Jun-2026

Sales

Trend

6-Month

Product Count

SKUs

Avg Price

YoY Sales Change

YoY Price Change

Market Insights Snapshot

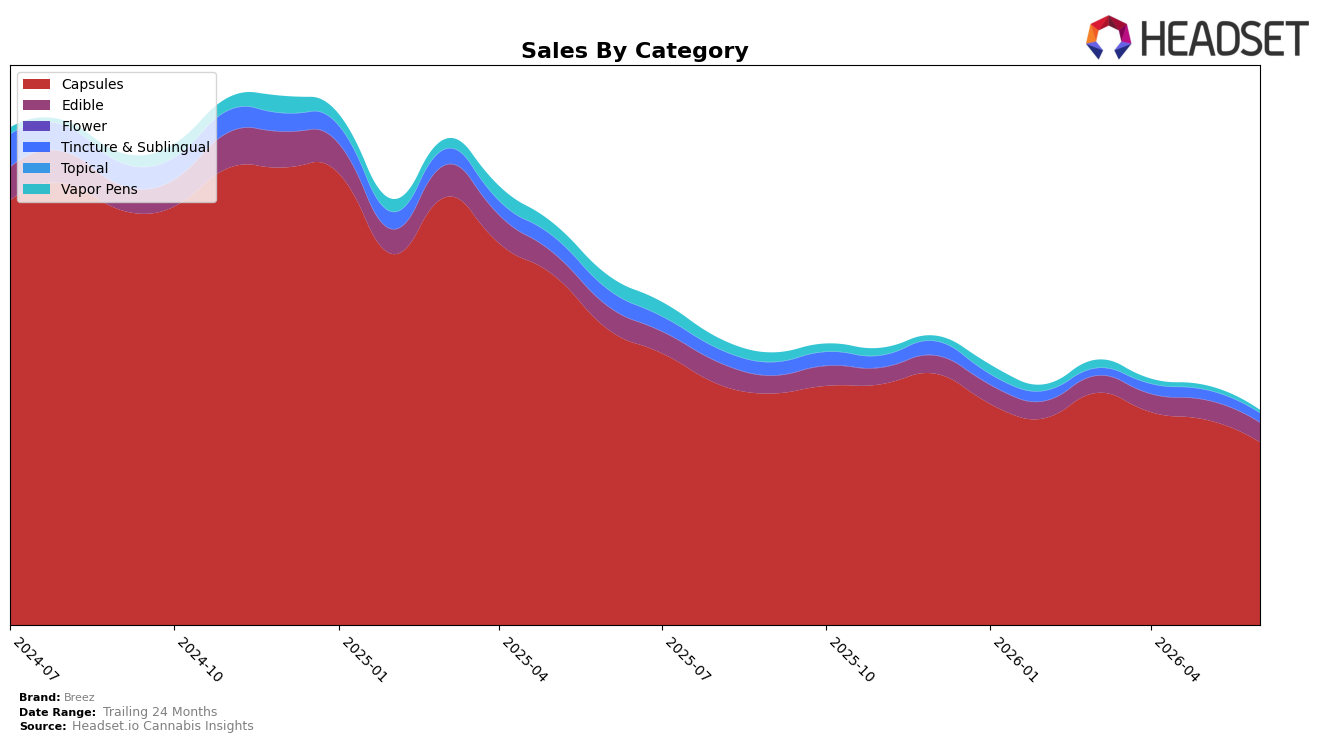

In June 2026, Breez concentrated 85.84% of sales in Capsules while Edible held 8.96% and Tincture & Sublingual 4.08%, with Vapor Pens at 1.11%; the brand’s overall sales were down 38.75% year over year while Capsules declined 38.16% YoY and 11.07% month over month. Edible contracted 15.39% YoY but only 0.23% MoM, whereas Tincture & Sublingual fell 45.80% YoY and 7.28% MoM, and Vapor Pens dropped 82.44% YoY and 38.72% MoM; average price rose 5.71% YoY to $38.71 while Capsules carried a higher $45.84 average. The pattern implies Breez is increasingly tethered to a shrinking Capsules base, with modest resilience in Edible mix share insufficient to offset accelerated monthly contraction in Capsules and Vapor Pens.

Holding rank 1 in Capsules in California provides near-term positioning leverage, but an 11.07% MoM decline in Capsules alongside a 38.72% MoM slide in Vapor Pens signals concentration risk if category headwinds persist; the 5.71% YoY price increase paired with a 38.75% YoY sales decline indicates price cannot counter volume erosion at current mix. With Edible down only 0.23% MoM versus larger monthly drops in Capsules and Tincture & Sublingual at 7.28% MoM, the mix shift opportunity sits in lower-priced formats, implying Breez’s positioning should pivot from premium Capsule dependence toward stabilizing Edible demand while defending Capsule leadership to reduce volatility.

Competitive Landscape

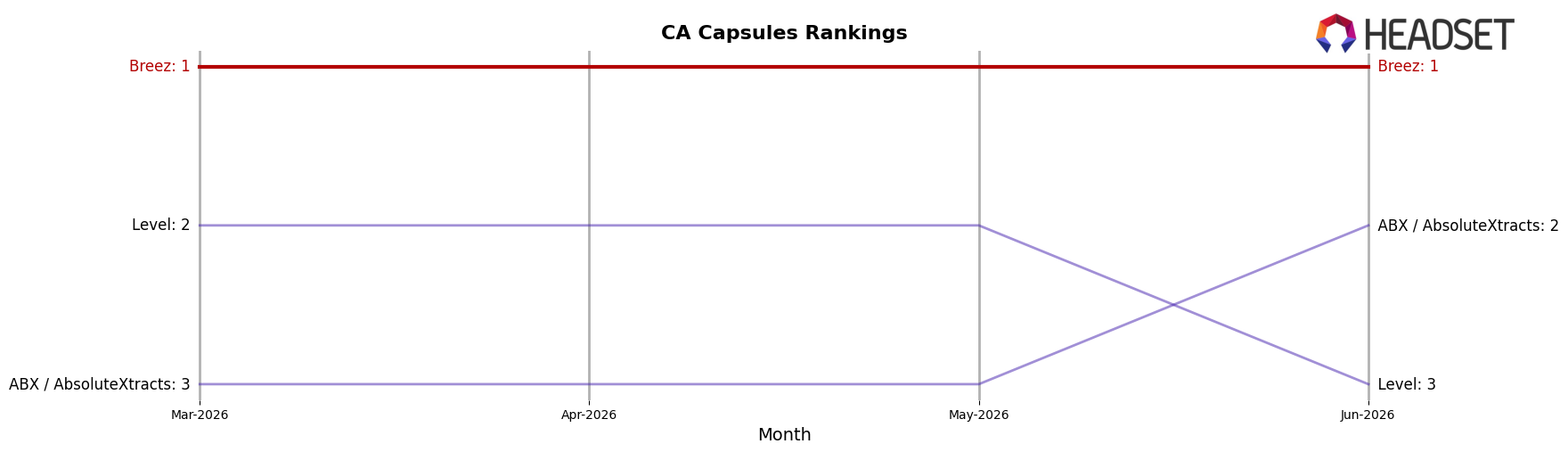

Breez is ranked #1 in California Capsules in June 2026, up 1 place year over year from #2, and it has held #1 for the past three months while also marking its peak in June 2026; meanwhile, ABX / AbsoluteXtracts sits at #2 after being #3 a year ago as its sales fell 23.27% year over year, and Level dropped from #1 to #3 alongside a 64.53% year-over-year sales decline. With Emerald Bay Extracts improving from #5 to #4 despite a 7.21% decline and Buddies moving from #6 to #5 with 29.83% sales growth, Breez’s climb to #1 and stability at the top indicate it is consolidating leadership as rivals either contract or grow from lower bases.

Notable Products

CBD/THC 1:1 Relief Cinnamon Mints 20-Pack (100mg CBD, 100mg THC) posted the steepest decline in June 2026 at -26.1% MoM while dropping to rank 6, contrasting with the Capsules leader Indica Extra Strength Tablet 50-Pack (1000mg) at rank 1 with a -6.1% MoM dip. Sativa Extra Strength Tablet 50-Pack (1000mg) slid -18.7% MoM at rank 2, whereas the CBD/THC/CBN 2:1:1 Nighttime Extra Strength Tablets 50-Pack (500mg CBD, 250mg THC, 250mg CBN) grew +18.7% MoM into rank 7, and four of the top ten are Capsules, indicating a continued mix-weight toward high-dosage formats. Edibles show mixed traction with Original Mint Tin 20-Pack (100mg) up +14.8% at rank 4 while Indica Royal Mint 10-Pack (100mg) edged +3.0% at rank 9, and the CBD Extra Strength Recovery Tablet 50-Pack (1000mg CBD) fell -12.7% at rank 8, implying selective demand for function-led SKUs over general wellness CBD. The pattern suggests Breez is leaning into potency and targeted use-cases within Capsules while Edibles serve as a secondary, more promotional lane, a direction that prioritizes retention via efficacy over breadth.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.