Jun-2026

Sales

Trend

6-Month

Product Count

SKUs

Avg Price

YoY Sales Change

YoY Price Change

Market Insights Snapshot

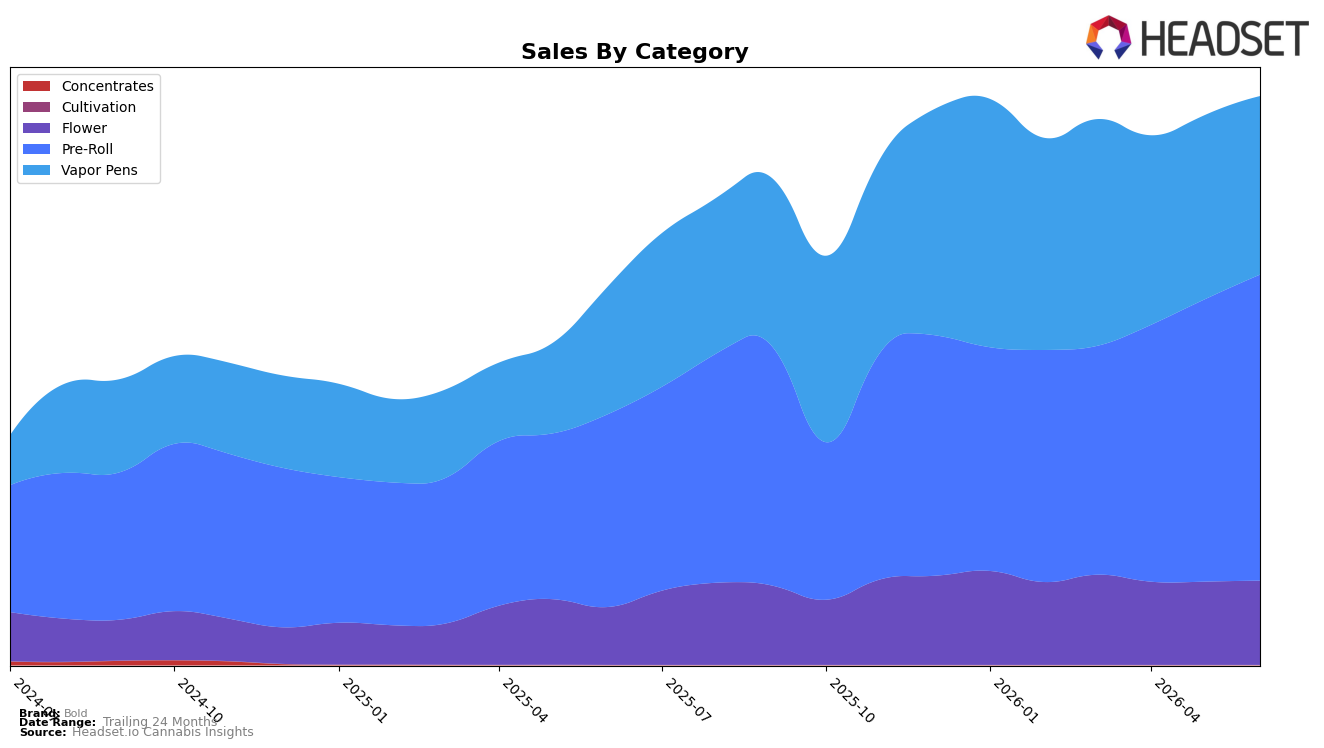

In June 2026, Bold’s mix tilted further toward Pre-Roll at 53.83% share, up alongside a 58.72% year-over-year lift and an 8.42% month-over-month gain, while Vapor Pens held 31.38% share with 39.55% YoY growth but a 3.09% MoM decline; Flower rounded out at 14.78% share with 45.69% YoY and 1.20% MoM growth. Against a brand-level 50.25% YoY sales increase and a 6.74% YoY drop in average price, the divergent MoM paths—Pre-Roll up 8.42% versus Vapor Pens down 3.09%—indicate volume-led expansion concentrated in value-oriented formats. The pattern implies Bold is pulling incremental units through Pre-Roll while accepting price pressure, using category breadth to offset a softer month in Vapor Pens and preserve overall momentum.

Despite Vapor Pens being the top category for Bold by capability context, the on-the-ground mix now favors Pre-Roll at 53.83% versus 31.38% for Vapor Pens, and the June 2026 rank of 2 in Vapor Pens within Saskatchewan contrasts with the 3.09% MoM decline in that category while Pre-Roll advanced 8.42%. With Flower steady at 1.20% MoM growth and a higher average price point at 50.46 versus 18.72 in Pre-Roll, the brand’s 6.74% YoY price decrease suggests a deliberate elasticity tradeoff that favors unit capture in lower-priced formats even as Vapor Pens sustains a 39.55% YoY increase. The positioning implication is that Bold is leaning into a value-led, unit-accretive Pre-Roll engine to stabilize share while keeping a premium-adjacent foothold via Vapor Pens performance and a price ladder anchored by Flower.

Competitive Landscape

Bold sits at rank #2 in SK Vapor Pens in June 2026, unchanged year over year at #2, after slipping from #1 three months ago and from a peak at #1 in March 2026; in contrast, Spinach holds #1 both currently and year over year while growing sales 24.2%, and Versus surged from #24 year over year to #4 with 702.9% sales growth. Meanwhile, Back Forty / Back 40 Cannabis remains steady at #3 YoY with 76.2% growth and General Admission advanced to #5 from #9 YoY on 104.2% growth; this pattern implies Bold’s flat YoY rank at #2 masks rising competitive pressure from faster-climbing peers, signaling a defense phase to protect share rather than a trajectory toward reclaiming #1.

Notable Products

Peachy Pie Pre-Roll 3-Pack (1.5g) posted the largest month-over-month gain at 37.3% while rising to rank 5, contrasted with Melted Strawberry Diamond Infused Pre-Roll 5-Pack (2g) slipping 3.0% at rank 3. Glazed Pre-Roll 2-Pack (2g) held rank 1 with a 34.0% increase and approximately $280,830 in June 2026, as Glazed - Juicy Pineapple Liquid Diamonds Cartridge (1g) fell 6.0% at rank 8. With eight of the top ten SKUs in Pre-Roll formats and only one Vapor Pens SKU in the top eight, the pattern implies Bold’s near-term commercial direction is consolidating around multi-pack pre-rolls with selective flavor extensions driving velocity at the very top.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.