Market Insights Snapshot

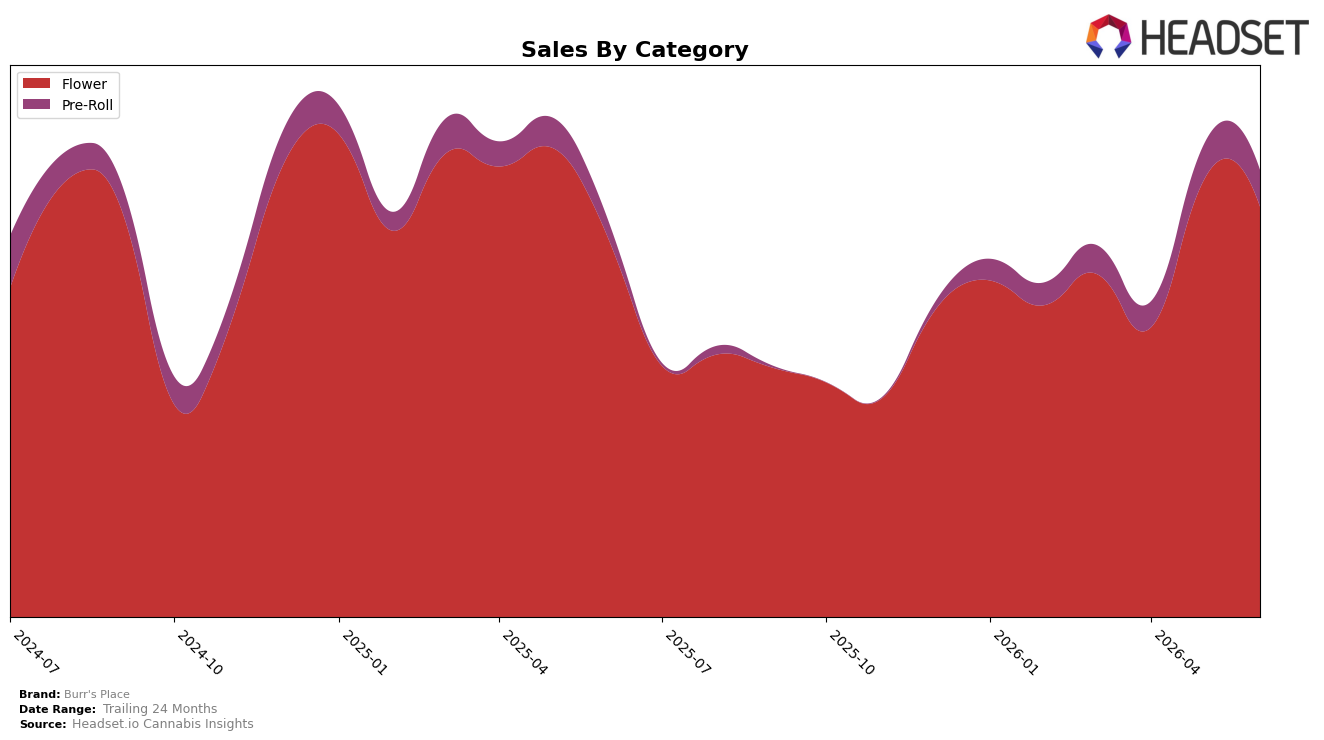

In June 2026, Burr's Place concentrated 91.55% of sales in Flower, down 6.37% month over month but up 8.36% year over year, while Pre-Roll held 8.45% share with 2.79% MoM growth and 98.67% YoY growth. Average price fell 38.67% YoY to $16.86 as overall brand sales rose 12.69% YoY, indicating volume expansion alongside price compression. Within Flower, a 6.37% MoM decline alongside Pre-Roll’s 2.79% MoM lift implies intra-portfolio substitution, and in California Flower the brand sits at rank 30, which frames the category-heavy mix against a mid-pack placement. The pattern implies Burr's Place is leaning on Flower for scale but relying on fast-growing Pre-Rolls to offset monthly volatility and support category diversification.

The shift toward a still-dominant but softening Flower base (91.55% share; rank 30 in California Flower) alongside a rapidly scaling Pre-Roll segment (+98.67% YoY; +2.79% MoM) implies a positioning pivot toward value-led trial and basket fill, aided by the 38.67% YoY average price decline. With total sales up 12.69% YoY despite a 6.37% MoM dip in Flower, mix resilience rests on Pre-Roll momentum and lower price points that likely expand unit velocity. The implication is that Burr's Place can protect relevance in crowded Flower while carving incremental occasions through Pre-Rolls, using price compression to capture share even as category rank pressure in California Flower caps immediate upside.

Competitive Landscape

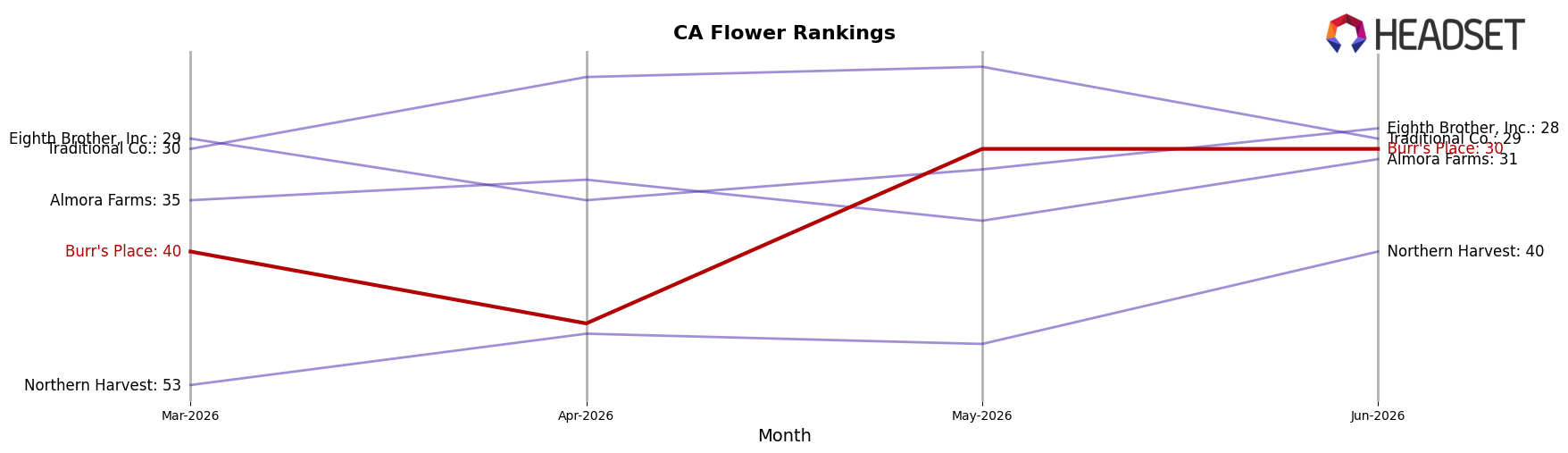

Burr's Place sits at rank #30 in CA Flower in June 2026 after improving 9 positions year over year from #39 to #30 and climbing 10 positions since March 2026 from #40 to #30, while also reaching a peak rank of #30 in June 2026; in contrast, STIIIZY edged up from #2 to #1 year over year and CAM advanced from #3 to #2 as CannaBiotix (CBX) slipped from #1 to #3, indicating that Burr's Place’s upward rank movement is occurring amid rapid consolidation at the top and implies its trajectory is one of late-cycle catch-up rather than head-to-head displacement of category leaders.

Notable Products

Macaroon (3.5g) delivered the headline move in June 2026 with a +66.4% month-over-month surge that vaulted it to rank 1, while Ze Chem (3.5g) fell -31.8% and slid to rank 3 from a higher prior position. Jelly Donutz #58 (3.5g) added breadth with a +51.1% gain at rank 2, and Orange Creampop (3.5g) contracted -21.2% at rank 10, concentrating wins at the very top while trimming the tail. With all top-10 SKUs in Flower and at least four of the top five Flower SKUs advancing by double digits, the mix points to Burr's Place leaning into premium Flower velocity rather than spreading attention across slower variants, supported by a single-month Flower leader booking $44,377.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.