Where to Buy

Cannavore is stocked at 20 licensed dispensaries across Nevada and Washington, 17 of them in Nevada, with the deepest coverage in Las Vegas, Reno, Fallon, Henderson, and Spanish Springs. Search by ZIP code or city below to find the closest one, or filter by product type if you are after a specific format.

Market Insights Snapshot

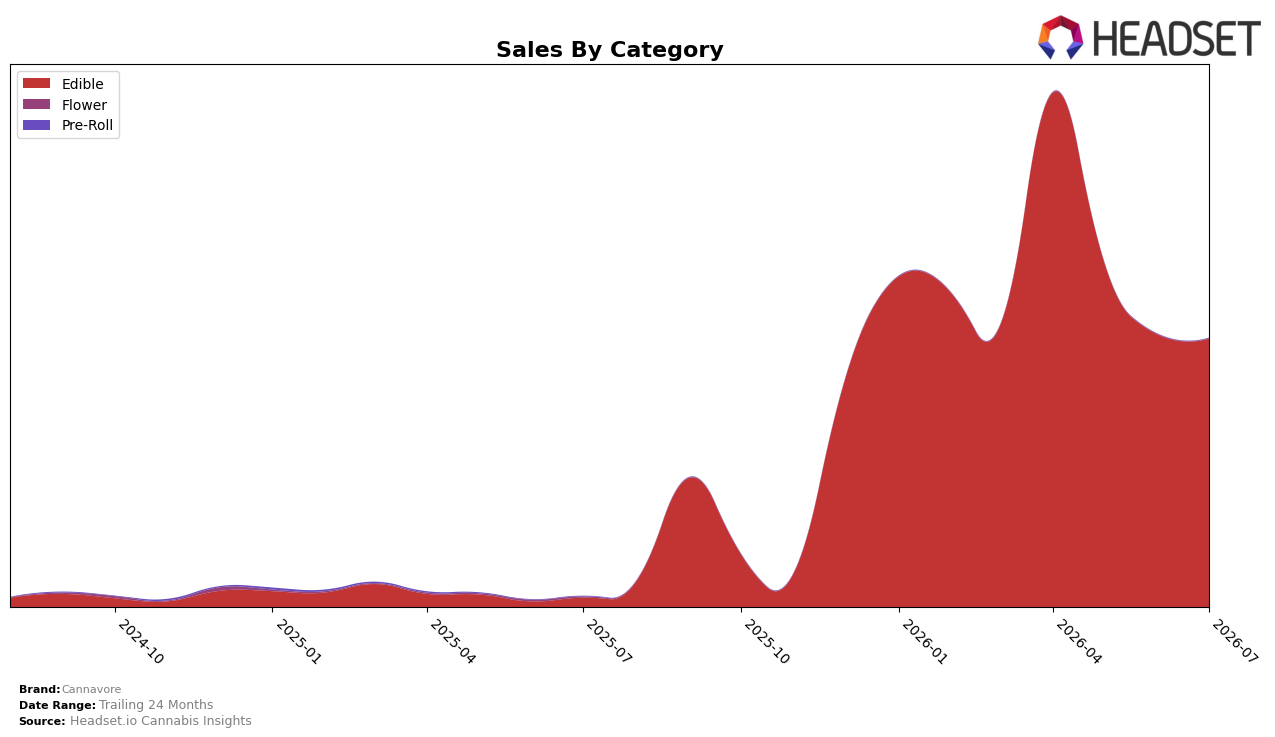

In July 2026, Cannavore operated as a single-category brand with Edible accounting for 100.0% of sales, while the Edible segment logged a year-over-year change of 2915.4% and a month-over-month change of -1.5%. Average price moved up 38.2% year over year to $17.96, alongside a brand-level year-over-year sales increase of 2603.2%, indicating that mix and pricing both expanded; the negative -1.5% MoM on Edible against a 100.0% share points to volume cooling within a concentrated portfolio. The pattern implies that Cannavore’s July 2026 momentum came from a pure-play Edible strategy that scaled rapidly year over year but encountered short-term demand friction month over month as higher prices met a fully concentrated mix.

Positioning-wise, Cannavore’s 100.0% reliance on Edibles, combined with a 38.2% YoY price lift and a rank of 9 in Edibles in Nevada, signals a premium-leaning stance that trades incremental share breadth for depth in one aisle. The 2915.4% YoY surge versus a -1.5% MoM dip suggests that the brand’s July 2026 share gains were driven by distribution and velocity expansion earlier in the year, while current elasticity is starting to surface at the shelf; this implies headroom to protect the number 9 slot through targeted price-pack architecture rather than category diversification in the near term.

Competitive Landscape

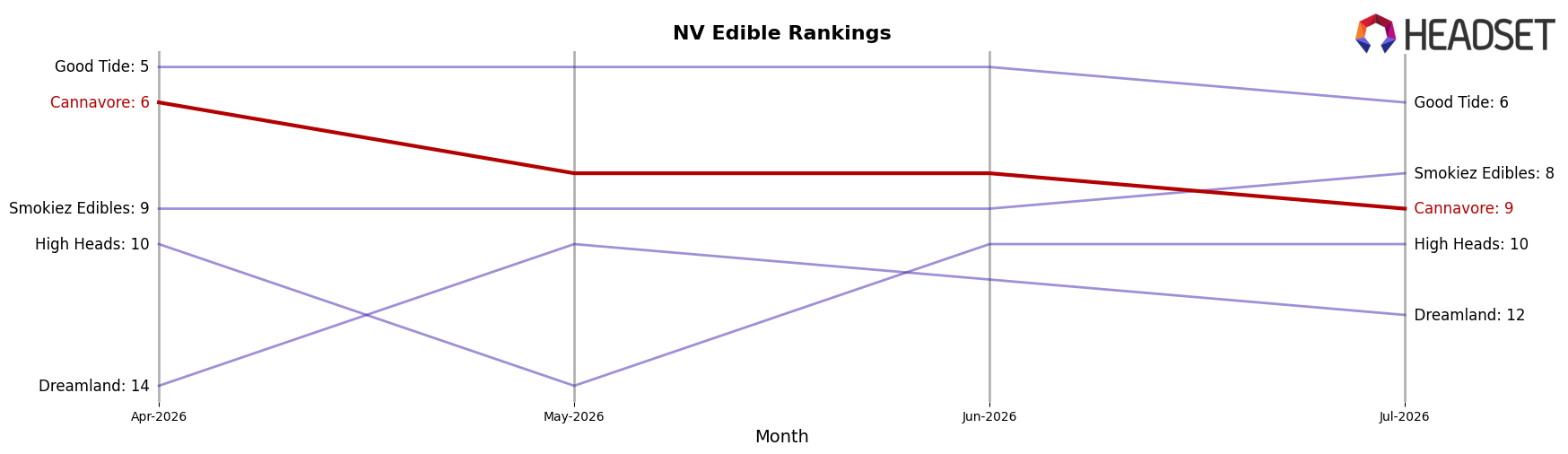

Cannavore is currently ranked #9 in NV Edible, a YoY climb of 33 positions from #42, but down 3 spots from #6 in April 2026 to #9 in July 2026, indicating momentum cooled quarter-over-quarter despite a large annual gain. Against competitors, Wyld held #1 with a 2.6% YoY sales increase while Cannavore slipped from #6 to #9 in the last three months, and Kanha / Sunderstorm advanced from #10 YoY to #4 with 196.5% YoY sales growth as Cannavore retreated 3 ranks since April 2026; this pattern implies Cannavore’s rapid annual ascent has stalled into mid-2026, requiring actions to convert past gains into sustained top-5 positioning.

Notable Products

CBN/THC 2:1 Grape Lemonade Gummies 10-Pack (200mg CBN, 100mg THC) posted the standout move in July 2026 with an 89.99% month-over-month surge, climbing into rank 7, while CBG/THC 1:1 Strawberry Watermelon Lemonade Gummies 10-Pack (100mg CBG, 100mg THC) fell 58.14% to rank 5. The top rank remained with CBD/THC 3:1 Cherry Pineapple Gummies 10-Pack (300mg CBD, 100mg THC) at rank 1 with 24.92% MoM growth and $67,235 in sales, as CBD/THC 2:1 Passion Fruit Guava Gummies 10-Pack (200mg CBD, 100mg THC) rose 33.70% to rank 3. With all top-10 SKUs concentrated in Edibles and two high-CBN formats gaining 89.99% and 54.17%, the pattern implies Cannavore is tilting toward functional minor-cannabinoid nighttime or relaxation use-cases within gummies.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.