Jul-2026

Sales

Trend

6-Month

Product Count

SKUs

Avg Price

YoY Sales Change

YoY Price Change

Where to Buy

The Standard is stocked at 262 licensed dispensaries across Missouri, Ohio, and 3 other states, 99 of them in Missouri, with the deepest coverage in St. Louis, KCMO, Columbia, Florissant, and Springfield. Search by ZIP code or city below to find the closest one, or filter by product type if you are after a specific format.

Market Insights Snapshot

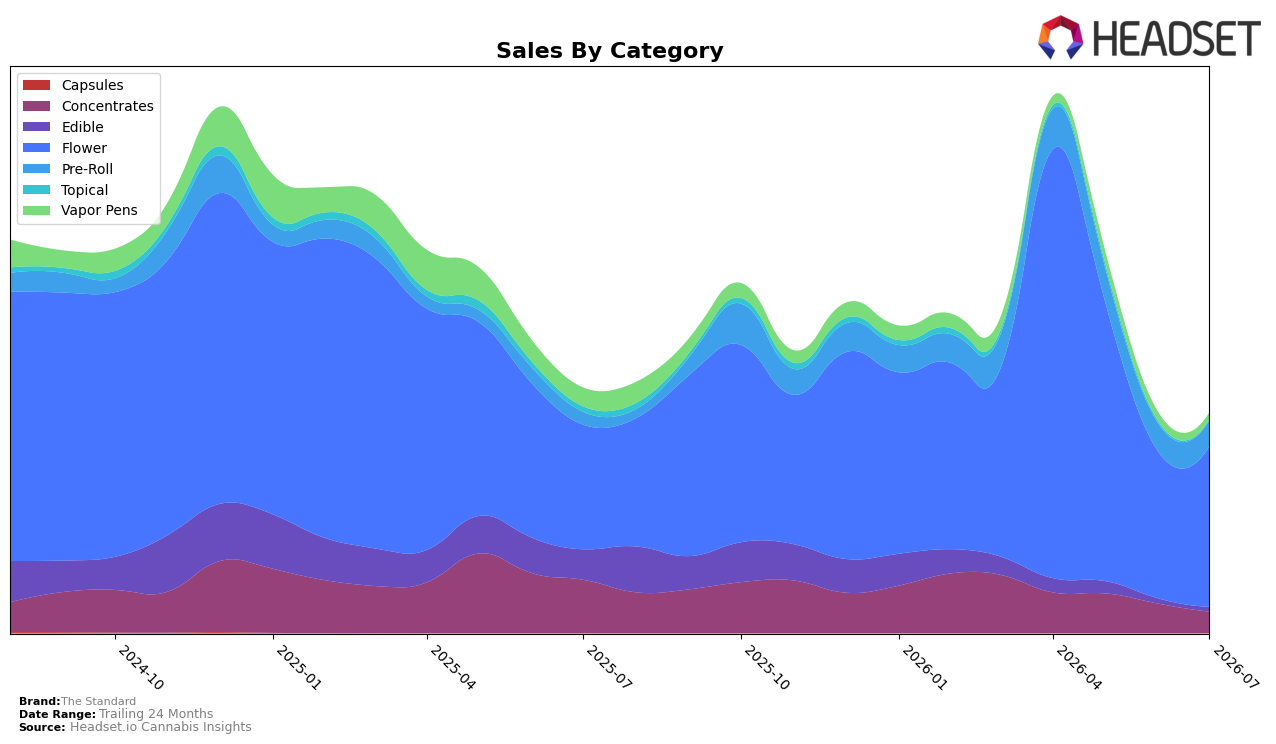

In July 2026, The Standard concentrated 73.44% of sales in Flower, up 9.24% month over month and 29.09% year over year, while Pre-Roll held 11.68% share with a 106.40% year-over-year surge but a 7.62% month-over-month dip. Conversely, Concentrates fell 27.85% month over month and 60.25% year over year to 9.63% share, and Vapor Pens declined 25.92% month over month and 64.81% year over year to 2.99% share; Edible was down 9.01% month over month and 85.34% year over year to 2.02% share, and Topical contracted 72.28% month over month and 89.56% year over year to 0.24% share. With brand sales down 10.23% year over year and average price down 12.69%, these shifts imply The Standard is consolidating around Flower and selective Pre-Roll while exiting or de-emphasizing low-velocity form factors, trading price for volume to defend share inside its core.

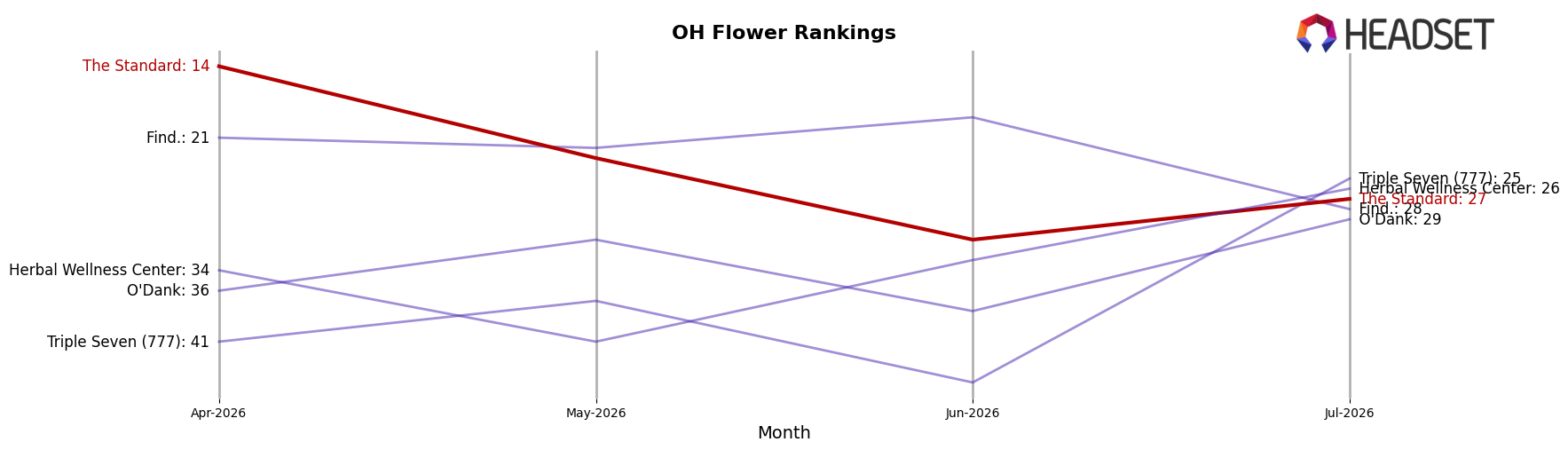

The pivot toward Flower and Pre-Roll repositions The Standard for basket-builder and value-driven missions: July 2026 Flower growth of 9.24% month over month alongside a 12.69% year-over-year price decline indicates elasticity capture, while the 106.40% year-over-year gain in Pre-Roll against a 7.62% month-over-month pullback suggests promotional or distribution spikes normalizing. Sharp contractions in Concentrates (-27.85% month over month) and Vapor Pens (-25.92% month over month) reweight the portfolio toward inhalables with simpler price cues, and the 27th rank in Flower in Ohio signals headroom if the mix-driven volume gains can offset margin compression; the pattern implies a scale-first posture prioritizing unit throughput in core inhalables over breadth.

Competitive Landscape

The Standard sits at rank #27 in July 2026, down 14 places from its April 2026 peak at #14 and six spots worse than its July 2025 position at #33, while the three-month slide from #14 in April 2026 to #27 in July 2026 marks a 13-place decline; in contrast, RYTHM climbed from #6 to #1 year over year with 74.99% sales growth and Klutch Cannabis surged from #21 to #3 with 403.04% sales growth. With Riviera Creek holding at #2 despite a -15.97% YoY sales decline and Buckeye Relief easing from #2 to #4 alongside -10.49% YoY sales, the competitive ladder is being reordered faster at the top than in the mid-pack; this rank trajectory implies The Standard is being out-accelerated by ascendant leaders and needs a catalyst to reverse a mid-year downdraft that has widened its gap from the top five.

Notable Products

Deleted Diesel Pre-Roll (1g) posted the steepest movement in July 2026 with a -74.4% month-over-month drop and slid to rank 9, while Dream Junky (3.5g) also contracted by -11.5% at rank 6, signaling pressure on both ends of the ranking. In contrast, Dawg Pound Kush Infused Pre-Roll (1g) climbed 46.7% month over month to hold rank 2 as Cherry Acai Distillate Infused Pre-Roll (1g) sat at rank 1, indicating mixed traction within Pre-Roll even as Flower logged a -38.4% decline for Caribbean Durbz (3.5g) at rank 5. With four of the top ten coming from Flower and three from Pre-Roll, the split suggests The Standard is leaning into Pre-Roll momentum while Flower volatility forces tighter SKU selection and pricing discipline.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.