Jul-2026

Sales

Trend

6-Month

Product Count

SKUs

Avg Price

YoY Sales Change

YoY Price Change

Where to Buy

Beboe is stocked at 315 licensed dispensaries across Maryland, Illinois, and 9 other states, 67 of them in Maryland, with the deepest coverage in Baltimore, Rockville, Hagerstown, Silver Spring, and Annapolis. Search by ZIP code or city below to find the closest one, or filter by product type if you are after a specific format.

Market Insights Snapshot

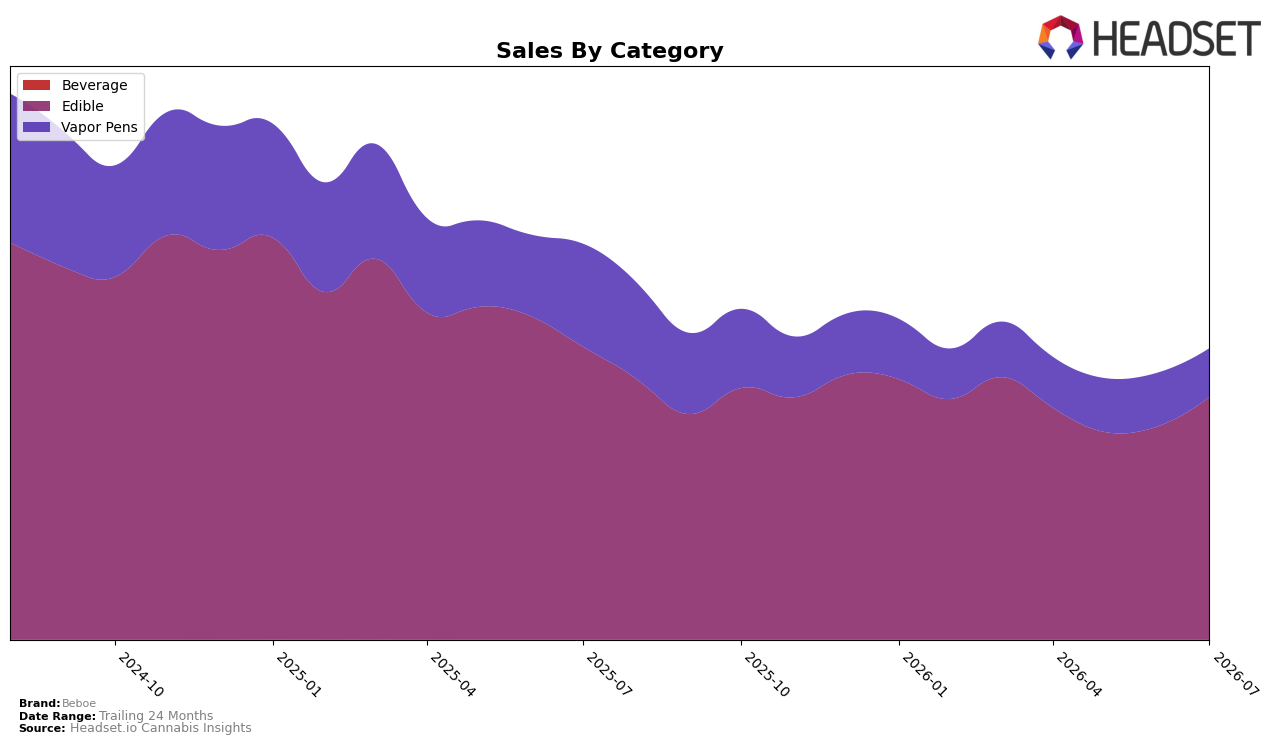

In July 2026, Beboe concentrated 83.43% of sales in Edible with a month-over-month increase of 13.88% but a year-over-year decline of 17.07%, while Vapor Pens held 16.57% share with a 9.72% month-over-month decline and a 53.03% year-over-year contraction. Average price moved down 16.92% year over year to $18.45, with Edible priced at 16.80 and Vapor Pens at 36.51, and Beboe ranked 13 in Edible in Maryland. The pattern implies Beboe’s near-term volume is being propped up by Edible’s month-over-month rebound and lower prices, while the deep Vapor Pens retrenchment is structurally shrinking the multi-category footprint.

With a 26.41% year-over-year brand sales decline alongside a 34.68% two-year slide, the mix shift toward Edible (up 13.88% month over month but still down 17.07% year over year) indicates reliance on a single category to stabilize traffic at lower price points. Holding rank 13 in Edible in Maryland while Vapor Pens fall 53.03% year over year suggests Beboe’s positioning is consolidating around edible occasions rather than inhalable use, implying assortment and pricing should prioritize depth in Edible over breadth in Vapor Pens to maintain share and mitigate further brand-level decline.

Competitive Landscape

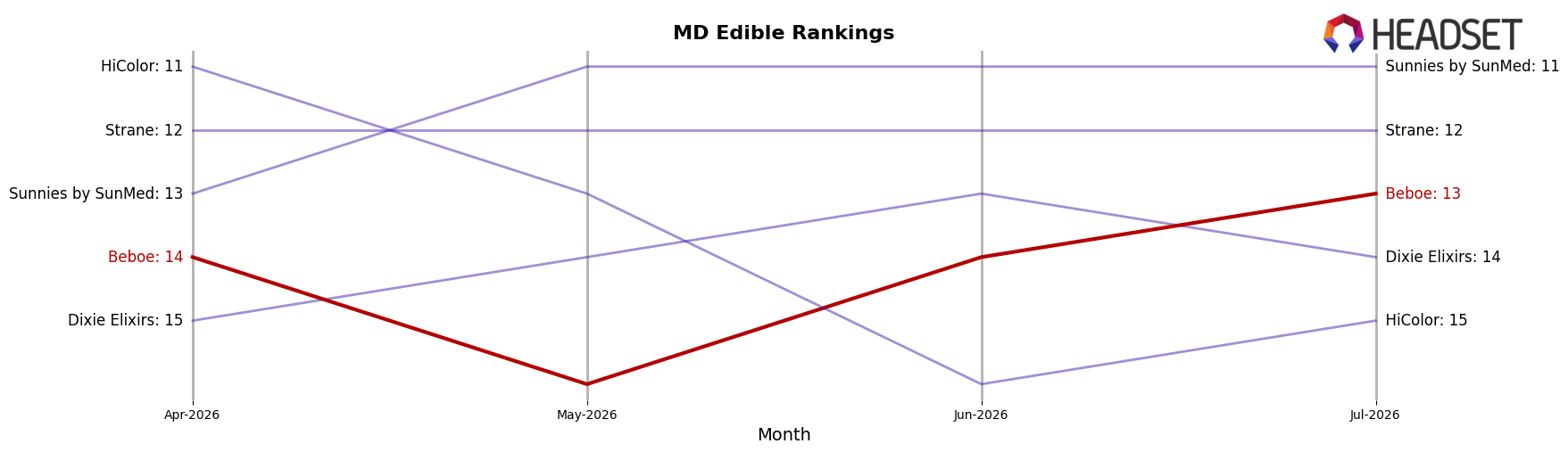

Beboe is ranked #13 in MD Edible in July 2026, unchanged YoY from #13, while improving 1 position from April 2026 when it sat at #14; the brand’s best historical mark was #9 in September 2024, a 4-rank gap from today. In contrast, Incredibles moved from #3 YoY to #1 with a 26.0% sales increase, and Wyld slipped from #1 YoY to #4 with an 18.0% sales decline, indicating Beboe’s flat rank comes amid active reshuffling at the top. The pattern implies Beboe’s steady #13 against both upward moves (e.g., Incredibles to #1) and downward moves (e.g., Wyld to #4) signals a holding pattern that will likely require share capture from mid-tier rivals to reapproach its #9 peak.

Notable Products

Anytime Huckleberry Gummies 20-Pack (100mg) delivered the headline move with a 258% month-over-month surge to rank 1, vaulting past a 20% decline for THC/CBG 1:1 Sparkling Pear Cloud 9 Gummies 20-Pack (100mg THC, 100mg CBG) now at rank 3. Inspired Blood Orange Gummies 20-Pack (100mg) climbed 47% to rank 5 while CBD/THC 1:1 Downtime Blueberry + Blueberry Pastilles 20-Pack (100mg CBD, 100mg THC) slipped 11% to rank 10, and nine of the top ten are Edibles, concentrating the mix in one category. The product slate is tilting toward fast-moving fruit-flavor Edibles with functional ratios receding, implying Beboe is consolidating around a single category where breakout SKUs can rapidly capture top ranks.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.