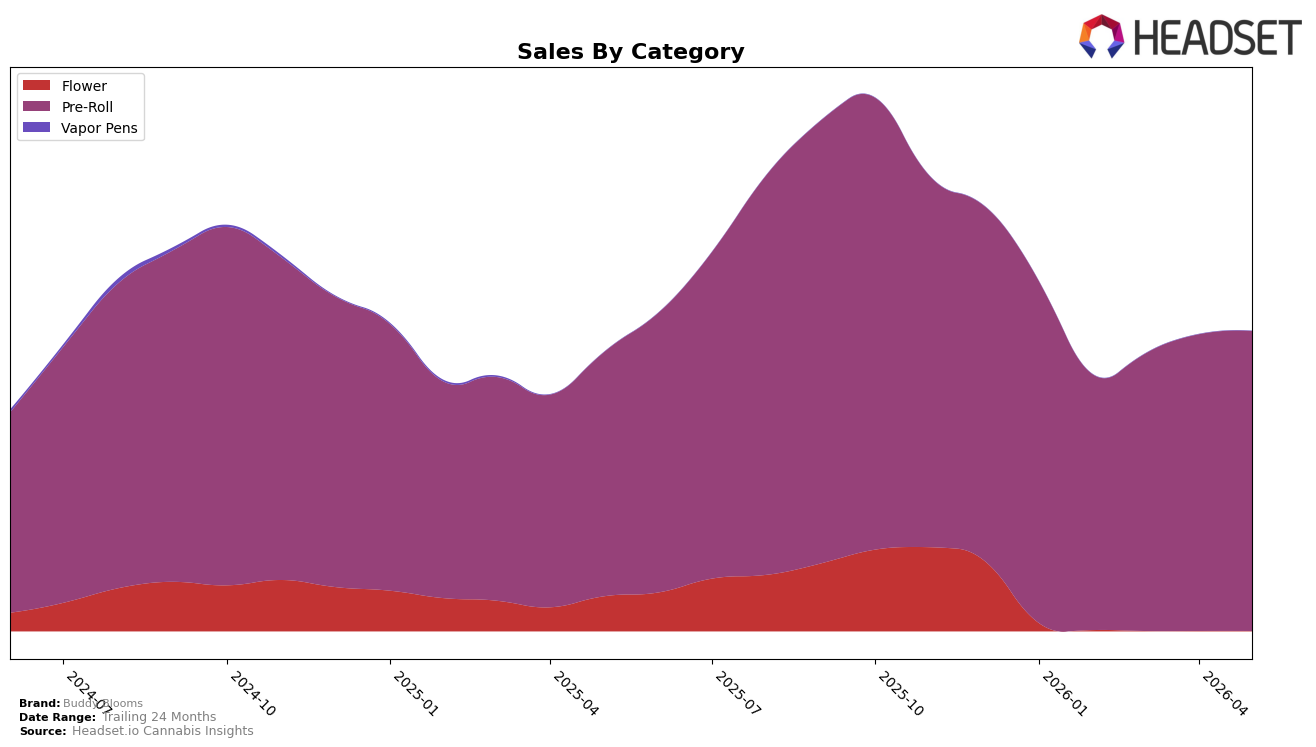

Market Insights Snapshot

Buddy Blooms concentrated entirely in Pre-Roll during May 2026, with category mix at 100.0% share and a rank of 25 in Ontario; within this single-category focus, Pre-Roll sales grew 23.05% year over year while month over month ticked up 1.08%. Brand-level sales rose 7.72% year over year alongside a 13.92% increase in average price to $15.05, indicating unit trends lag price expansion even as the Pre-Roll category outpaced the overall brand growth rate; the pattern implies reliance on pricing and mix concentration to offset softer unit momentum.

The one-category footprint amplifies exposure to Pre-Roll price elasticity, as the 13.92% average price lift outstrips the 1.08% month-over-month sales gain and coincides with a rank position of 25 that leaves limited buffer for volatility; with 34.72% sales growth over 24 months, the trajectory is durable but concentrated. The year-over-year Pre-Roll growth of 23.05% versus the brand’s 7.72% highlights that mix concentration is beneficial only while category momentum persists, so near-term positioning hinges on sustaining price at roughly $15.05 without eroding velocity and exploring incremental mix breadth if rank in Ontario stalls at 25.

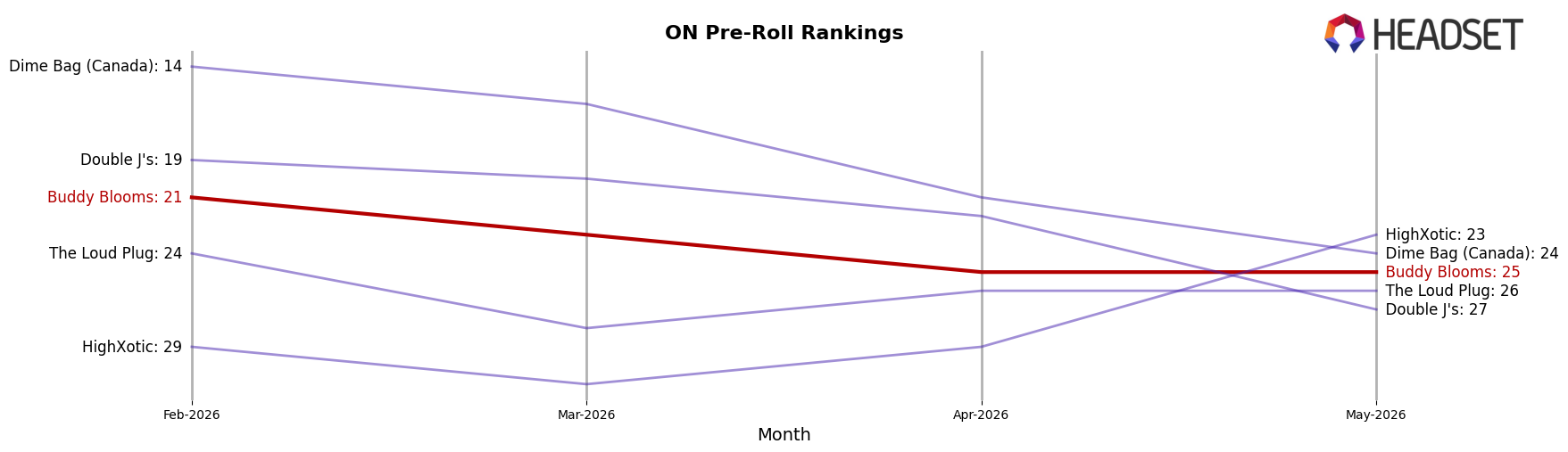

Competitive Landscape

Buddy Blooms sits at rank #25 in ON Pre-Roll for May 2026, improving 4 positions year over year from #29 while sliding 4 spots since February 2026 when it was #21; against this backdrop, Back Forty / Back 40 Cannabis climbed from #3 to #1 and expanded with a 66.8% YoY sales increase, whereas Jeeter slipped from #2 to #3 alongside a 48.4% YoY sales decline, indicating the competitive top tier is consolidating upward as Buddy Blooms stabilizes mid-pack. With a prior peak of #14 in September 2025 and a current position 11 ranks below that peak, the brand’s 4-rank YoY ascent contrasts with a 10-rank gap from its high-water mark, implying the trajectory points to recovery potential but requires regaining momentum relative to faster-rising leaders.

Notable Products

Biggest Buddy Sativa Pre-Roll 2-Pack (2g) fell 21.4% month over month and still held rank 1, while Big Buddy - Indica Pre-Roll 2-Pack (2g) declined 11.6% and sat at rank 4; the combination of a top-ranked drop and another double-digit decline implies reliance on value 2-packs is softening in May 2026. In contrast, Purple Haze Pre-Roll 10-Pack (5g) climbed 26.1% to rank 2 as Highbrid Pre-Roll 10-Pack (5g) rose 14.0% at rank 9, and four of the top ten are Pre-Roll 10-Packs, indicating multi-pack formats are absorbing demand that’s leaving the 2-pack tier. With Indica Pre-Roll (1g) down 22.3% at rank 8 while Lil Buddy - Sativa Pre-Roll (0.5g) grew 3.8% at rank 6, single sticks are bifurcating toward entry 0.5g rather than 1g, and the $257,023 taken by Purple Haze Pre-Roll 10-Pack (5g) reinforces where basket size is moving. Net pattern: mix is rotating toward 10-packs and select small-format entries, pointing Buddy Blooms toward bulk and value-led multipacks as the commercial direction.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.