year decline contrasts with Pre-Roll’s 11.77% year-over-year growth, indicating a pivot toward formats that convert under tighter pricing. The 5.55% month-over-month rebound in Flower alongside a 7.57% month-over-month dip in Pre-Roll signals short-term cannibalization risk between adjacent value tiers, and the 52.32% year-over-year drop in Concentrates concentrates Tribal’s positioning away from niche potency plays; together, these patterns point to a strategy anchored in accessible inhalables where price elasticity can sustain share despite category-level headwinds.

Competitive Landscape

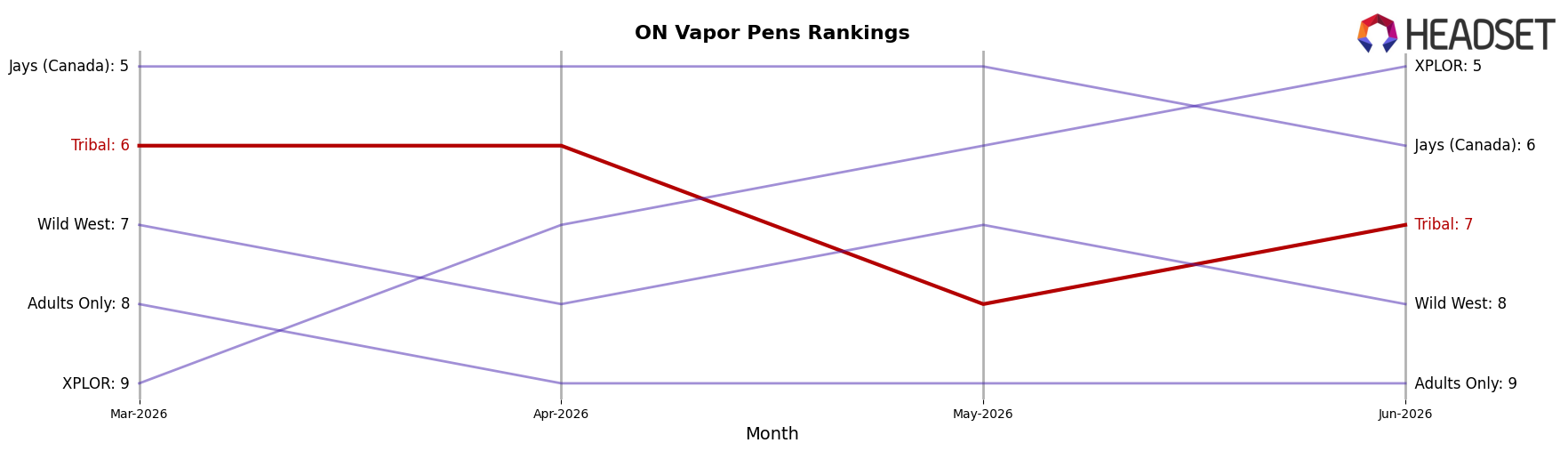

Tribal sits at rank #7 in ON Vapor Pens in June 2026, down 1 position from rank #6 year over year, and 1 position lower than March 2026 when it was #6; by contrast, Spinach climbed from #5 to #1 with a 173.8% year-over-year sales increase while BoxHot slipped from #1 to #3 alongside a 22.1% sales decline. Tribal’s peak at #5 in February 2026 and a 1-rank slide over the last three months (from #6 in March 2026 to #7 in June 2026) signal share pressure as ladder-movers consolidate the top tier; the pattern implies Tribal is stabilizing mid-pack rather than reclaiming its February 2026 peak without a change in mix or activation.

Notable Products

The steepest decline sets the tone: Cuban Linx Pre-Roll (1g) fell 72.9% month over month while still holding rank 1, and Neon Sunshine Pre-Roll (1g) dropped 21.1% at rank 2. Bubble Up (3.5g) slid 24.2% at rank 10 alongside Gran Turismo (3.5g) down 22.5% at rank 7. With four of the top ten in Pre-Roll, the category is concentrated at the top even as single-count SKUs retrench, implying Tribal is leaning on format breadth rather than velocity per SKU to defend share.

Countering the pullback, Cuban Linx Live Resin Cartridge (1g) in Vapor Pens grew 3.2% at rank 5 while Cuban Linx Pre-Roll 5-Pack (2.5g) rose 9.4% at rank 4, together accounting for $829,000 in June 2026. Cuban Linx (3.5g) hovered just inside the top ten at rank 8 with a 9.9% decline, and Gran Turismo Pre-Roll 5-Pack (2.5g) was effectively flat at rank 6 with a 0.3% dip. The pattern implies a pivot toward multi-pack Pre-Rolls and inhalable derivatives absorbing demand as single-counts and eighths soften, steering Tribal’s mix toward bundle value and device-compatible formats.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.