Mar-2026

Sales

Trend

6-Month

Product Count

SKUs

Avg Price

YoY Sales Change

YoY Price Change

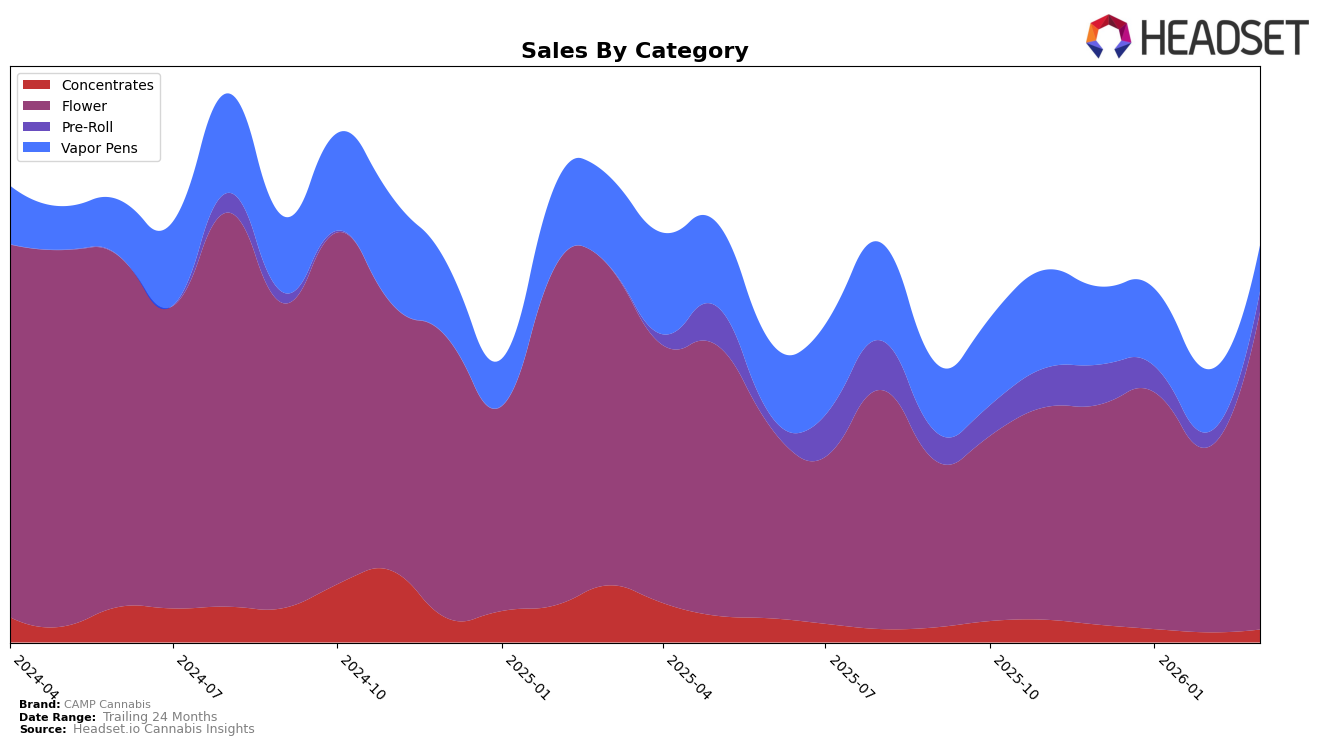

Market Insights Snapshot

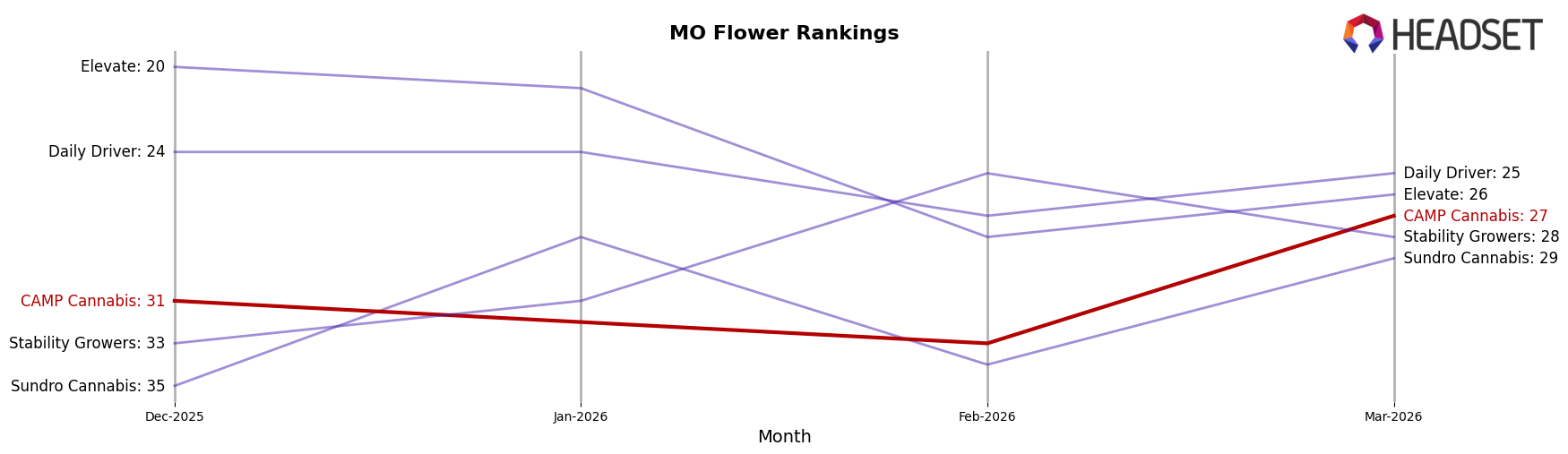

CAMP Cannabis has shown a mixed performance across different categories in Missouri. In the Flower category, the brand has made a notable improvement, climbing from a rank of 31 in December 2025 to 27 by March 2026. This upward movement is indicative of a strong presence and growing consumer preference in this segment, especially considering the substantial increase in sales from December to March. However, in the Concentrates category, CAMP Cannabis has struggled to maintain a top 30 position, with rankings hovering in the mid-30s, highlighting potential challenges in capturing market share here.

In other categories, such as Pre-Rolls and Vapor Pens, CAMP Cannabis has not managed to break into the top 30 rankings in Missouri. The Pre-Roll segment saw a decline to 60th position in February 2026, before slightly recovering to 52nd in March 2026, suggesting volatility and perhaps a need for strategic adjustments. Similarly, the Vapor Pens category has seen a drop in rank, moving from 41 in January to 49 by March, which could indicate increased competition or shifting consumer preferences. Overall, while CAMP Cannabis has shown strength in the Flower category, there are opportunities for growth and improvement in other segments.

Competitive Landscape

In the competitive landscape of the Flower category in Missouri, CAMP Cannabis has shown a notable improvement in rank from December 2025 to March 2026. Starting at rank 31 in December, CAMP Cannabis climbed to rank 27 by March, indicating a positive trend in market presence. This upward movement is particularly significant when compared to competitors like Daily Driver and Elevate, both of which experienced fluctuations and did not maintain a consistent presence in the top 20. While Stability Growers briefly surpassed CAMP Cannabis in February, they fell behind again by March. Meanwhile, Sundro Cannabis showed a similar upward trajectory but remained behind CAMP Cannabis in rank. This competitive positioning suggests that CAMP Cannabis is successfully capturing market share, potentially due to strategic marketing efforts or product offerings that resonate well with consumers in Missouri.

Notable Products

In March 2026, Papayaz Ice Cream Cake (3.5g) emerged as the top-performing product for CAMP Cannabis, climbing from a fifth-place rank in February to the first position with impressive sales of 2462 units. NF1 (3.5g) made a strong debut, securing the second spot, while Triangle Kush (Bulk) ranked third. Spec Ops (Bulk) followed closely in fourth place, marking its entry into the rankings this month. Melted Strawberries (3.5g) experienced a drop from second place in February to fifth in March. This shift in rankings highlights a dynamic month for CAMP Cannabis, with new products gaining traction and previously top-ranked items adjusting their positions.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.