Jul-2026

Sales

Trend

6-Month

Product Count

SKUs

Avg Price

YoY Sales Change

YoY Price Change

Where to Buy

Cannavative is stocked at 49 licensed dispensaries across Nevada, with the deepest coverage in Las Vegas, North Las Vegas, Reno, Henderson, and Ely. Search by ZIP code or city below to find the closest one, or filter by product type if you are after a specific format.

Market Insights Snapshot

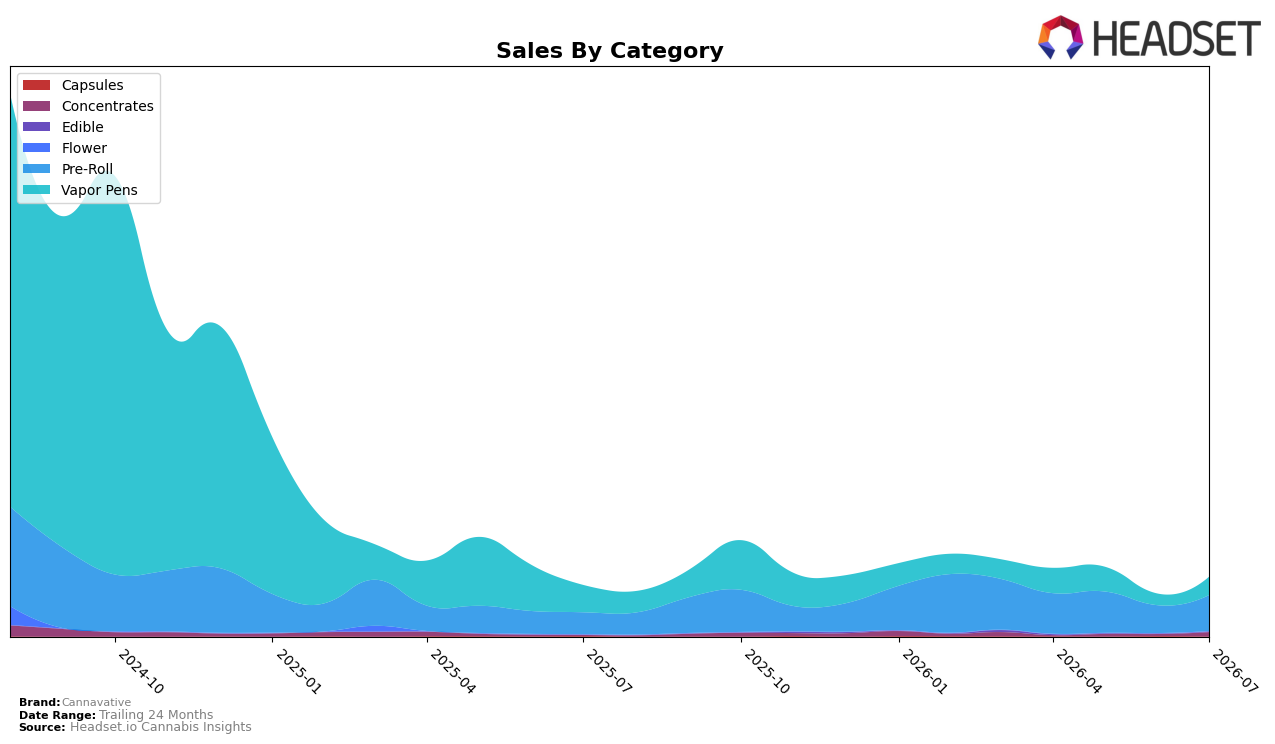

Cannavative’s category mix in July 2026 concentrated 61.19% of sales in Pre-Roll with year-over-year growth of 65.50% and month-over-month growth of 29.53%, while Vapor Pens held 30.98% share with a year-over-year decline of 33.52% but a month-over-month jump of 59.49%. Concentrates expanded to 7.17% share with a 371.81% year-over-year increase and a 127.26% month-over-month lift, whereas Capsules fell to 0.15% share with year-over-year and month-over-month declines of 82.55% and 83.09%, respectively. Average price fell 16.86% year over year to $16.66 as Pre-Roll averaged $14.00 and Vapor Pens $27.51, and the small Edible segment doubled month over month by 98.02% to 0.50% share. The pattern indicates a pivot toward lower-priced inhalables anchored by Pre-Roll and a revived Concentrates line, using price compression and mix shift to offset weakness in Vapor Pens while expanding unit throughput.

With a Pre-Roll rank of 26 in Nevada and Pre-Roll share at 61.19% alongside a 65.50% year-over-year increase, Cannavative is competing as a value-leaning inhalables player rather than a premium cart-led brand as Vapor Pens contracted 33.52% year over year despite a 59.49% month-over-month rebound. The 371.81% year-over-year surge and 127.26% month-over-month gain in Concentrates at a $15.44 average price, paired with a 16.86% brand-wide price decline, point to a strategy prioritizing accessible price points and cross-category trial, while Capsules’ 82.55% year-over-year drop and Edible’s 98.02% month-over-month uptick suggest pruning of low-velocity formats in favor of fast-moving inhalables. This configuration implies Cannavative’s near-term positioning hinges on scaling Pre-Roll penetration in Nevada while using Concentrates growth to diversify basket contribution and reduce dependence on volatile Vapor Pens.

Competitive Landscape

Cannavative sits at rank 26 in July 2026, improving 20 positions from rank 46 year over year, yet slipping 2 spots from April 2026 when it was rank 24, and remaining 12 places below its peak rank 14 in August 2024; meanwhile, Rove advanced from rank 4 to rank 1 with 92.2% year-over-year sales growth while STIIIZY moved from rank 1 to rank 2 alongside a 37.5% sales decline, indicating Cannavative’s upward YoY trajectory coexists with top-tier consolidation and that sustaining gains will require outpacing leaders that are either accelerating or ceding share.

Notable Products

Motivator - Jack and Cake Infused Pre-Roll (1g) posted the largest month-over-month surge at 118.4% to reach rank 2, while Motivator - Pineapple Icee Infused Pre-Roll (1g) climbed 86.9% to rank 1, indicating a sharp shift toward higher-velocity infused SKUs. In contrast, Motivator - Tamarindo Infused Pre-Roll (1g) fell 48.1% to rank 6, a break from the upward pattern that concentrates gains in only a subset of flavors. With four Motivator-branded infused pre-rolls sitting in the top seven and pre-rolls occupying nine of the top ten spots, July 2026 product demand is consolidating around infused pre-rolls, implying Cannavative’s near-term growth will hinge on a narrower set of hero SKUs rather than broad-line expansion.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.