Jul-2026

Sales

Trend

6-Month

Product Count

SKUs

Avg Price

YoY Sales Change

YoY Price Change

Where to Buy

The Growfather is stocked at 53 licensed dispensaries across New Jersey, with the deepest coverage in Jersey City, Ewing Township, Hackettstown, Mount Laurel, and Newark. Search by ZIP code or city below to find the closest one, or filter by product type if you are after a specific format.

Market Insights Snapshot

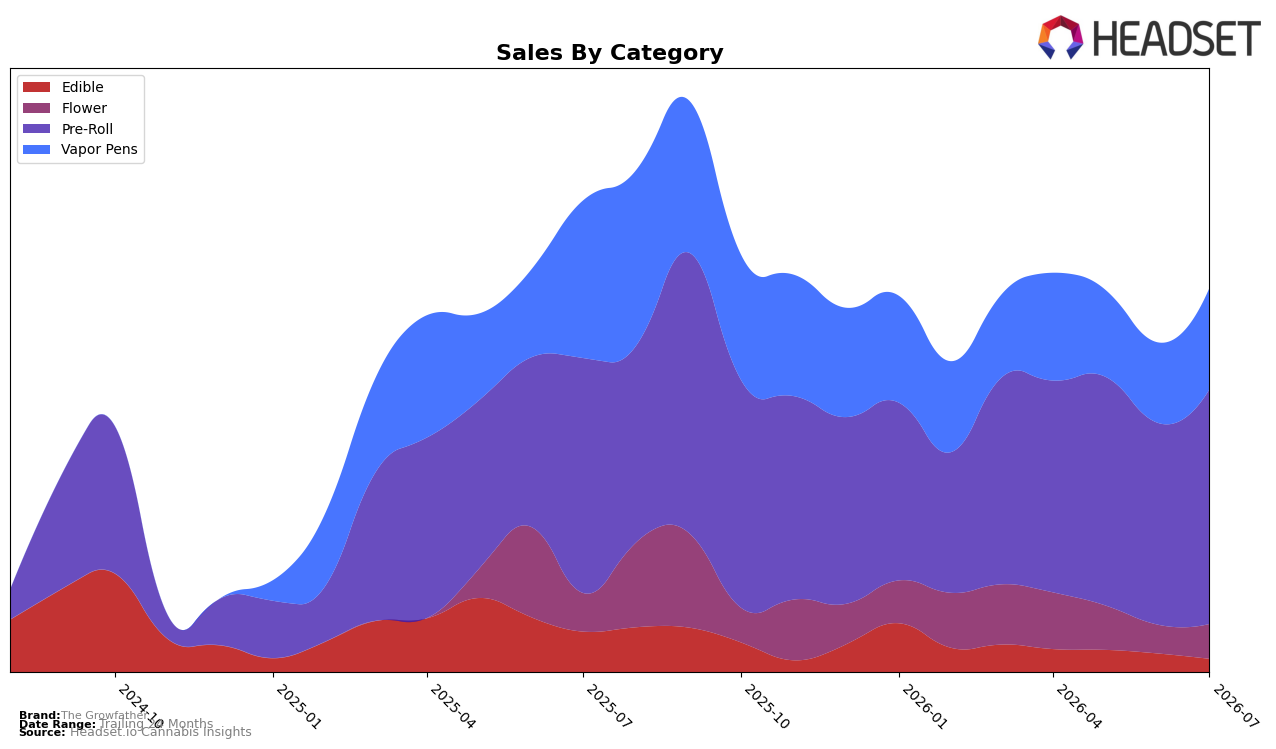

The Growfather concentrated 61.14% share in Pre-Roll with month-over-month growth of 16.28% but essentially flat year-over-year at -0.16%, while Vapor Pens held 26.40% share with a 26.04% MoM rise against a -35.73% YoY drop. Flower represented 9.02% share with 21.28% MoM growth and a -9.80% YoY change, and Edible slipped to 3.44% share with -28.87% MoM and -67.37% YoY. Despite an overall brand sales YoY decline of -18.60% and a -1.18% YoY average price movement to $30.74, the mix tilted toward inhalables that rebounded MoM, implying July 2026 was a volume-recovery month led by Pre-Roll and Vapor Pens while Edible contraction capped year-over-year momentum.

With Pre-Roll ranked 15th in New Jersey and accounting for 61.14% of sales, the brand’s positioning hinges on maintaining mid-pack visibility where a 16.28% MoM lift can move rank faster than a -0.16% YoY suggests. Vapor Pens’ -35.73% YoY against a 26.04% MoM rebound and Flower’s -9.80% YoY alongside 21.28% MoM indicate demand elasticity toward quick-turn inhalables at current price points, while Edible’s -28.87% MoM and -67.37% YoY signal deprioritization. Net effect: prioritize Pre-Roll depth to convert MoM gains into rank improvement around 15th, use Vapor Pens’ MoM momentum to recapture lost YoY share, and limit Edible exposure to avoid drag on overall growth trajectory.

Competitive Landscape

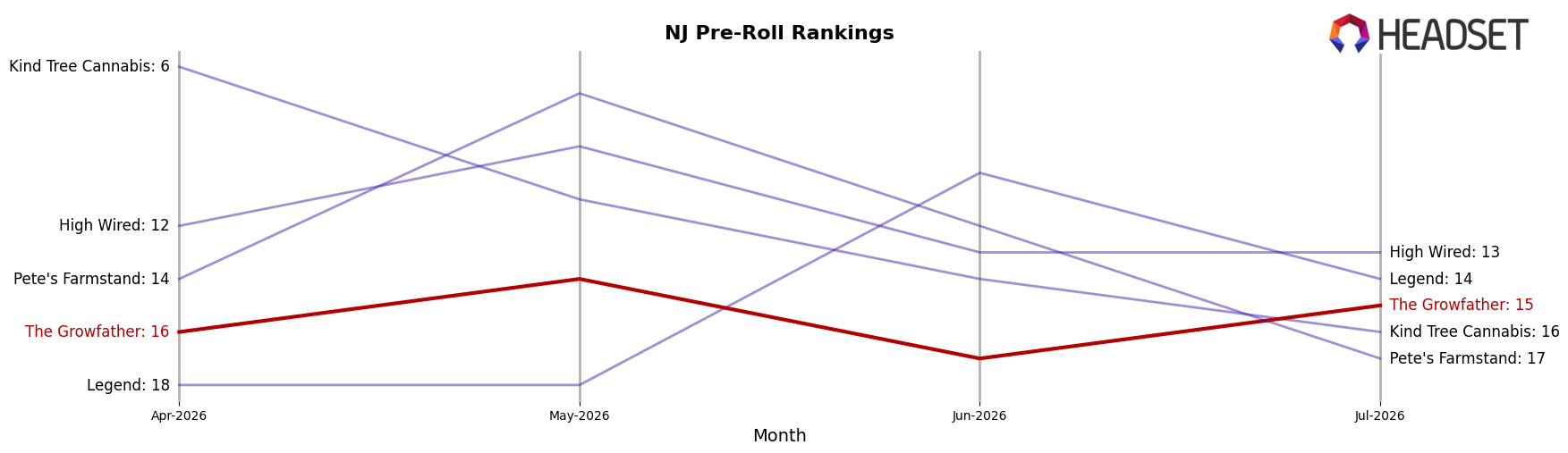

The Growfather sits at rank #15 in NJ Pre-Roll in July 2026, down 2 spots YoY from #13 and up 1 place from #16 three months ago, while its peak of #12 in September 2025 is 3 positions higher than today; meanwhile, RYTHM moved from #3 to #1 with 24.4% YoY sales growth and Ozone jumped from #8 to #2 on 119.1% YoY growth, indicating that The Growfather’s slight rank erosion is more about faster-rising leaders than a broad category slide. With Full Tilt Labs leaping from #22 to #4 on 264.3% YoY growth and Garden Greens dropping from #1 to #3 amid a 59.2% YoY decline, The Growfather’s movement from #13 to #15 suggests it is being outpaced by surging entrants rather than displaced by long-time incumbents, implying that without a step-change in velocity it risks drifting further from its September 2025 peak as challengers consolidate share at the top.

Notable Products

Sour Diesel Infused Pre-Roll (1.2g) set the pace in July 2026 with a 92.8% month-over-month surge and a climb to rank 1, while Pineapple Express Infused Pre-Roll (1.2g) followed with a 54.2% gain at rank 2, indicating a sharp tilt toward higher-octane SKUs at the very top. In contrast, Blue Dream Razz Pre-Roll (1.2g) fell 26.2% to rank 7 and Do Si Dos Infused Pre-Roll (1.2g) dipped 2.0% at rank 5, creating a widening performance gap inside the same format that concentrates demand at the extremes. With eight of the top ten sitting in Pre-Roll and White Widow Ground (3.5g) debuting at rank 9 without a reported month-over-month rate on $30,712 in sales, the mix suggests pre-rolls are anchoring velocity while Flower re-enters as a selective complement. The pattern implies The Growfather is consolidating around infused pre-roll energy while testing limited Flower presence to diversify without diluting its rank momentum.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.