Market Insights Snapshot

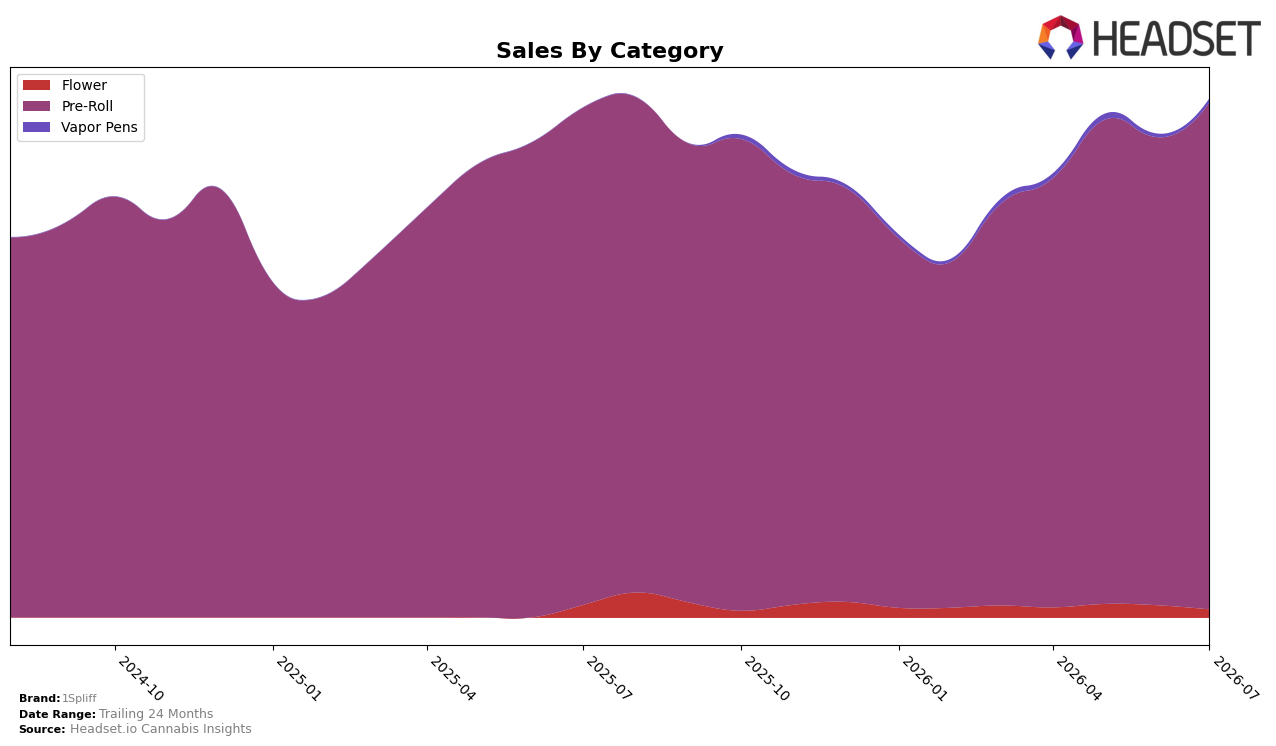

In July 2026, 1Spliff concentrated 97.71% of sales in Pre-Roll with a 1.92% year-over-year increase and an 8.30% month-over-month lift, while Flower contracted to a 1.55% share with a -35.54% year-over-year drop and a -33.75% month-over-month decline. Vapor Pens remained a small 0.74% share but expanded month-over-month by 22.29%, with no year-over-year baseline, and the overall average price rose 7.18% year-over-year to $22.39. With Pre-Roll ranked 15 in Ontario and holding a widening month-over-month gap versus Flower’s contraction, the pattern implies a deliberate consolidation around Pre-Roll that trades breadth for depth in a single-category footprint.

Because Pre-Roll’s 8.30% month-over-month growth coincides with a 7.18% year-over-year price increase, while Flower shrank -33.75% month-over-month and -35.54% year-over-year, 1Spliff’s pricing power and volume are increasingly tied to Pre-Roll rather than a diversified mix. The 22.29% month-over-month uptick in Vapor Pens at only 0.74% share provides optionality but not near-term scale, so maintaining rank 15 in Ontario likely depends on sustaining Pre-Roll velocity and mitigating the drag from Flower’s double-digit declines; the implication is a positioning bet on dominating a narrow lane rather than spreading across categories.

Competitive Landscape

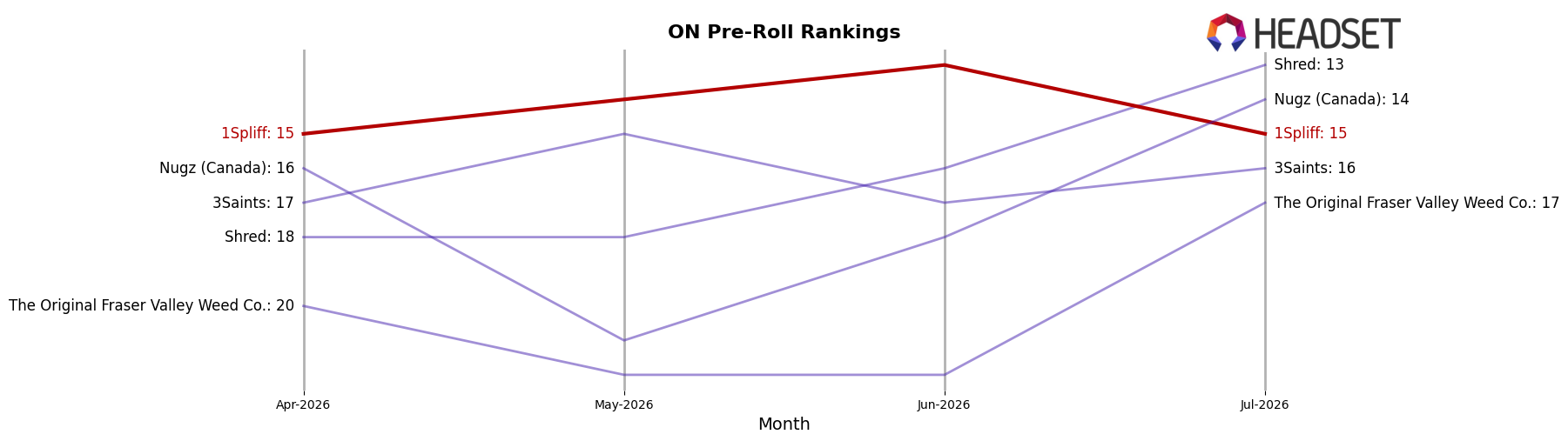

1Spliff sits at rank 15 in ON Pre-Roll in July 2026, unchanged year over year from rank 15, while its peak at rank 13 in June 2026 indicates a brief two-spot improvement before reverting. In contrast, Back Forty / Back 40 Cannabis advanced from rank 2 to rank 1 with 67.4% year-over-year sales growth, and General Admission slid from rank 1 to rank 2 alongside a 23.2% sales decline; meanwhile, Spinach climbed from rank 14 to rank 5 with 65.3% growth, outpacing 1Spliff’s flat rank trajectory over both three months and one year. The combination of a stable rank at 15 and competitors shifting by as many as nine positions implies that 1Spliff is holding share in a market with rapid up-and-down movements, but without a clear catalyst to climb, its mid-tier position risks being crowded by faster risers.

Notable Products

Hawaiian Snowcone Pre-Roll 10-Pack (3.5g) posted the steepest movement in July 2026 with a -17.5% month-over-month drop while holding rank 2, contrasting with Cannon Pre-Roll (1g) up 18.5% at rank 1. Across the top ten, nine of the SKUs are multi-pack or single-pack Pre-Rolls, indicating category concentration, with Hawaiian Snowcone Pre-Roll (1g) up 31.2% at rank 10 and Island Pink Pre-Roll 7-Pack (3.5g) up 7.9% at rank 6. The mix shows momentum shifting toward single units and value-positioned formats even as a high-volume multi-pack softened, implying 1Spliff is leaning into breadth within Pre-Rolls rather than rotating into new categories.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.