May-2026

Sales

Trend

6-Month

Product Count

SKUs

Avg Price

YoY Sales Change

YoY Price Change

Market Insights Snapshot

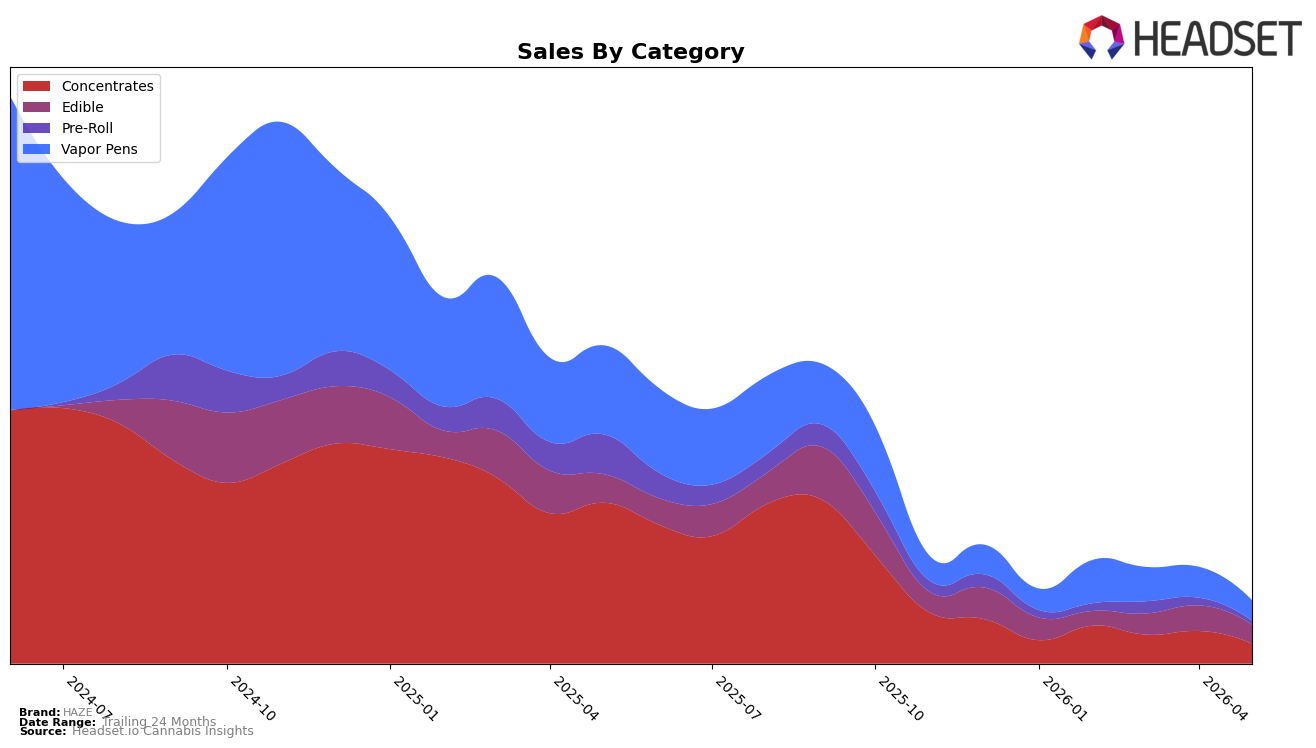

In May 2026, HAZE’s mix is concentrated in Vapor Pens at 32.54% share and Concentrates at 31.60% share, with Edible close behind at 29.72% and Pre-Roll at 6.14%. Vapor Pens declined 77.12% year over year and 33.80% month over month, while Concentrates fell 87.73% year over year and 39.11% month over month; this paired contraction shifts relative weight toward Edible despite Edible also dropping 34.67% year over year and 26.56% month over month. Pre-Roll contracted 90.30% year over year and 48.77% month over month, leaving it structurally minor within the portfolio. The pattern implies a defensive tilt toward lower-volatility Edible as higher-ticket inhalables retrench, with category balance now hinging on whether Vapor Pens at a 32.54% anchor can stabilize faster than Concentrates at 31.60%.

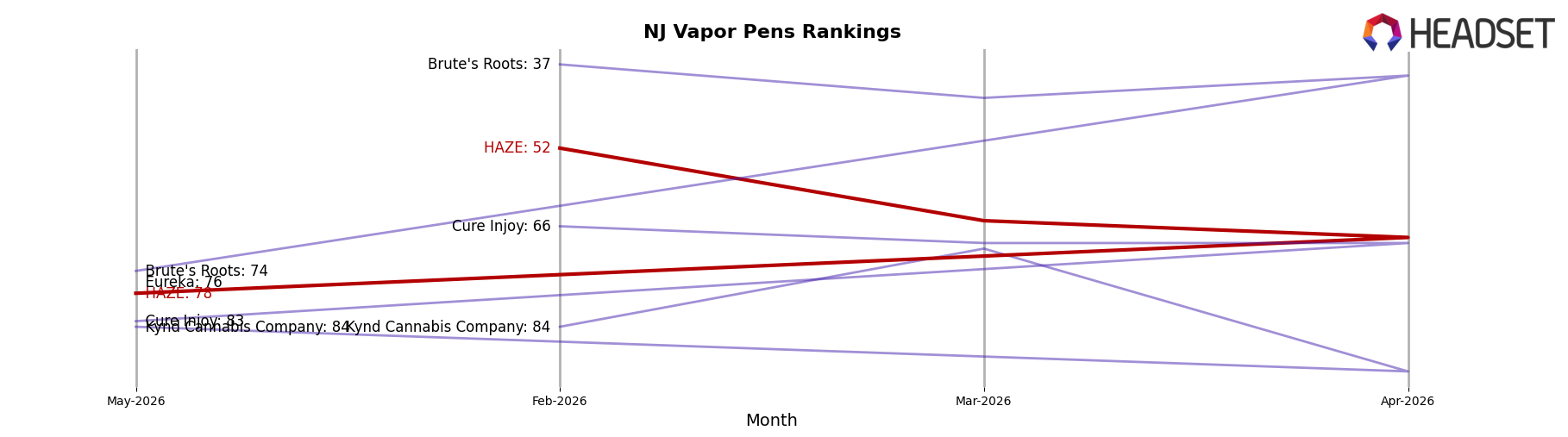

Average price mixed down 13.61% year over year to $22.79 amid category-level price points of $36.29 in Vapor Pens and $38.14 in Concentrates versus $12.57 in Edible, and the sharper month-over-month declines in Concentrates (down 39.11%) versus Vapor Pens (down 33.80%) suggest price-sensitive demand is reallocating into Edible. With rank 78 in Vapor Pens in New Jersey, recovery in the core inhalable slot likely requires either further price normalization or a pivot to the 29.72% Edible base where YoY decline at 34.67% is materially lighter than the 77.12% and 87.73% seen in the two largest inhalable segments. The implication is that near-term positioning favors margin-managed Edible to preserve share while Vapor Pens and Concentrates absorb the sharper volume and rank pressure.

Competitive Landscape

HAZE sits at rank #78 in New Jersey Vapor Pens in May 2026, down 39 positions year over year and 26 positions since February 2026, after previously peaking at #14 in June 2024. In contrast, Select held #1 while its sales fell 13.6% year over year, and Rove advanced from #16 to #5 with 159.0% year-over-year sales growth, indicating HAZE’s share is being reallocated toward faster-rising leaders. The gap between HAZE’s #52 rank in March 2026 and #78 in May 2026, alongside Legend moving from #5 to #3 with 63.7% growth and Simply Herb nudging from #6 to #4 with 2.7% growth, points to a trajectory of declining visibility where recovery would require reversing multi-month rank losses rather than counting on market softness at the top.

Notable Products

Haze X Mudd Brothers - Charlie's Girl #9 Live Resin Badder (1g) posted the steepest movement in May 2026 with a -63% month-over-month drop to rank 7, while Dragonfruit Diesel Live Resin Gummies 10-Pack (100mg) surged +105% to rank 1 and captured the brand’s momentum. Haze x Mudd Brothers - Raspberry Lime Live Rosin Gummies 10-Pack (100mg) rose +44% to rank 2 as Edibles occupied four of the top ten, whereas Sundae Sherbert Live Resin Sugar (1g) fell -23% to rank 5, signaling category divergence between Edibles and Concentrates. The scale of the +105% MoM gain at rank 1 alongside a -63% MoM decline in a top-10 Concentrate implies a pivot toward gummy-led velocity and away from extract-heavy bets, concentrating near-term commercial upside in Edibles.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.