Jun-2026

Sales

Trend

6-Month

Product Count

SKUs

Avg Price

YoY Sales Change

YoY Price Change

Market Insights Snapshot

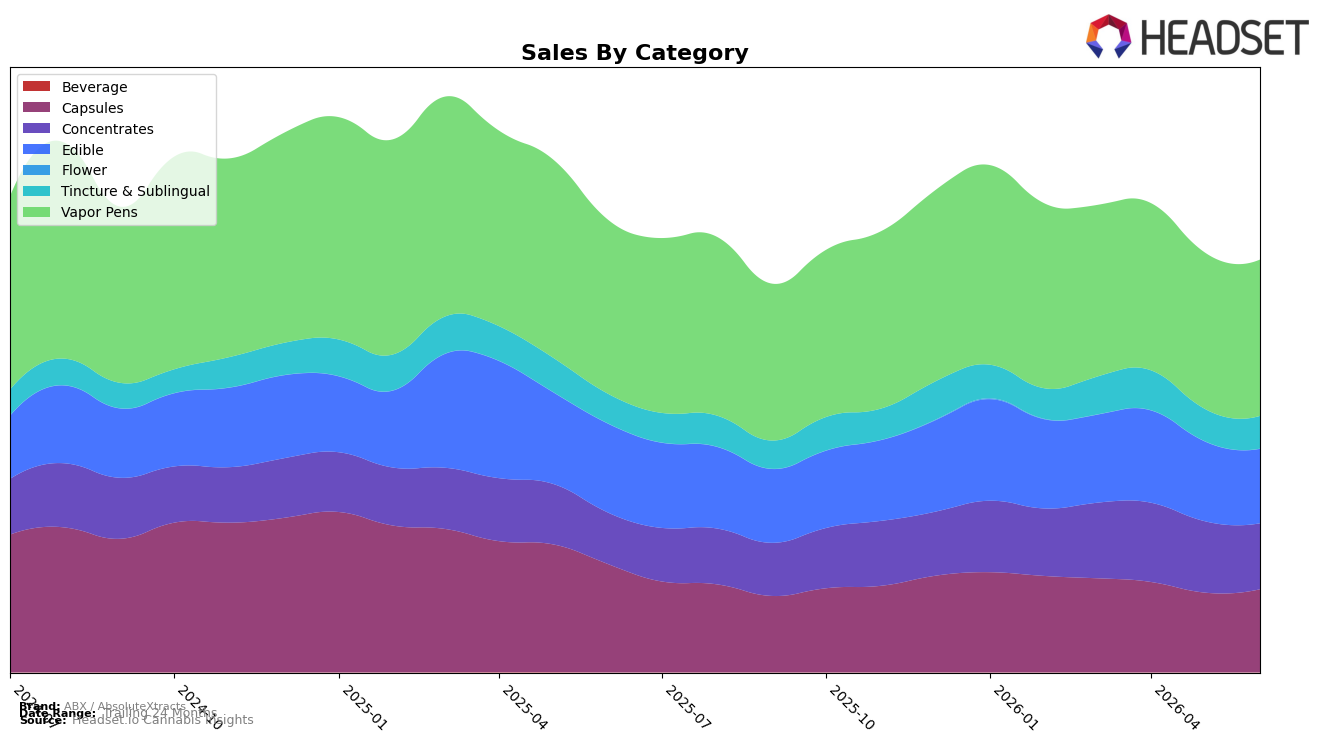

In June 2026, ABX / AbsoluteXtracts concentrated 37.94% of sales in Vapor Pens with year-over-year decline of 10.15% and a marginal month-over-month dip of 0.04%, while Capsules held 20.15% share with a 23.27% YoY drop but a 4.17% MoM rise. Edible accounted for 18.04% share with YoY down 16.25% and MoM down 6.71%, contrasted by Concentrates at 15.97% share growing 28.27% YoY despite a 7.68% MoM pullback; Tincture & Sublingual at 7.90% share increased 10.30% YoY and 1.08% MoM. With overall brand sales down 8.79% YoY and average price down 2.22%, the pattern implies mix is tilting away from large, declining Edible and Vapor Pens toward faster-growing but smaller pockets like Concentrates and Tincture & Sublingual, cushioning the YoY slide but not offsetting it month-over-month.

Positioning-wise, anchoring in Vapor Pens at rank 23 in California places the brand mid-pack while growth is concentrated in niches: a 28.27% YoY surge in Concentrates and a 10.30% YoY rise in Tincture & Sublingual coincide with MoM contractions of 7.68% and MoM gains of 1.08%, respectively. The 4.17% MoM uptick in Capsules against a 23.27% YoY decline, paired with Edible’s 6.71% MoM fall and 16.25% YoY drop, indicates a need to prioritize repeatable monthly traction over legacy scale categories; the implication is a repositioning toward efficacy-led formats (Concentrates, Tincture & Sublingual) to stabilize share while maintaining a presence in Vapor Pens where rank 23 suggests room to climb through price-pack and strain portfolio calibration.

Competitive Landscape

ABX / AbsoluteXtracts sits at rank #23 in CA Vapor Pens in June 2026 with no year-over-year rank change from #23, and no three-month movement from #23 either; against a field where STIIIZY held #1 both this year and last while its sales declined 6.95%, and Jetty Extracts climbed from #5 to #3 on 47.32% YoY sales growth, the brand’s flat position contrasts with peers’ upward and downward rank shifts, suggesting that stability at #23 alongside a historical peak at #18 in March 2025 implies a stalled trajectory that will likely require share-capturing moves to re-enter the top 20.

Notable Products

Sleepytime- THC/CBN 2:1 Elderberry Gummies 20-Pack (100mg THC, 50mg CBN) posted the steepest decline at -10.6% month over month while holding the number 1 rank, and Maui Wowie Terp Chews 20-Pack (100mg) also slipped -10.5% at rank 4. In contrast, Refresh - Blue Dream CO2 Cartridge (1g) rose 14.8% to rank 5 as CBN/THC 2:5 Blueberry Lavender Sleepy Time Gummies 20-Pack (40mg CBN, 100mg THC) gained 10.4% at rank 2. Four of the top ten are Edible SKUs clustered in sleep and terp-chew formats with mixed movements from -10.6% to +13.7%, while Vapor Pens show a split with +14.8% for Blue Dream and -1.3% for Granddaddy Purple High Potency CO2 Cartridge (1g). The pattern implies ABX / AbsoluteXtracts is leaning into higher-velocity Vapor Pens alongside a still-dominant but softening sleep-Edibles core, suggesting portfolio balance rather than single-category dependence.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.