Where to Buy

ButACake is stocked at 34 licensed dispensaries across New Jersey, with the deepest coverage in Newark, Atlantic City, Belleville, Bloomfield, and Bridgeton. Search by ZIP code or city below to find the closest one, or filter by product type if you are after a specific format.

Market Insights Snapshot

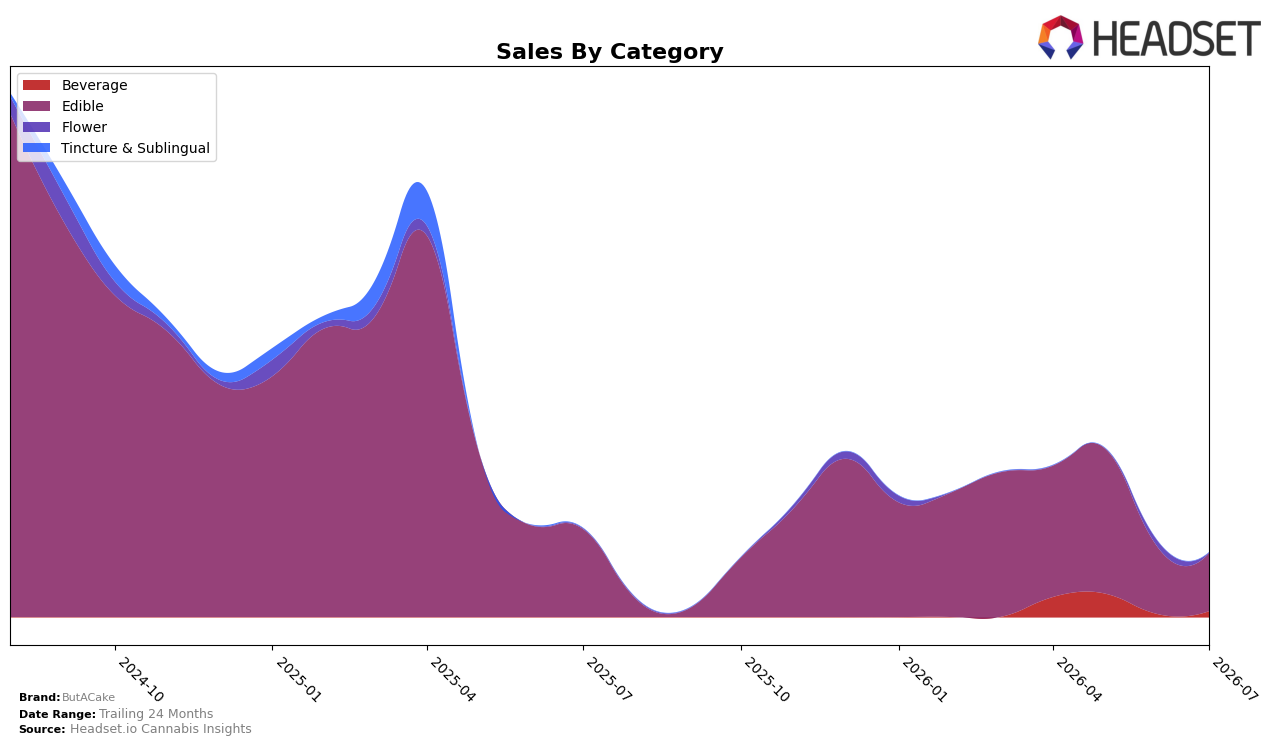

ButACake remained concentrated in Edible at 90.50% share in July 2026, with Edible sales down 34.23% year over year and 13.34% month over month, while Beverage climbed to 9.26% share on a 97.08% month-over-month surge and Flower slid to 0.24% share with a 97.35% month-over-month decline. Despite a 21.73% year-over-year drop in average price to $6.09, total brand sales fell 27.71% year over year as Edible weakness outweighed Beverage gains, and within New Jersey Edible the brand sat at rank 58, indicating that the mix shift is occurring from a low category rank position and implies the portfolio is relying on a shrinking Edible base while testing Beverage as a secondary volume lever.

The rapid month-over-month Beverage rise of 97.08% alongside a 13.34% Edible pullback and a 97.35% Flower retreat points to a tactical pivot toward higher-priced Beverage (average price $9.38 versus Edible at $5.88) to partially offset Edible contraction, yet the 27.71% overall sales decline and 21.73% price compression suggest discount-led defense in Edible is diluting value. With Edible holding 90.50% share and rank 58 in New Jersey, the pattern implies ButACake’s positioning is skewed toward lower-priced Edible volume where it lacks rank advantage, and it needs Beverage scale beyond 9.26% mix or a differentiated Edible price ladder to shift from share attrition to category-relevant placement.

Competitive Landscape

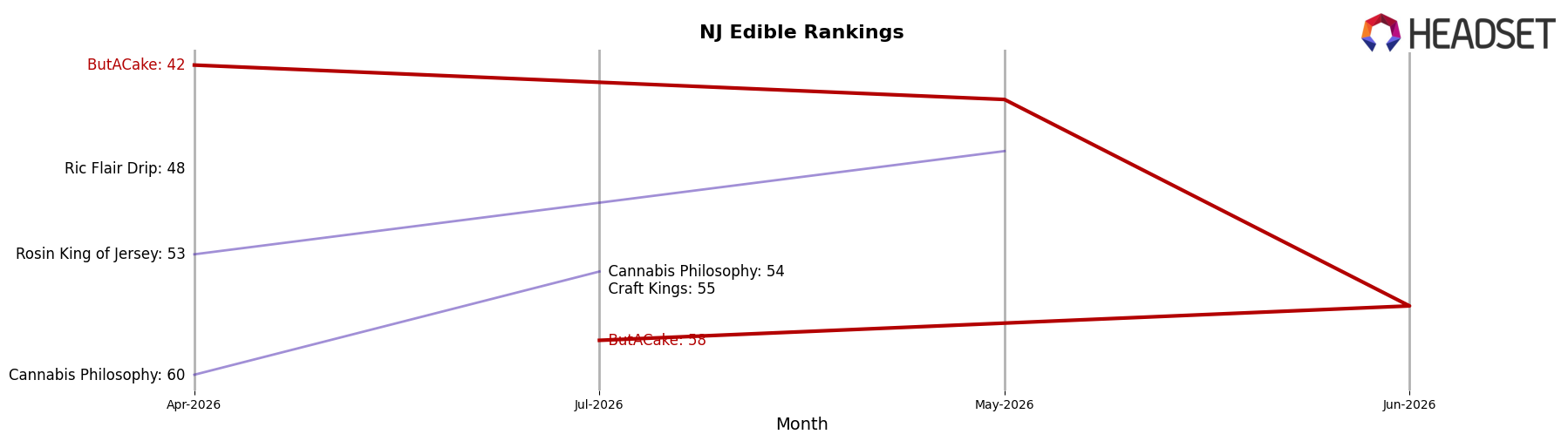

ButACake ranks #58 in NJ Edible in July 2026, down 15 positions year over year from #43, and 16 positions below its three-month mark of #42, while also sitting 37 spots beneath its peak of #21 from July 2024; by contrast, Gron / Grön holds #1 despite a 15.05% year-over-year sales decline and Wyld advanced to #2 from #3 with a 2.59% sales increase, indicating that ButACake’s rank erosion is more about relative share loss than category contraction and implies continued slippage unless the brand reclaims velocity against leaders gaining or retaining top-two positions.

Notable Products

Sugar Cookie (10mg) posted the standout move in July 2026 with a 140% month-over-month jump to rank 1, while Choco Chunk Cookie (10mg) rose 81% to rank 2, indicating a sharp split between winners and laggards at the top. In contrast, Snickerdoodle Cookie (10mg) fell 26% to rank 3 and PBNJ Brownie (10mg) dropped 49% to rank 7, and six of the top ten are Cookie SKUs, concentrating demand in a single family despite divergent trajectories. With Oatmeal Raisin Cookie (10mg) sliding 48% at rank 4 even as the lead cookie surges 140%, the mix implies ButACake is consolidating around a few hero cookie formats while pruning or repositioning underperforming variants.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.