Jun-2026

Sales

Trend

6-Month

Product Count

SKUs

Avg Price

YoY Sales Change

YoY Price Change

Market Insights Snapshot

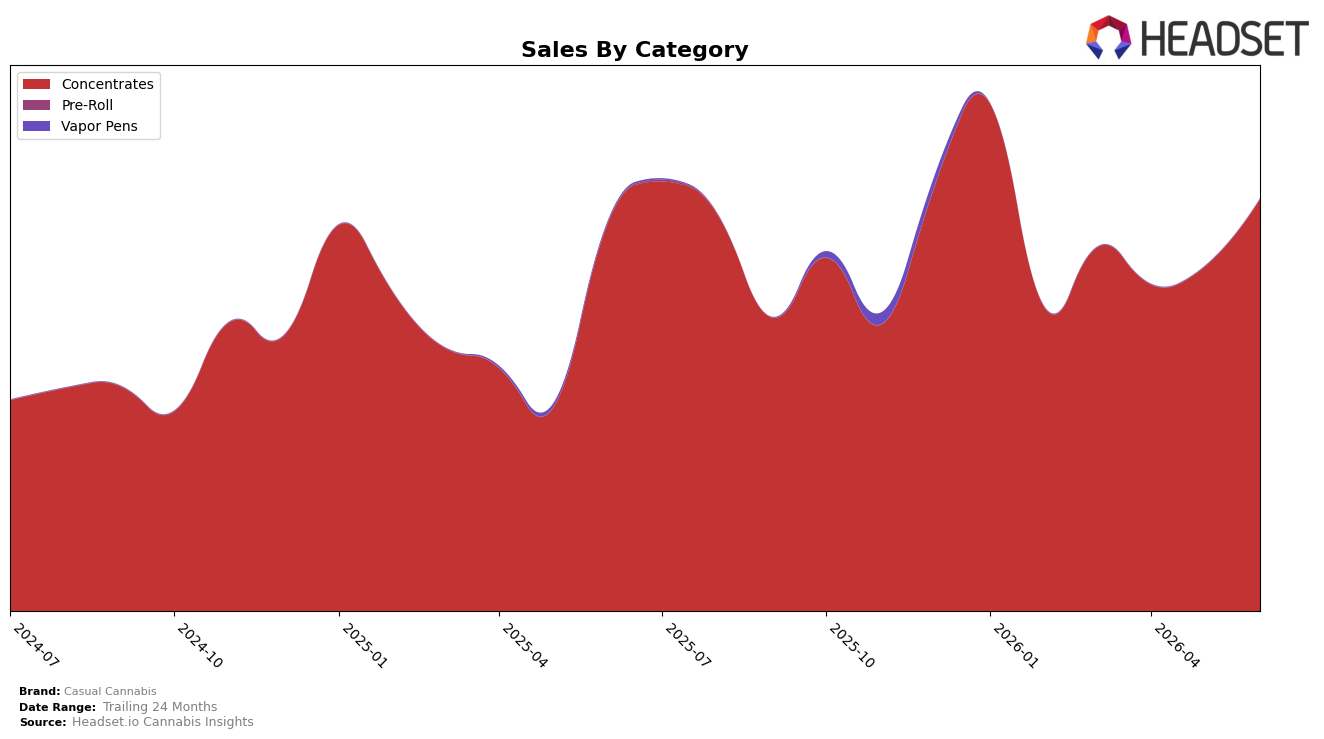

In June 2026, Casual Cannabis operated as a single-category brand with Concentrates accounting for 100.0% of sales, posting a 5.9% year-over-year increase alongside a 19.7% month-over-month gain. Within this mix, the brand’s average item price rose 0.6% year over year while total brand sales advanced 5.4% year over year, indicating volume growth outpacing pricing, and the 19.7% month-over-month uplift suggests a tactical acceleration ahead of typical summer demand. The thesis is that reliance on one category magnifies execution effects: with all revenue tied to Concentrates, even a mid‑single‑digit year-over-year gain paired with a high‑teens month-over-month surge implies that pricing discipline plus unit expansion were the levers moving share inside a narrow portfolio.

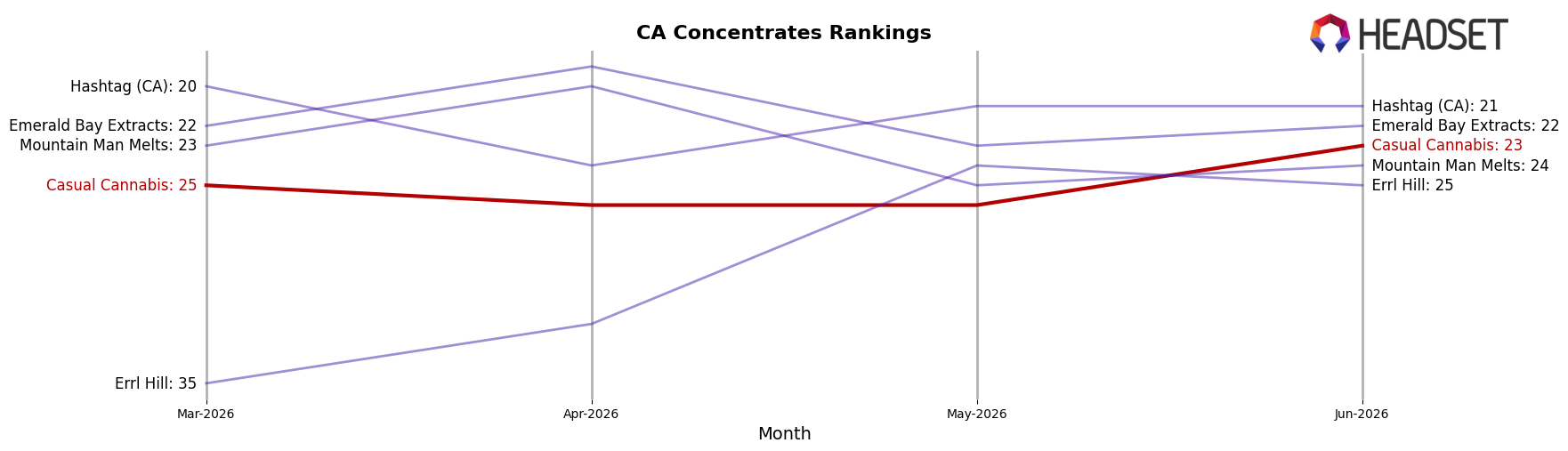

Casual Cannabis ranked 23rd in Concentrates in California, which, combined with a 19.7% month-over-month rise against a 5.9% year-over-year pace, implies recent momentum stronger than the annual trend and thus potential near-term laddering within the mid‑tier of the ranking. Given that Concentrates are 100.0% of sales while the average price only increased 0.6% year over year, the brand’s positioning hinges on sustaining unit velocity rather than price-led gains, and the 23 rank indicates room for share capture if the June cadence persists; the implication is that maintaining this month-over-month trajectory would convert into rank improvement faster than a price strategy would in this segment.

Competitive Landscape

Casual Cannabis sits at rank #23 in CA Concentrates in June 2026, improving 2 positions from #25 year over year, while slipping 3 spots from its peak rank of #20 reached in January 2026; in contrast, Raw Garden held #1 with a 0-position YoY change as 710 Labs climbed from #4 to #3 with 24.7% YoY sales growth. Over the last three months Casual Cannabis moved from #25 to #23 (+2 ranks) as category leaders like STIIIZY maintained #2 with a 0-position YoY change and 4.2% YoY sales growth, while Punch Extracts / Punch Edibles slid from #3 to #4 amid a 29.1% YoY sales decline; this pattern implies Casual Cannabis is inching back into the competitive mid-pack but must convert small rank gains into sustained share against stable top-5 incumbents.

Notable Products

Master Cake Badder (1g) delivered the standout move in June 2026 with a +252.7% month-over-month surge to rank 1, while Northern Ape Badder (1g) also accelerated by +239.7% to rank 3, indicating outsized momentum concentrated at the very top. Banana Marker Badder (1g) entered at rank 2 with $9,940 in sales, positioning between two triple-digit gainers and reinforcing that ranks 1–3 are anchored by Badders. With all top 10 products in Concentrates and ten of the top ten specifically Badder SKUs, the assortment is consolidated around a single format rather than spread across categories. This pattern implies Casual Cannabis is leaning into a depth strategy in Badders to capture share via a narrow, high-velocity lineup rather than diversifying formats.

Top Selling Cannabis Brands

Data for this report comes from real-time sales reporting by participating cannabis retailers via their point-of-sale systems, which are linked up with Headset’s business intelligence software. Headset’s data is very reliable, as it comes digitally direct from our partner retailers. However, the potential does exist for misreporting in the instance of duplicates, incorrectly classified products, inaccurate entry of products into point-of-sale systems, or even simple human error at the point of purchase. Thus, there is a slight margin of error to consider. Brands listed on this page are ranked in the top twenty within the market and product category by total retail sales volume.