Jul-2026

Sales

Trend

6-Month

Product Count

SKUs

Avg Price

YoY Sales Change

YoY Price Change

Where to Buy

Emerald Bay Extracts is stocked at 389 licensed dispensaries across California, with the deepest coverage in Los Angeles, Sacramento, San Diego, Santa Rosa, and Fresno. Search by ZIP code or city below to find the closest one, or filter by product type if you are after a specific format.

Market Insights Snapshot

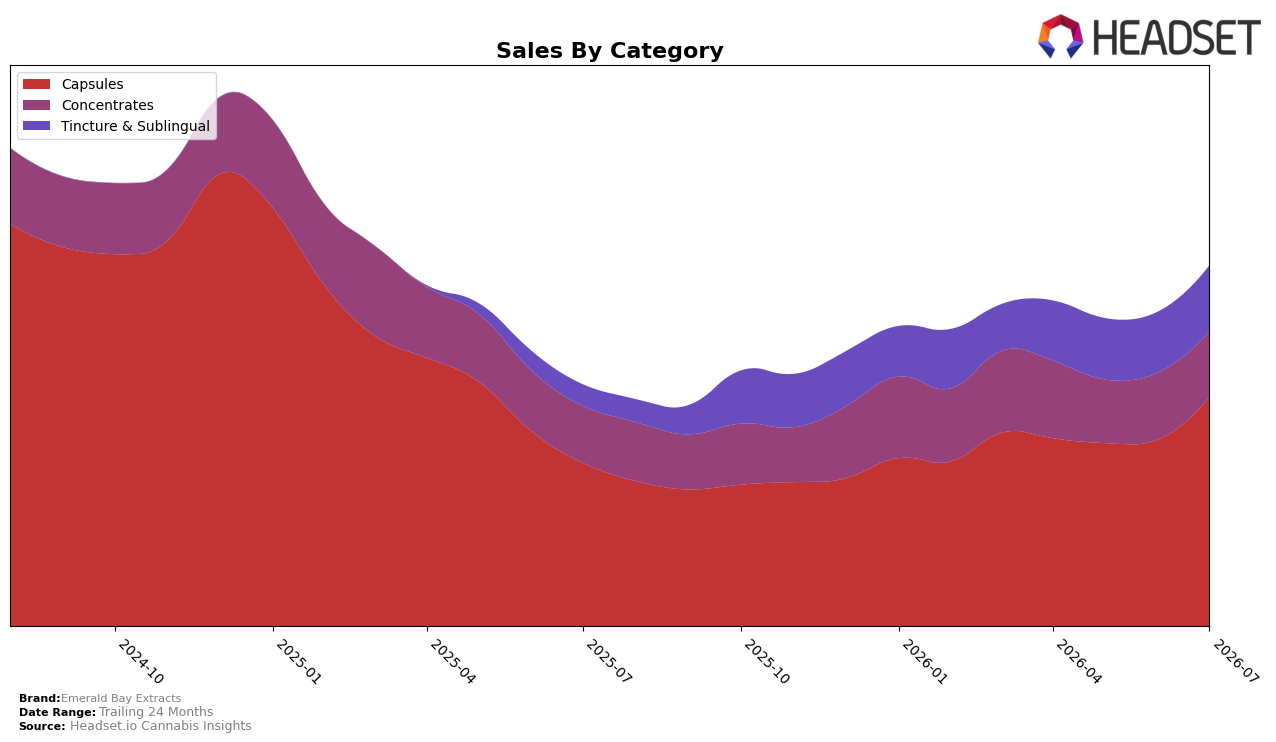

In July 2026, Emerald Bay Extracts concentrated 63.62% of sales in Capsules with 40.61% year-over-year growth and a 22.75% month-over-month lift, while Tincture & Sublingual rose to 18.26% share on a 209.88% year-over-year surge and an 8.34% month-over-month increase. Concentrates held 18.12% share but slipped month-over-month by 1.76% despite a 15.07% year-over-year gain, and the brand’s average price moved down 2.57% year-over-year to $33.20. With Capsules ranked 2 in California and share expanding sequentially, the pattern implies a tilt toward wellness-led formats where Capsules and Tincture & Sublingual are pulling mix upward while Concentrates plateau, setting the brand’s near-term volume engine in Capsules and its incremental growth optionality in Tincture & Sublingual.

The shift toward Capsules (+22.75% month-over-month) and Tincture & Sublingual (+8.34% month-over-month), alongside a modest price deflation of 2.57% year-over-year and a 49.51% year-over-year brand sales increase, implies Emerald Bay Extracts is trading for depth in routine-use segments rather than chasing volatility in Concentrates (−1.76% month-over-month). Holding the number 2 Capsules rank in California while Tincture & Sublingual posts a 209.88% year-over-year spike suggests positioning around format reliability and dosage clarity, with Capsules anchoring retention and Tincture & Sublingual widening the funnel; the implication is that protecting Capsules rank and selectively funding Tincture & Sublingual could compound share even if Concentrates maintain mid-teens year-over-year without monthly momentum.

Competitive Landscape

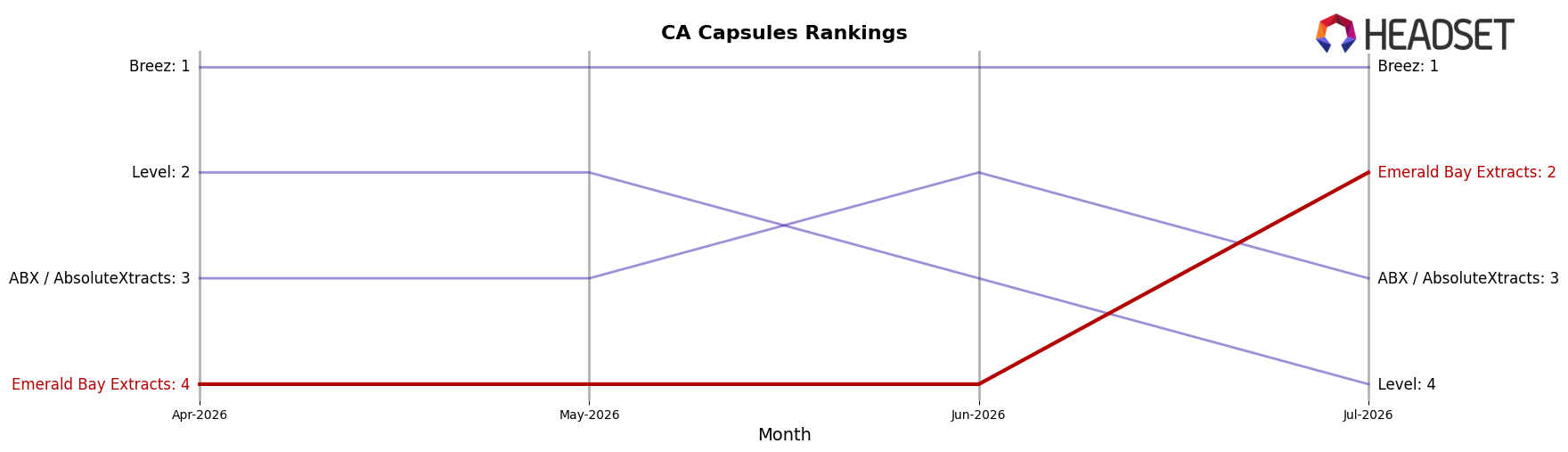

Emerald Bay Extracts sits at rank #2 in California Capsules in July 2026, up three spots from #5 year over year and two places from #4 in April 2026, indicating a steady climb as it hits its peak rank of #2 in July 2026. In directional contrast, Breez holds #1 but slipped from #2 a year ago while posting a -32.4% sales change, and ABX / AbsoluteXtracts sits at #3 with a flat rank versus last year and a -7.0% sales change; meanwhile, Level fell from #1 to #4 alongside a -60.2% sales change. This pattern implies Emerald Bay Extracts is consolidating share against leaders with declining momentum, positioning the brand to contest #1 if it maintains rank gains while rivals contract.

Notable Products

Ice Cream Cake RSO Syringe (1g) posted the steepest decline at -27.09% while falling to rank 4, contrasted by Ice Cream Cake RSO Tincture (1000mg THC, 20ml) jumping +43.12% into rank 8, indicating demand is shifting within format rather than flavor. Permanent Marker RSO Tablets 10-Pack (1000mg) held rank 1 with $58,108 despite no month-over-month figure, and Blue Dream RSO Syringe (1g) rose +16.81% at rank 2 as Blue Dream RSO Tablets 40-Pack (1000mg) slipped -6.84% at rank 3, showing inhalable RSO formats are gaining share at the expense of larger tablet packs. With six of the top ten positioned in Capsules and two in Concentrates, the mix implies Emerald Bay Extracts is tilting toward fast-acting formats inside a capsule-heavy portfolio, suggesting future growth will come from balancing format-led wins against erosion in legacy syringe SKUs.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.